Market Data

July 22, 2022

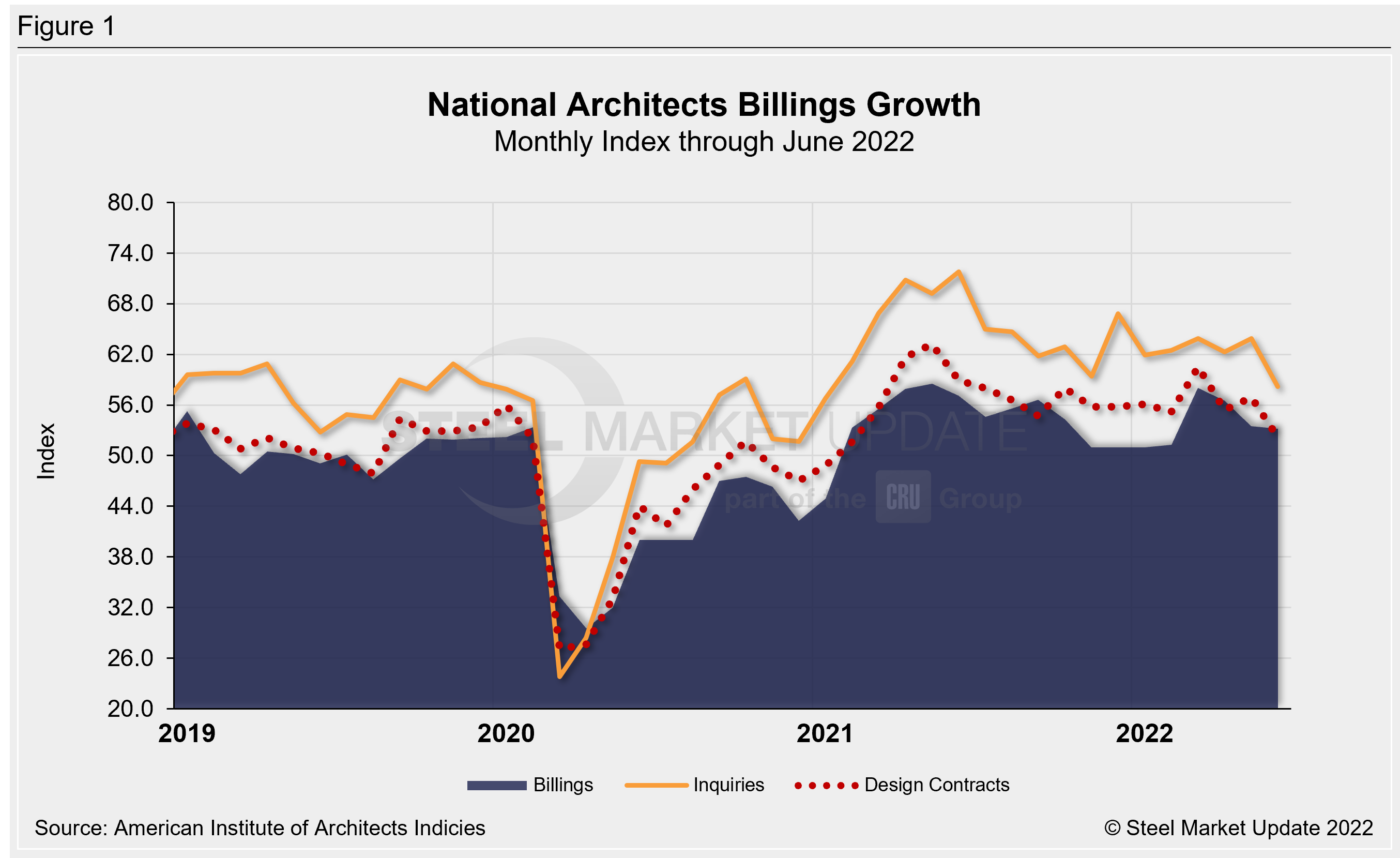

ABI’s Pace of Growth Moderates in June

Written by David Schollaert

Demand for design services from architecture firms in the US continued to grow in June, though at a modest pace. The June AIA Architecture Billings Index (ABI) score was down marginally month-on-month (MoM) but marked the 17th consecutive month of growth following the pandemic-induced downturn in 2020.

The June ABI registered 53.2, down fractionally from May’s score of 53.5, according to the latest report from the American Institute of Architects. The ABI is an advanced economic indicator for nonresidential construction activity with a lead time of 9–12 months. A score above 50 indicates an increase in activity and a score below 50 indicates a decrease.

Most architecture firms reported growing business conditions, but still-rising inflation, higher interest rates, and a continued shortage of building and construction materials mean the future view is less certain, the report said.

Indicators of future work remained firm, driven by the value of new design contracts and extended backlogs.

Both design contracts and new project inquiries moderated in June but continued to show growth. New project inquiries posted a score of 58.2, down 5.7 points from May’s score of 63.9. Design contracts came in at 52.2 points, declining 4.7 points from May’s score of 56.9. This was the slowest rate of growth for both since the recovery began in early 2021.

Backlogs, which had been growing at a torrid pace recently, declined slightly, from an average of 7.2 months at the end of the first quarter of 2022, to an average of 7.0 months at the end of the second quarter. Most firms still have a robust supply of work in the pipeline, despite the modest decline quarter-on-quarter.

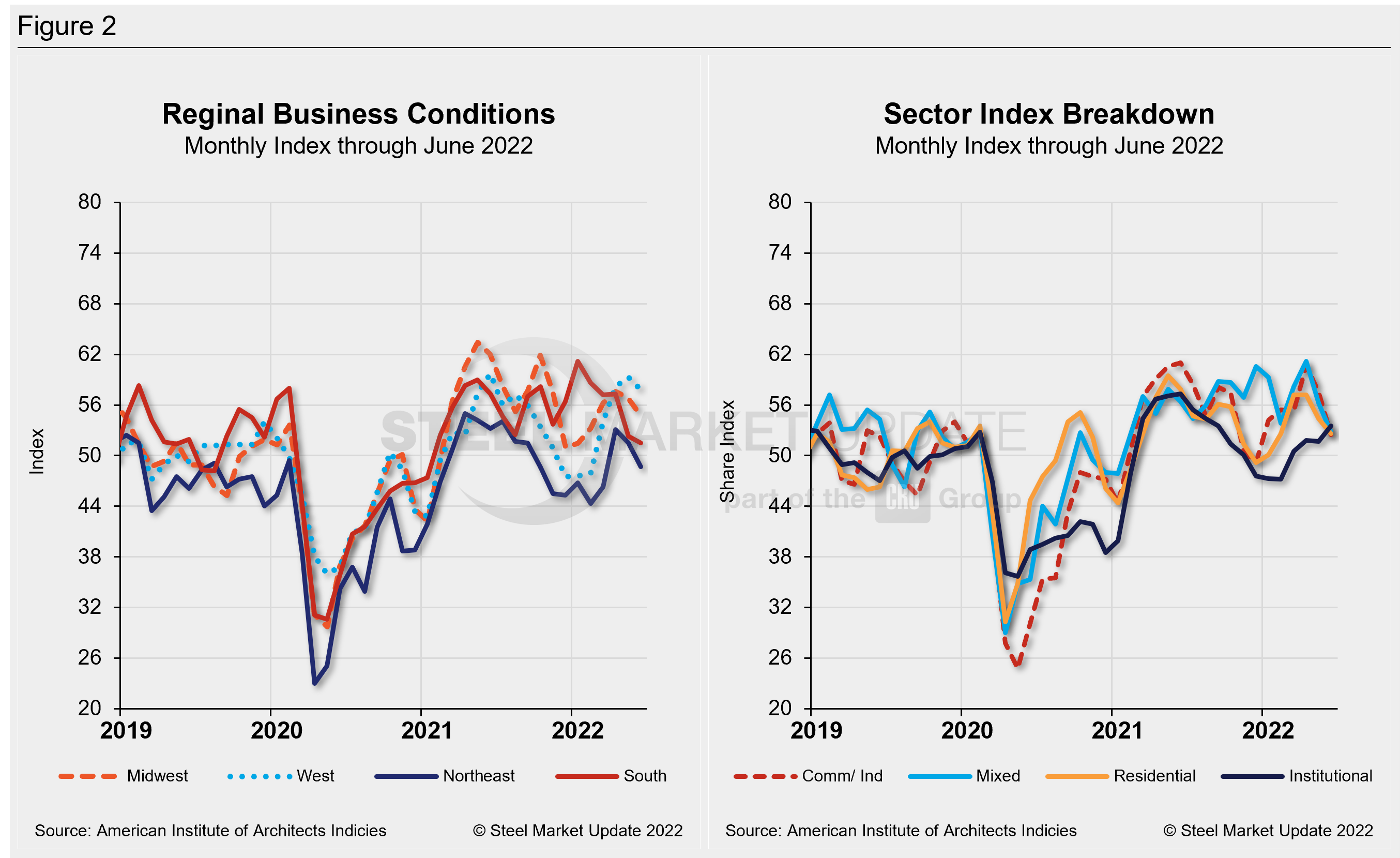

The MoM changes in scores for regional billings—which, unlike the national score, are calculated as three-month moving averages (3MMA)—moderated in June (Figure 2). All four regional billing scores lost ground, with the Northeast slipping below 50.0. Billings in the South decreased 0.8 points, while billings in the West and Midwest declined by 1.5 points and 2.0 points, respectively. Billings in the Northeast saw the widest decline, shrinking by 2.8 points MoM in June.

All four of June’s sector billings scores remained above 50.0 while three out of four decreased from their May values. The commercial/industrial sector fell by 5 points and the multifamily residential score decreased by 1.8 points. The mixed-practice sector decreased by 3.4 points, while the institutional sector expanded by 1.8 points. Like the regional billings scores, sector billings scores are also calculated as 3MMA and are displayed in Figure 2.

“Ongoing project activity at architecture firms as well as new work coming online remains strong, pushing project backlogs up to seven months on average nationally,” said Kermit Baker, AIA’s chief economist. “In spite of heavy workloads, employment at architecture firms has stabilized, suggesting that adding new employees is becoming even more challenging as the building construction sector continues to recover.”

Key ABI highlights for June include:

- Regional averages: West (57.8); Midwest (54.8); South (51.5); Northeast (48.7)

- Sector index breakdown: Institutional (53.5); mixed practice (52.8); multi-family residential (52.6); commercial/industrial (52.5)

Regional and sector scores are calculated as three-month averages. Below are three charts showing the history of the AIA Architecture Billings Index, Reginal Business Conditions, and Sectors.

An interactive history of the AIA Architecture Billings Index is available on our website. Please contact us at info@SteelMarketUpdate.com if you need assistance logging into or navigating the website.

By David Schollaert, David@SteelMarketUpdate.com