Analysis

April 15, 2022

North American Auto Assemblies Accelerate in March

Written by David Schollaert

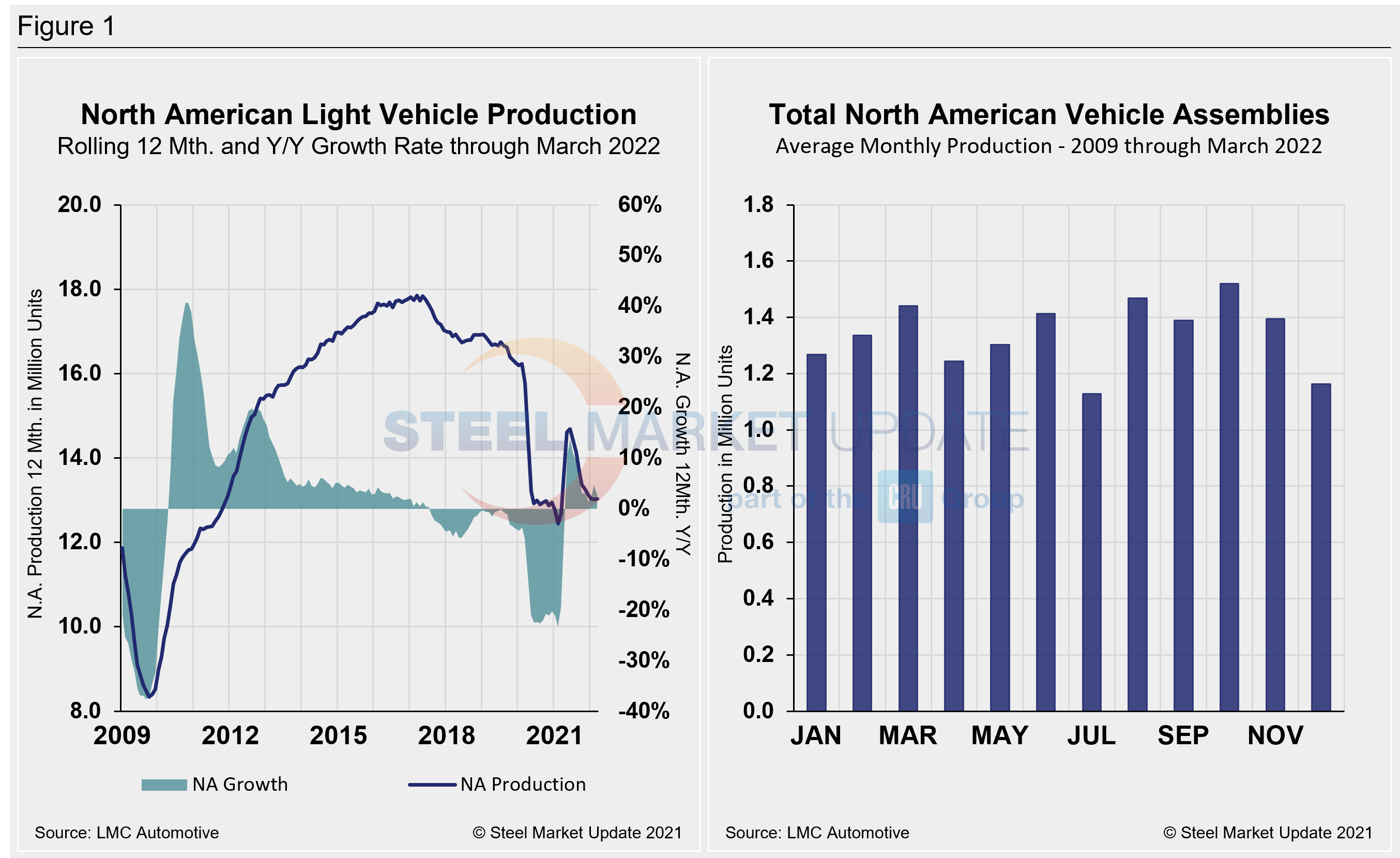

North American auto assemblies grew by 18.1% in March, expanding for the third straight month despite ongoing supply hurdles. Though North American production has improved since last December, March’s recovery was just 1% higher year on year. And it’s still 13.5% below the pre-pandemic period of March 2019.

At the onset of 2022, the global auto industry was looking forward to a year of growth. Nearly two years removed from the initial pandemic shock, sentiment was upbeat with Covid rates receding and supply chains expected to improve. Recent events have greatly complicated the outlook, however, as the war in Ukraine takes the auto sector on another roller coaster ride.

The fallout from the war has caused energy prices to skyrocket. An earthquake in Japan and new lockdowns in China all threaten more disruption for the industry, specifically semiconductor supply. Concerns about supply chains are again at the forefront.

Semiconductor lead times have continued to increase in March. They currently stand at around 27 weeks, with exports from China and South Korea down noticeably, according to CRU’s April Automotive Sector Outlook. In February, China exported just 2% more microchips than in the same period two years ago. And that figure was down 46% from December’s total. Korean exports, by comparison, were up 31% versus February 2020 but 62% down compared to December.

“A possible explanation for falling exports is the combination of growth in domestic (Chinese and Korean) demand and production reaching its maximum capacity,” said CRU. “There has been heavy investment in new fabs, but these will still require months to be fully operational.”

Increased near-shoring efforts are leading to greater allocation of semiconductors to domestic OEMs within chip-producing countries. And an increasing EV penetration rate in China is driving higher-than-average internal demand. These dynamics are undercutting export availability.

The North American auto industry has been resilient, as evidenced by recent production gains. But automakers continue to be met with strong supply-related headwinds. The industry is nearly two years into a period of chip and parts shortages. And those problems aren’t likely to get any better given additional strains from the war in Ukraine.

North American vehicle production, including personal and commercial vehicles, totaled 1.273 million units in March, up from the downwardly revised February total of 1.078 million units. Though improved, North American automotive assembly totals are still well behind pre-pandemic totals. Last month’s total was down 146,000 units from February 2020’s production total.

Below in Figure 1 is North American light vehicle production since 2009 on a rolling 12-month and year-over-year growth rate. Also included is average monthly production, including seasonality, over the same period.

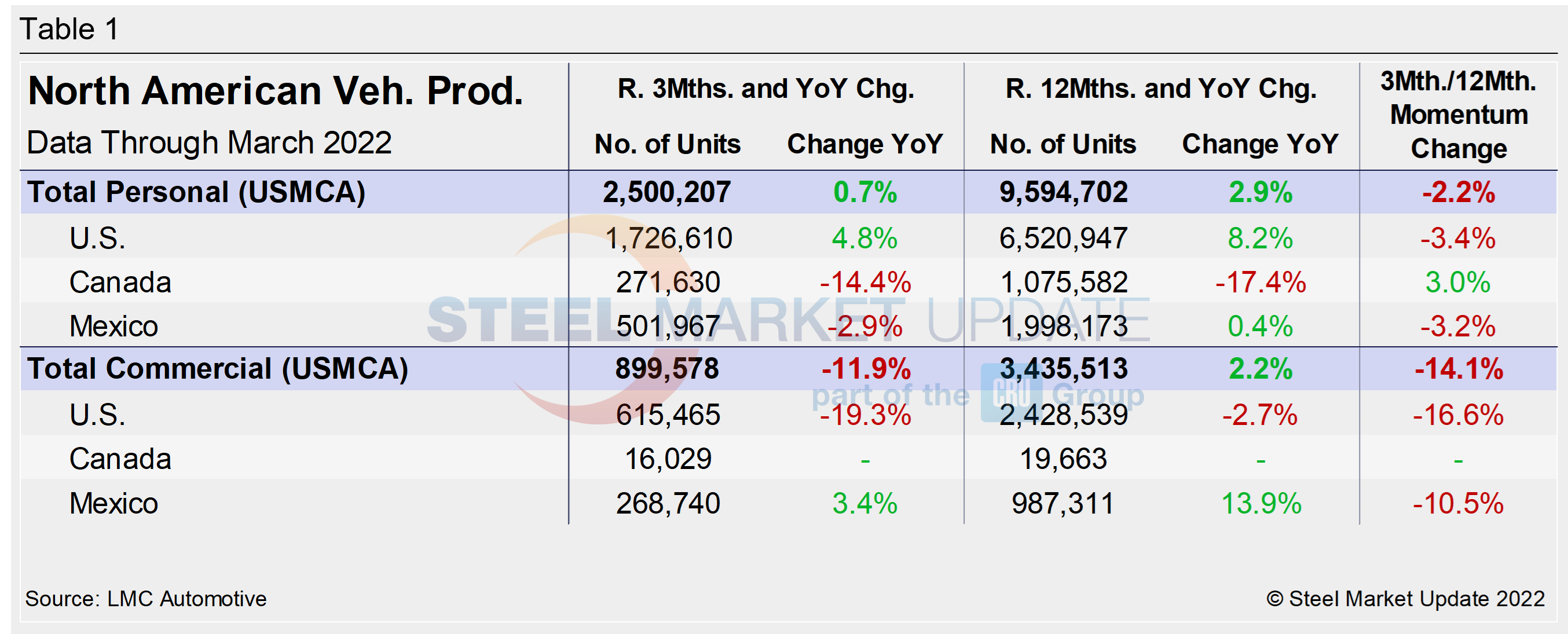

A short-term snapshot of assembly by nation and vehicle type is shown in the table below. It breaks down total North American personal and commercial vehicle production into US, Canadian and Mexican components, along with the three- and 12-month growth rate for each. On the far right, it shows the momentum for the total and for each of the three nations.

Although the initial rebound from the Covid doldrums was impressive, the effect of the chip and parts shortage has been even more damaging due to its prolonged nature. Through last June, growth rates for personal and commercial light vehicles soared by 156.8% and 127.4%, respectively. But they have since nosedived because the chip shortage and supply-chain disruptions have persisted.

In three months through March, the growth rate for total personal vehicle assemblies in the USMCA region was a mere 0.7% year on year. That’s still noticeably improved from -6.0% month on month. Growth for commercial and light vehicle assemblies has taken a hit, falling from -7.4% in February to -11.9% in March. The decline in commercial assembly growth is underpinned by decreased demand for fleet vehicles, as automakers focus their limited microchips on the best-selling vehicles. The impact of the global semiconductor chip shortage on automotive production across North America cannot be understated.

Personal Vehicle Production

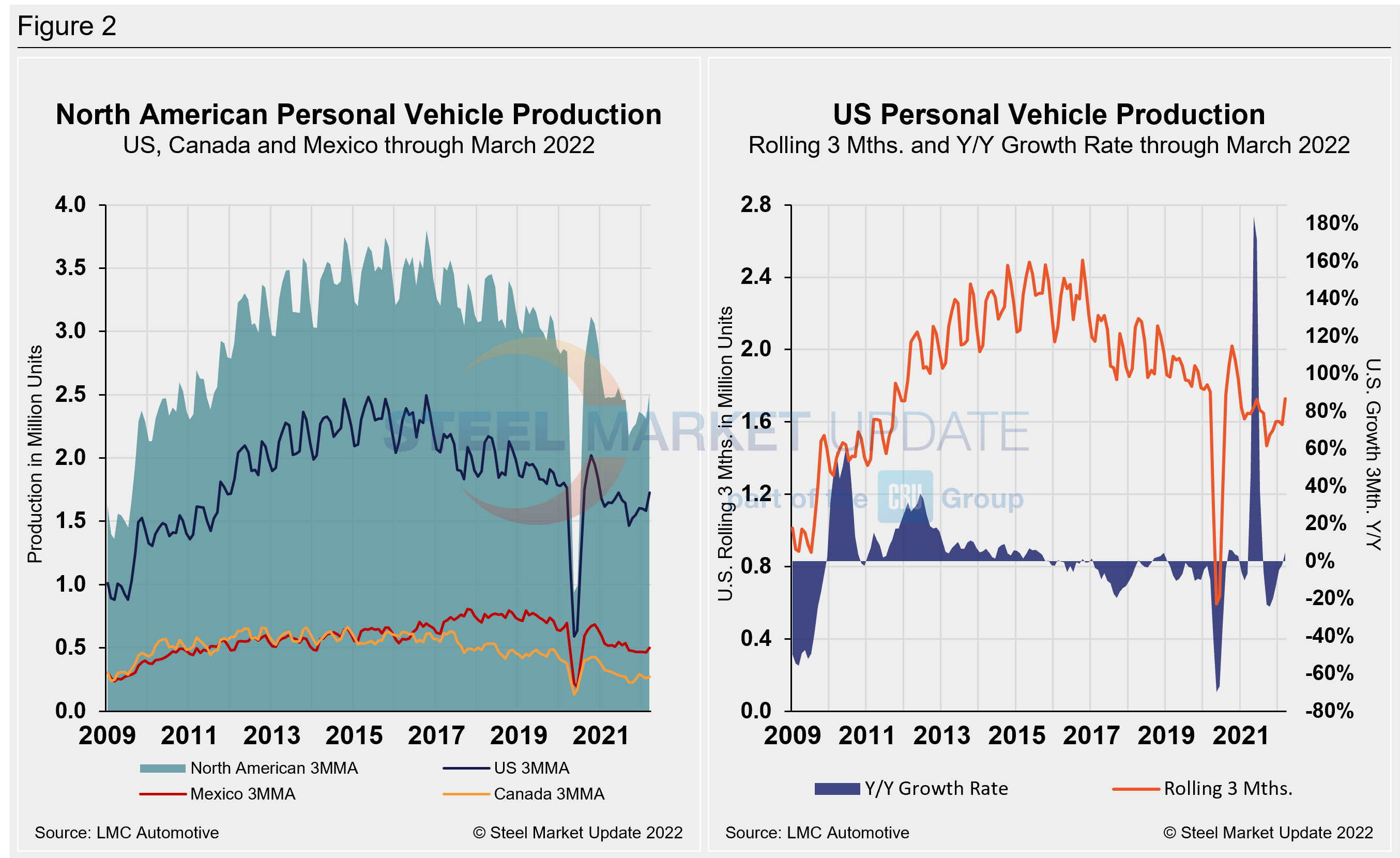

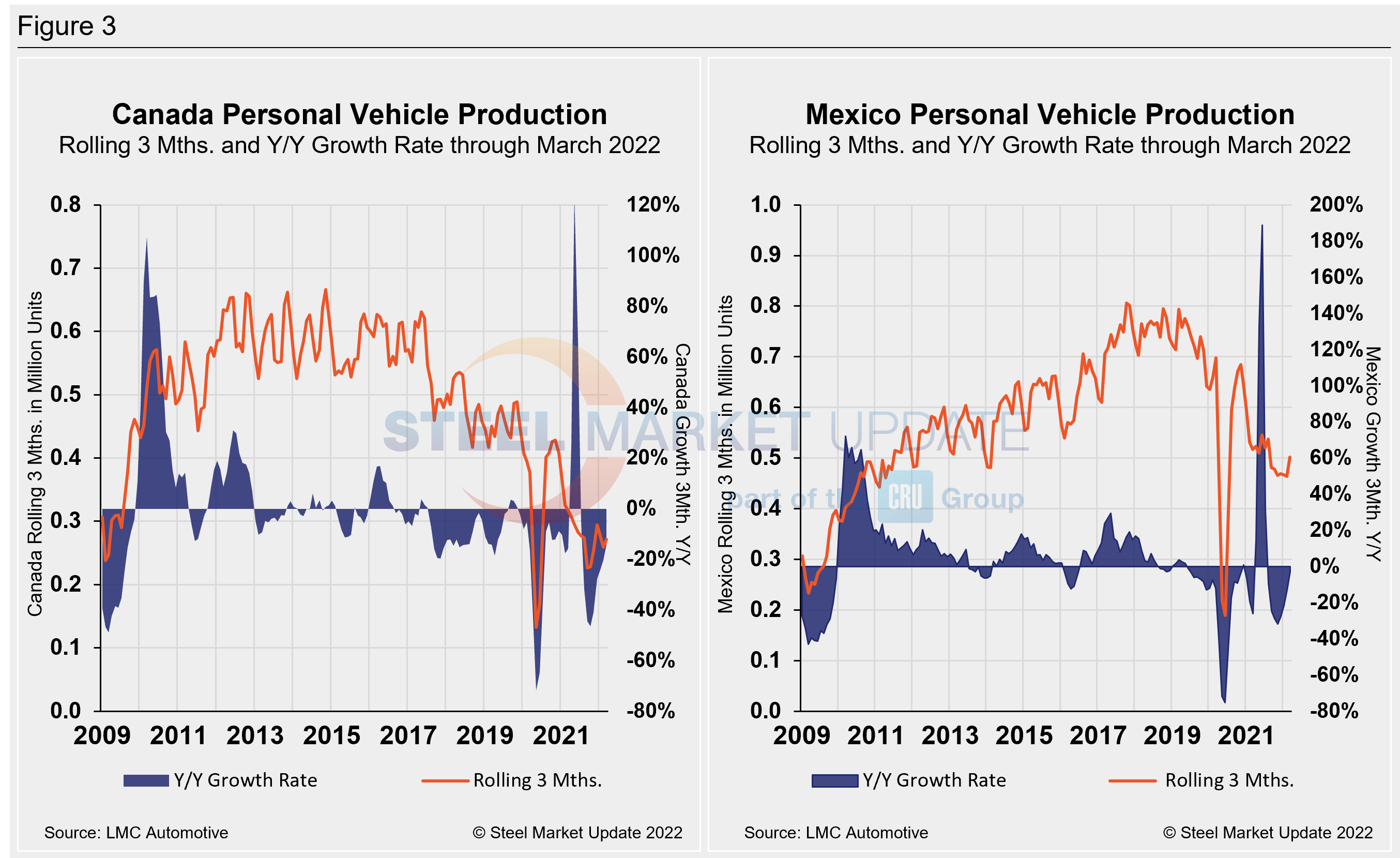

The longer-term picture of personal vehicle production across North America is shown below. The first chart in Figure 2 shows total personal vehicle production for North America as well as total for the US, Canada and Mexico individually. The production of personal vehicles in the US and the year-over-year growth rate are displayed in the second chart. Figure 3 shows side-by-side the production of personal vehicles in Canada and Mexico and the year-over-year growth rate.

In terms of personal vehicle production, all three – the US, Canada, and Mexico – saw double-digit gains in March. Production has increased for at least two out of the first three months of the year despite ongoing supply-chain limitations and work stoppages.

Canada saw the greatest percentage gain, up 21.6% (+32,838 units) versus the month prior. The US saw the largest increase in total units, up 94,049 (+17.1%) month over month. Mexican auto assemblies were also 18.9% higher (+17,047 units) over the same period.

The annual growth rate across the region in February was mixed. Mexico saw the best gain at 9.9%, followed by the US at 6.8%. Canada’s annual growth rate rebounded 5.8% in March after falling 8.1% the month prior. Overall, the region saw an increase of 143,924 units in March, an 18.1% jump over February’s total.

Canada’s personal vehicle production share of the North American market slipped slightly to 10.9% month over month in March, while Mexico’s share was unchanged at 20.1%. The US saw its share of the North American market rise four percentage points to 69.1% in March.

Commercial Vehicle Production

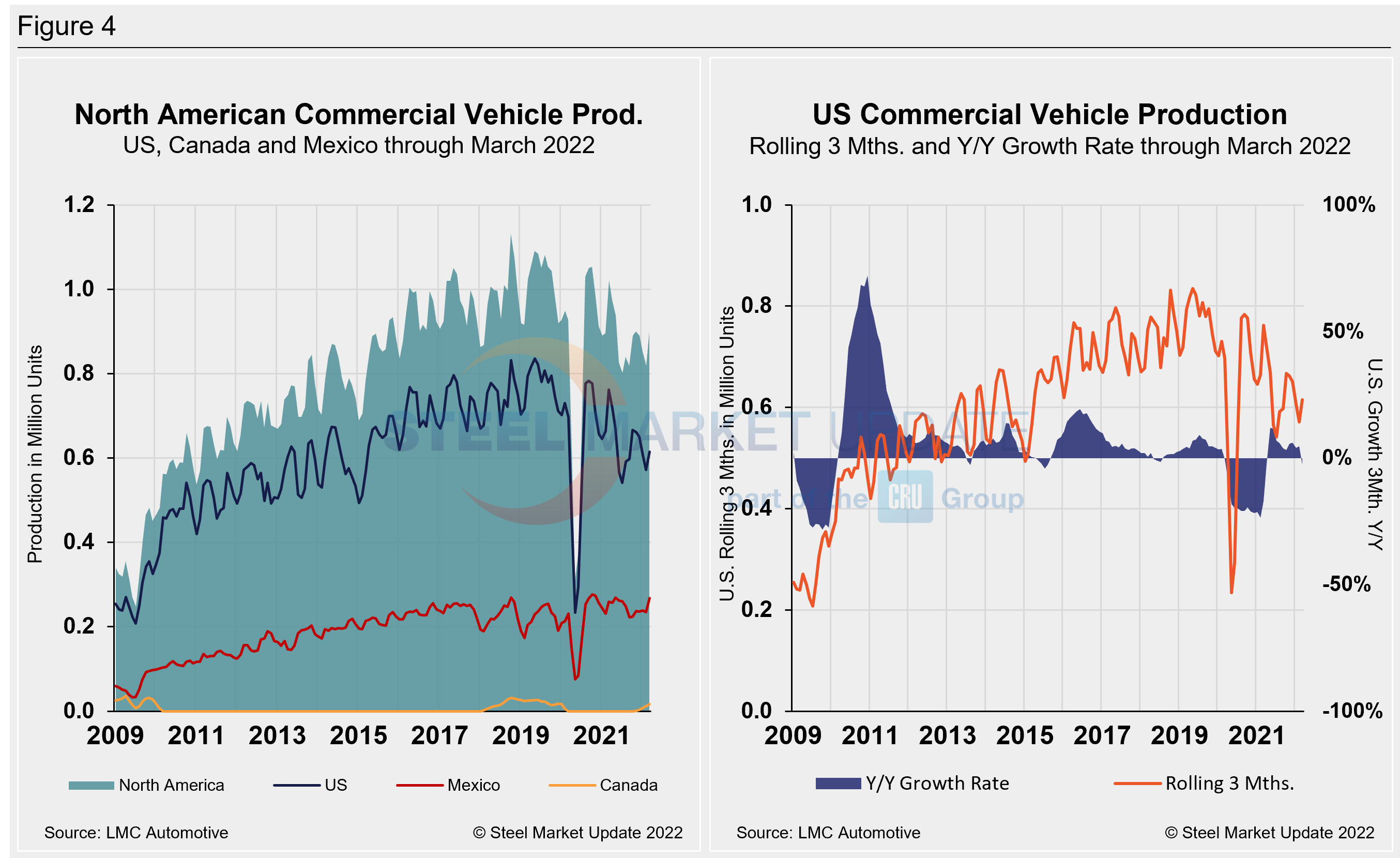

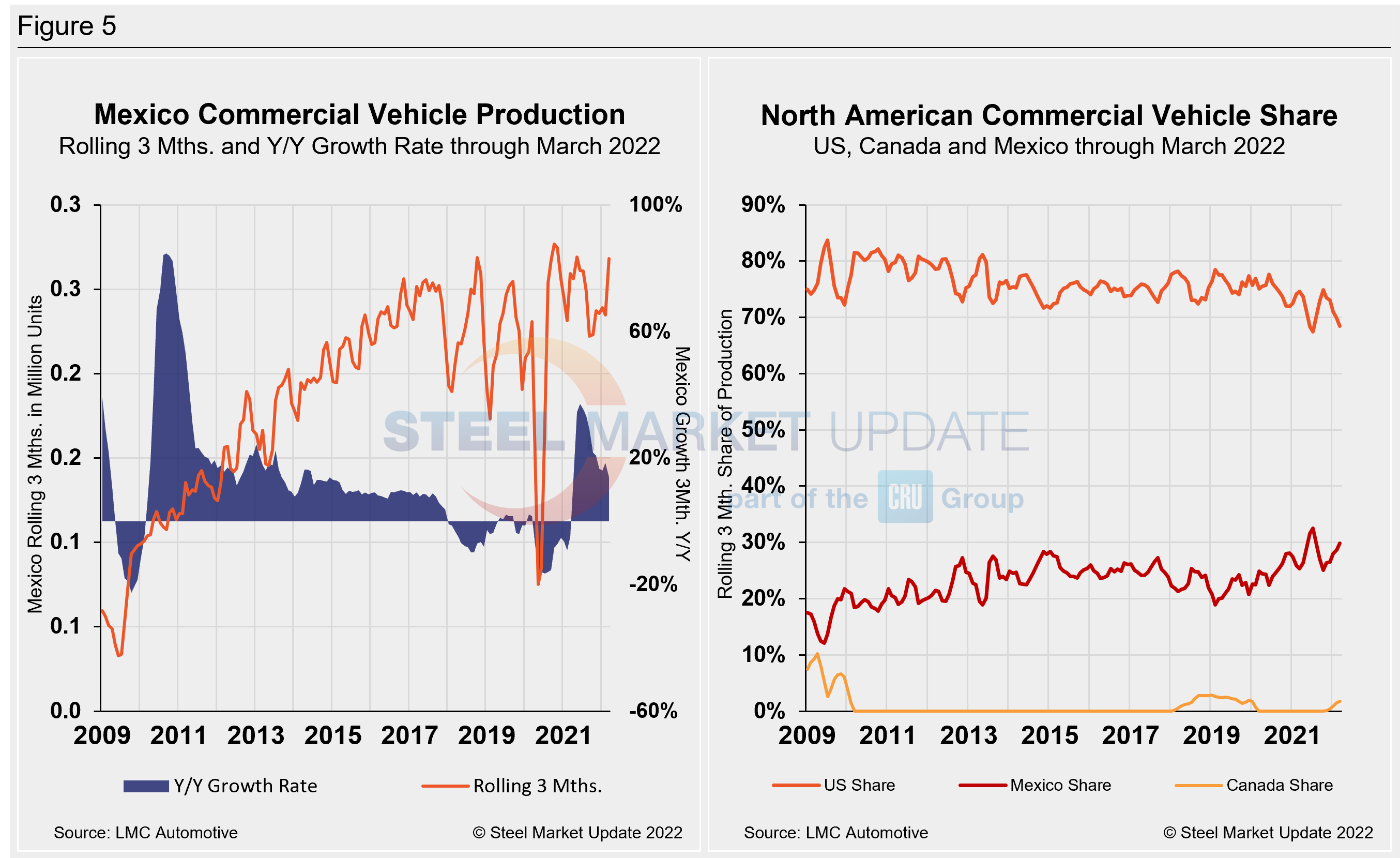

Total commercial vehicle production for North America and the total for each nation within the region are shown in the first chart in Figure 4 on a rolling three-month basis. The production of commercial vehicles in the US and the year-over-year growth rate are displayed in the second chart. The first chart in Figure 5 shows the production of commercial vehicles and the year-over-year growth rate in Mexico. The the second chart shows the production share for each nation in North America.

Of note for the Canadian automotive sector: March marked Canada’s fifth straight month of commercial vehicle production after a 20-month production halt. Canada produced 6,570 light commercial vehicles in March, a 25.9% jump month over month.

North American commercial vehicle production rose 18.2% in March to 333,426 units. The 51,293-unit gain month over month was driven by growth across the region. The US saw the highest unit gain, up 39,774 (+20.8%), followed by Mexico, up 10,167 (+11.9%), and Canada.

The annual commercial production growth rate is now -11.9% for the region, with output down nearly 125,000 units year over year. The US share was 68.4%, down 0.6 percentage points in March month over month. Both Mexico and Canada saw their shares rise in March to 29.8% and 1.8%, respectively. Presently, Mexico exports just under 80% of its light vehicle production. The US and Canada are the highest volume destinations for Mexican exports.

Editor’s Note: This report is based on data from LMC Automotive for automotive assemblies in the US, Canada, and Mexico. The breakdown of assemblies is “Personal” (cars for personal use) and “Commercial” (light vehicles less than 6.0 metric tons gross vehicle weight rating; heavy trucks and buses are not included).

By David Schollaert, David@SteelMarketUpdate.com