Market Data

February 17, 2022

Steel Mill Lead Times and Negotiations: Waiting for an Inflection Point

Written by Tim Triplett

Steel mill lead times, which have shortened to near historical averages, are about as low as they will go and now register only minor movements up or down from week to week, based on Steel Market Update’s surveys of the market. Likewise, SMU’s data on negotiations between mills and buyers has reached a similar steady state.

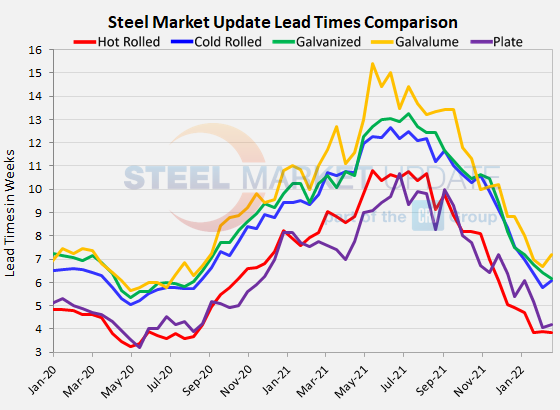

Buyers polled by SMU over the past three days reported mill lead times ranging from 3-5 weeks for hot rolled, 5-8 weeks for cold rolled, 4-8 weeks for galvanized, 6-9 weeks for Galvalume, and 4-5 weeks for plate.

The latest survey shows that the average lead time for hot rolled was roughly flat at 3.84 weeks. Cold rolled lead times now average 6.07 weeks, a small uptick from 5.79 weeks in early February. Galvanized lead times dipped to 6.16 weeks from 6.43 in the past two weeks. The average Galvalume lead time is now down to about 7.20 weeks. Mill lead times for plate are now at 4.20 weeks, up slightly from 4.08 weeks in SMU’s last check of the market.

When Will Lead Times Extend?

Of more interest is when lead times will begin to extend again, signaling that the mills are getting busier, processing more orders, and more likely to begin holding the line on prices.

SMU asked buyers in this week’s poll: When do you expect mill lead times to begin extending again? About 20% of the respondents said they still see lead times getting shorter. Another 28% said lead times are already or will soon extend. The majority, the other 52%, don’t expect longer lead times until the second quarter, if not the second half of the year.

So, clearly, there is no consensus on when mill lead times will turn around—and by extension when steel prices may finally reach an inflection point.

Here’s what a few survey respondents had to say:

“It’ll be Q2 or Q3 until lead times start to stabilize and go back out. We need service centers to start buying and automotive to come back.”

“Mill outages in March will cause lead times to start tightening.”

“Order books will increase in early to mid-March.”

“Demand has been the savior, but it may not continue into the second quarter.”

“Customers will re-engage shortly. They cannot stay on the sideline much longer for spot.”

“There will not be as much foreign coming in through July. It’s too scary to buy seeing the direction pricing is taking.”

Meanwhile, steel prices continue to see weekly declines of $50-100 per ton. SMU’s check of the market this week puts the benchmark price for hot rolled coil at $1,080 per ton, down 45% from its peak last September.

Note: These lead times are based on the average from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. SMU measures lead times as the time it takes from when an order is placed with the mill to when the order is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our Steel Mill Lead Times data, visit our website here.

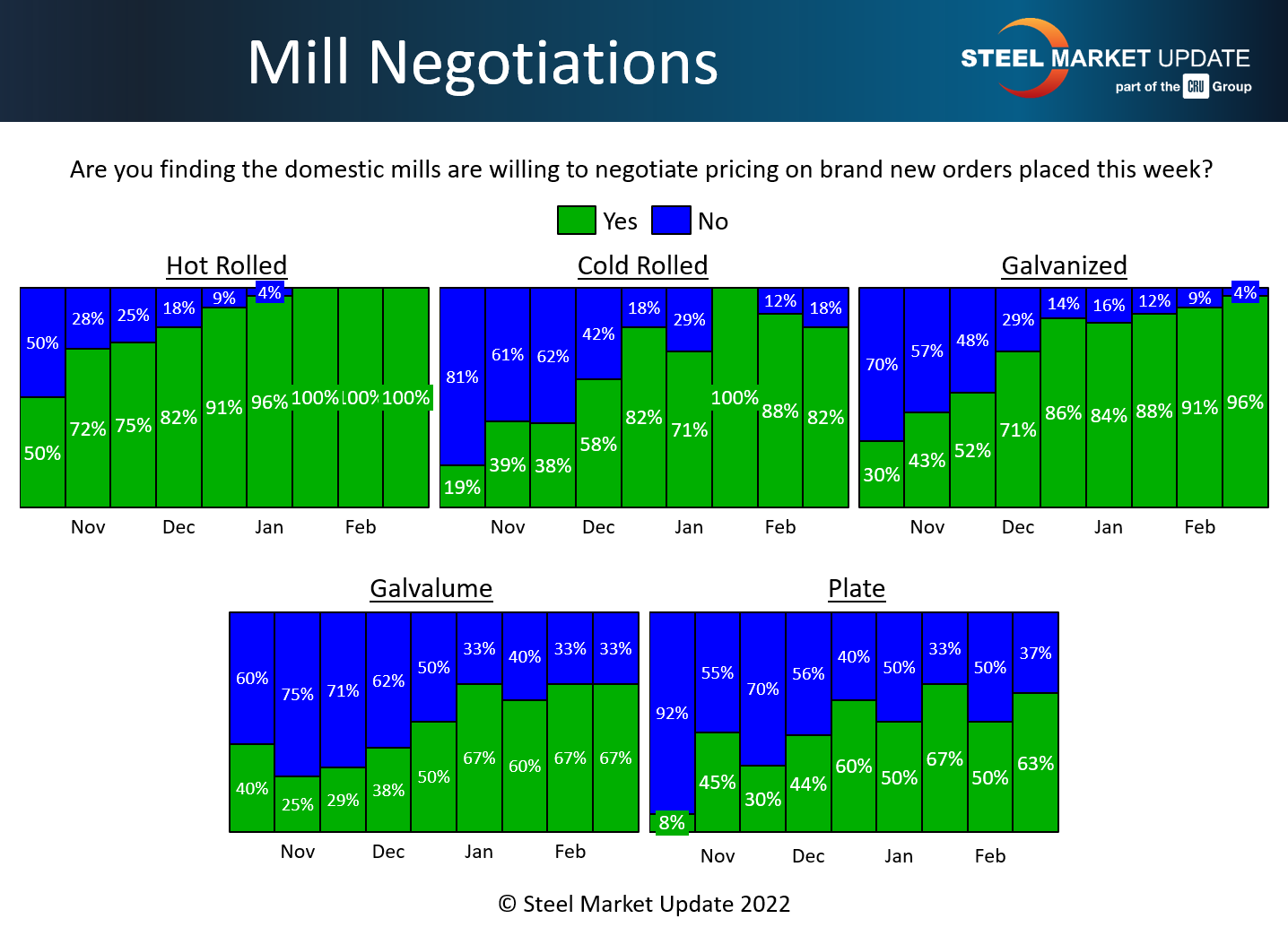

Negotiations

There’s not much new to report on the tone of price negotiations between buyers and the mills. In an environment where steel prices continue to decline week after week, buyers clearly maintain the upper hand, as shown by the predominantly green bars in the chart below

Every two weeks, Steel Market Update asks readers: Are you finding the domestic mills willing to negotiate spot pricing on new orders placed this week? The vast majority of buyers in every product category tell SMU that mills are in a deal-making mode to secure sales before the next price drop.

Like lead times, which can’t get much shorter, price negotiations can’t get much more one-sided. It won’t be until lead times begin to lengthen again and mills begin to say “no” again when customers ask for a discount that this data will signal a change in the direction of pricing.

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.

By Tim Triplett, Tim@SteelMarketUpdate.com