Overseas

June 9, 2022

CRU: Markets in Asia Stabilize as Price Drops Elsewhere Accelerate

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Sheet Products Monitor, June 8

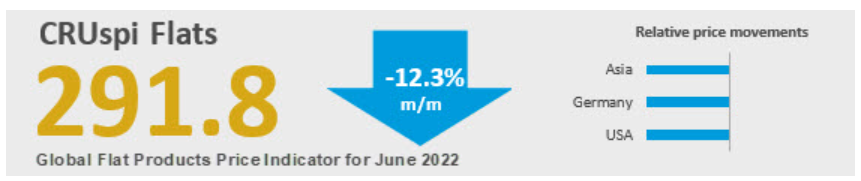

The CRUspi plummeted again month-on-month in June by over 12.3%, which is a larger drop than in May. This makes it the third-largest percentage point drop on record and the second largest in terms of total points. The supply shock caused by the war in Ukraine has eased substantially, and supply continues to outpace demand in many key markets. Still, recent developments in Asia have helped stabilize prices in the region, creating a sharp divide in price movements in the east and west.

Global sheet prices continued to fall in most regions of the world, but declines in North America and Europe were sharper than those elsewhere. In both regions, sheet availability has continued to increase even as demand remains stable or lessens. In combination with falling raw material prices, downward pressure in both markets caused price falls to accelerate in the weeks following our last report. In Asia, easing Covid-19 lockdown measures in China have helped prevent further price declines. And in some locations, prices even rose week-on-week (WoW). In addition, the surprise implementation of a new export tariff on steel in India has caused sellers there to withdraw material on offer, which has helped further tighten markets in the region.

Sheet prices in Europe have returned near to or below where they were immediately before Russia’s invasion of Ukraine. Despite missing material from both countries, European buyers have been able to import from Asia at prices well below domestic offers at a time when end-use demand is cooling. Demand is also waning in the US, and sheet prices have fallen at an accelerating rate WoW due to increased availability and falling raw material prices. Still, US prices have yet to fall to pre-war levels. Since reaching their peak levels in April, prices in Europe and the US are now off by ~$430 per ton and ~$335 per ton, respectively.

These falling prices indicate that the supply shock caused by the war has eased. Within Russia itself, domestic prices and demand have plummeted as sanctions have hampered activity in the local industry and as buyers abroad self-imposed embargoes on Russian material. Meanwhile, Ukrainian producers have found some success in restarting output and shifting volumes away from ports toward destinations in Europe via rail. Still, Ukrainian steel output remains a fraction of what it was before the war began.

In Asia, prices have begun to stabilize now that China is easing lockdown measures in key cities. This has allowed manufacturing activity to resume and domestic mills to release built-up inventories. At the same time, Chinese exporters are now lowering material on offer as they redirect volumes to the domestic market. Adding to this tightness in exports, and generating more bullish sentiment in the region, was an unexpected implementation of export tariffs on steel by the Indian government. As a result of this development, Indian exporters have withdrawn offers to other areas of the world and domestic prices have fallen sharply.

Outlook: Price Falls to Slow After Returning to Pre-War Levels

Now that prices in Europe have fallen below or are nearing pre-war levels, we expect WoW declines to decelerate. In part, this is due to the return of Chinese manufacturing activity, which should limit Chinese sheet exports and boost global prices, making material from abroad less attractive. The recent implementation of India’s export tariff will also help contribute to price stabilization. Meanwhile, prices in the US still have further to fall before reaching their pre-war average, and we only expect price declines to slow down once those levels are reached.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com