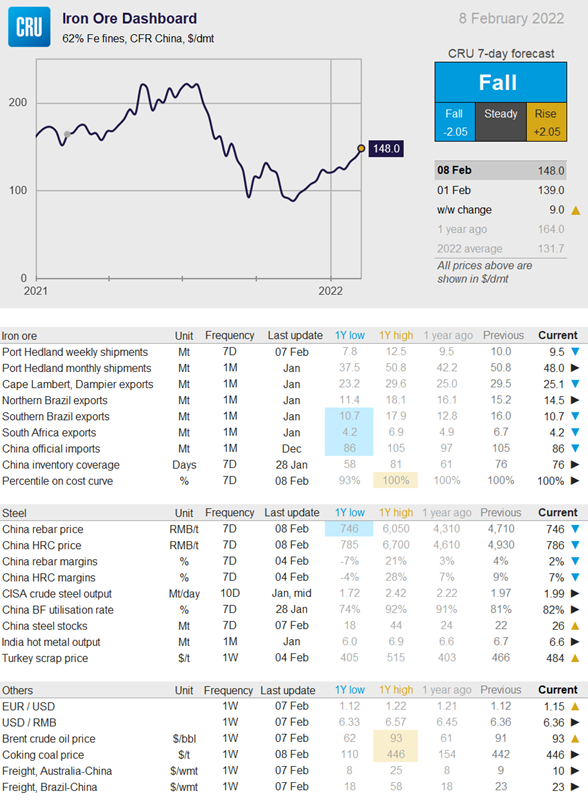

Prices

February 8, 2022

CRU: Post-CNY Speculation Pushes Iron Ore Up

Written by Aaron Kearney-Keaveny

By CRU Research Analyst Aaron Kearney-Keaveny, from CRU’s Iron Ore Market Outlook, Feb. 8

The iron ore price has been driven up over the last week, despite sparse activity during and after the Chinese holiday. The rise in price primarily came from traders who have been increasing their stocks in anticipation of higher prices, not from actual changes to the fundamentals.

![]() The Chinese steel market has been quiet during the Chinese New Year holidays, but steel prices opened high after the market reopened on Feb. 7. This was driven by expected post-holiday demand recovery and further speculation on the government’s support to infrastructure and the real estate sector. This has also fueled price hikes for iron ore, even though BF operation slowed during the holiday period, leading to port inventories rising to over 157 Mt. The Chinese government has addressed speculation’s role in the recent rise, which has caused concern by traders that policies could be introduced to reverse the spike. The high prices for coking coal have kept high grade premia high, but as it now levels out at a peak, this will start to reverse.

The Chinese steel market has been quiet during the Chinese New Year holidays, but steel prices opened high after the market reopened on Feb. 7. This was driven by expected post-holiday demand recovery and further speculation on the government’s support to infrastructure and the real estate sector. This has also fueled price hikes for iron ore, even though BF operation slowed during the holiday period, leading to port inventories rising to over 157 Mt. The Chinese government has addressed speculation’s role in the recent rise, which has caused concern by traders that policies could be introduced to reverse the spike. The high prices for coking coal have kept high grade premia high, but as it now levels out at a peak, this will start to reverse.

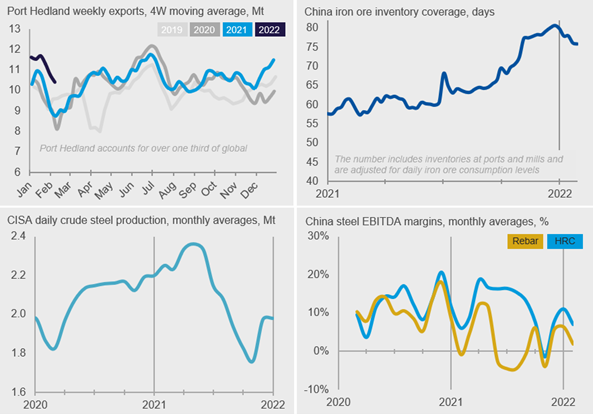

Supply from Port Hedland has fallen to 9.5 Mt, levels, which are much more expected for this time of year after an impressive January. There are currently no tropical lows nor cyclones threatening iron ore ports, although there are some minor tropical lows in surrounding areas. The Bureau of Meteorology in Australia has lifted the risk assessment level from very low (<5% chance of occurrence) to low (5-20%). The Australian government has lifted travel restrictions, allowing for vaccinated tourists to enter the country, but Western Australia still maintains its regional restrictions, which will continue the labor shortages faced by mining companies. Western Australia’s Covid-19 infection rate has gone up, but remains at very low levels.

Exports from northern Brazil have continued to fall this week, while the south remains steady after recovering from flooding. January had the lowest level of south Brazilian exports since March 2020 with 10.7 Mt, while the north shipped a more standardized 14.5 Mt. Pellet feed exports notably suffered, meaning that pellet production in MENA has a high chance of being affected. CSN saw the largest fall in exports as a result of the weather disruptions. Heavier rain and storms are predicted for the next week. While this is unlikely to have the same impact as in the last month, it is still a notable risk that will keep market participants’ attention.

Supply issues and risks still place upward pressure on iron ore’s price, from weather fears in Brazil to cyclones, labor shortages, and Covid-19 issues in Australia. The main driver, however, will be the fall in consumption for iron ore. The traders waiting for notably higher steel output will have to wait until March when restrictions end after the Paralympics. Their recent stocking will slow down and diminish as iron ore consumption remains low and access to large port stocks remain.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com