Prices

March 6, 2022

CRU: Ukraine Nightmare Scenario Facing Aluminum

Written by Greg Wittbecker

By Greg Wittbecker, Advisor, CRU Group

Two weeks ago, I described how the aluminum industry would not run out of metal supply in 2022 despite the fears of some. Fast forward to today, and we now have the worst case scenario of the war in Ukraine likely leading to Russia being a pariah in the global aluminum community.

It will be difficult to compensate for the effect of wholesale sanctions on Russian aluminum. Thus far, the NATO alliance has taken measured steps to ramp up sanctions on Russia, with energy exports carved out and aluminum commerce continuing. As the carnage from the war escalates, it is highly likely that these exemptions will go away. Removing Russian aluminum from the market will eliminate any perceived “cushion” in supply.

Let’s put it into context as fundamentals continue to be fluid:

• CRU has now upwardly revised its estimate of the 2022 primary deficit from 1.6 million to 2.2 million tons.

• Russian exports of primary metal are about 3.3 million tons/year.

Assuming the Russians are embargoed from trade, that means the effective deficit goes to 5.5 million tons. Now, the fear that “we are out of everything” (we wrote about this in our column two weeks ago) DOES become quite real.

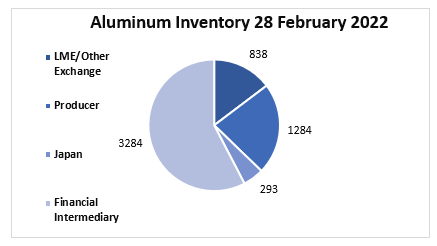

CRU’s latest estimate of World ex China inventories ending February 2022 stands at 5.7 million tons.

Clearly, it is unrealistic to think that we could deplete these stocks in their totality to cover that 5.5-million-ton deficit. As we discussed here in our last column, those stocks held by financial intermediaries (3.2 million) and the LME (.83 million) are the most viable sources of supply. That would still leave the market scrambling for another 1.5 million tons.

How Else Does the Market Solve Its Problem?

On the supply side:

• Producers will be challenged to further reduce work-in-progress and expedite shipments to reduce metal “in transit.”

• We may see previously marginal, idled primary smelting capacity be restarted, such as capacity in the U.S., Brazil and India. However, this may not come fast enough to solve the problem for 2022.

• Brownfield projects in India may be accelerated, for possible help late in 2022.

• Some substitution of scrap for primary metal will be attempted, but this will require accelerated capital project completions to bring more scrap processing into play during late 2022.

• The NATO alliance might allow some carve-out of limited amounts of Russian exports for special purpose allocation.

• We could see higher Chinese exports of semi-fabricated aluminum entering Europe and the U.S. to replace domestic mill production unable to secure enough primary or secondary substrate to meet demand.

On the demand side:

• Obviously, higher prices for aluminum may result in demand destruction as end consumers delay or quit buying and/or we see some material substitution. Steel might benefit from this.

Does this Deficit and Price Action Force Consideration to Remove Section 232?

LME aluminum prices are now at $3,700, within reach of the record high of $4,300 set in June 1988. U.S. and European physical premiums are at record highs, with the U.S. Midwest at 38 cents/pound over LME. This has pushed Midwest aluminum to $2.13 per pound. That is obviously highly inflationary and a bitter pill for those major buyers like auto, beverage companies and building products to absorb.

Opponents to Section 232’s continuation have some solid arguments:

• Domestic aluminum producers (Alcoa, Century, Magnitude 7) are making very good money; they don’t need safeguard duties to keep them whole.

• After four years, domestic aluminum production has flatlined and is not responding to price incentives to re-open remaining idled capacity, much less consider new greenfield capacity. In fact, Alcoa shut down its Washington state smelter at Ferndale and has idled capacity at its Warrick, Ind., smelter. Magnitude 7 has one-third of its capacity shut down at New Madrid, Mo.

This behavior contrasts to that of steel, which also operates under the protection of Section 232. New steel capacity is being built, notably U.S. Steel and Nucor announcing major projects in Arkansas and West Virginia.

It would not surprise us to learn that leading buyers begin to raise these arguments in Washington, D.C., demanding that Section 232 be lifted on aluminum.

While that may not solve the deficit, it would remove nearly 18 cents/pound of price exposure that is directly linked to the 10% import duty.

Greg Wittbecker joined CRU in January 2018 after retiring from Alcoa, where he was Vice President of Industry Analysis and Managing Director of Alcoa Beijing Trading, based in Shanghai, China. His career spans 35 years in the aluminum industry, having also held senior commercial and management roles at Cargill, Wise Metals and Koch Supply and Trading. Greg brings perspective on the entire aluminum supply chain from bauxite to aluminum finished products and will be a regular contributor to SMU going forward. He can be reached at gregory.wittbecker@crugroup.com

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com