Market Data

January 19, 2022

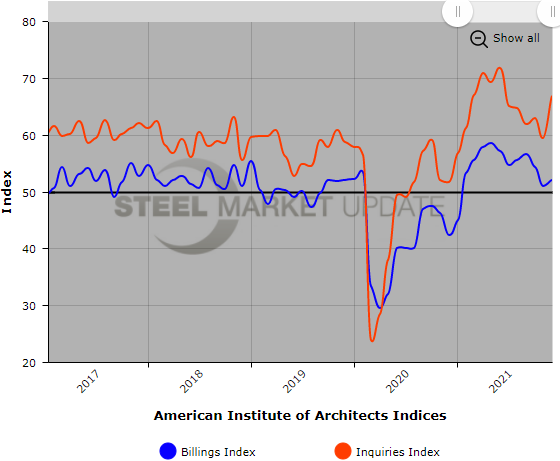

Architectural Billings Index Expands in December

Written by David Schollaert

Demand for design services from architecture firms in the U.S. improved for the 11th straight month in December, according to the latest report from the American Institute of Architects. AIA’s Architecture Billings Index rose from 51.0 in November to 52.0 in December. The ABI expanded each month in 2021 except for January.

The index for new project inquiries expanded by 8.0 points to 62.0, while the new design contracts index was flat month on month at a reading of 55.8.

“Business conditions at architecture firms ended 2021 on a high note. Firm billings increased every month of the year except for January, as most firms experienced a strong rebound from the 2020 downturn. And despite a variety of concerns related to the omicron variant, prices/availability of construction materials, and labor shortages, firms also continued to report a robust supply of work in the pipeline, and backlogs remaining near the highest levels ever reported since we started collecting this data in 2010, at an average of 6.5 months,” reported AIA.

The Architecture Billings Index is an advance economic indicator for nonresidential construction activity, with a lead time of approximately 9-12 months. A score above 50 indicates an increase in activity and a score below 50 a decrease.

Key ABI highlights for September include:

- Regional averages: Midwest (51.0); South (56.4); West (47.5); Northeast (45.3)

- Sector index breakdown: mixed practice (49.6); commercial/industrial (49.2); multifamily residential (49.2); institutional (47.6)

Regional and sector scores are calculated as three-month averages.

Below is a graph showing the history of the AIA Architecture Billings Index. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging into or navigating the website, please contact us at info@SteelMarketUpdate.com.

By David Schollaert, David@SteelMarketUpdate.com