Analysis

September 25, 2022

US Light Vehicle Sales Improved in August

Written by David Schollaert

Steel Market Update is pleased to share this Premium content with Executive members. For information on upgrading to a Premium-level subscription, email Info@SteelMarketUpdate.com.

US light vehicle (LV) sales grew in August, coming in at 1.13 million units, unadjusted. Last month’s total was a 3.9% increase year-on-year (YoY), the US Bureau of Economic Analysis (BEA) reported.

The YoY gain was the first since July 2021. The comparison was helped by weak sales a year ago and by an extra selling day last month. Volumes have been remarkably steady for the past three months, with sales rounding to 1.13 million units in each, perhaps hinting at the supply problems still restricting the market. That said, inventories grew to 1.27 million units by the end of August, a 10.2% increase month-on-month (MoM).

Annualized, though, last month’s results brought US vehicle sales down 1.1% MoM to 13.2 million. The reading also came in slightly below the consensus forecast of 13.3 million. The pullback in August sales was a disappointment, particularly coming after two consecutive months of gains.

The daily selling rate was 43,392, down 0.7% from last August’s reading of 43,706. Through the first eight months of the year, sales have totaled 9.0 million units – down 15.3% from 2021’s year-to-date measure.

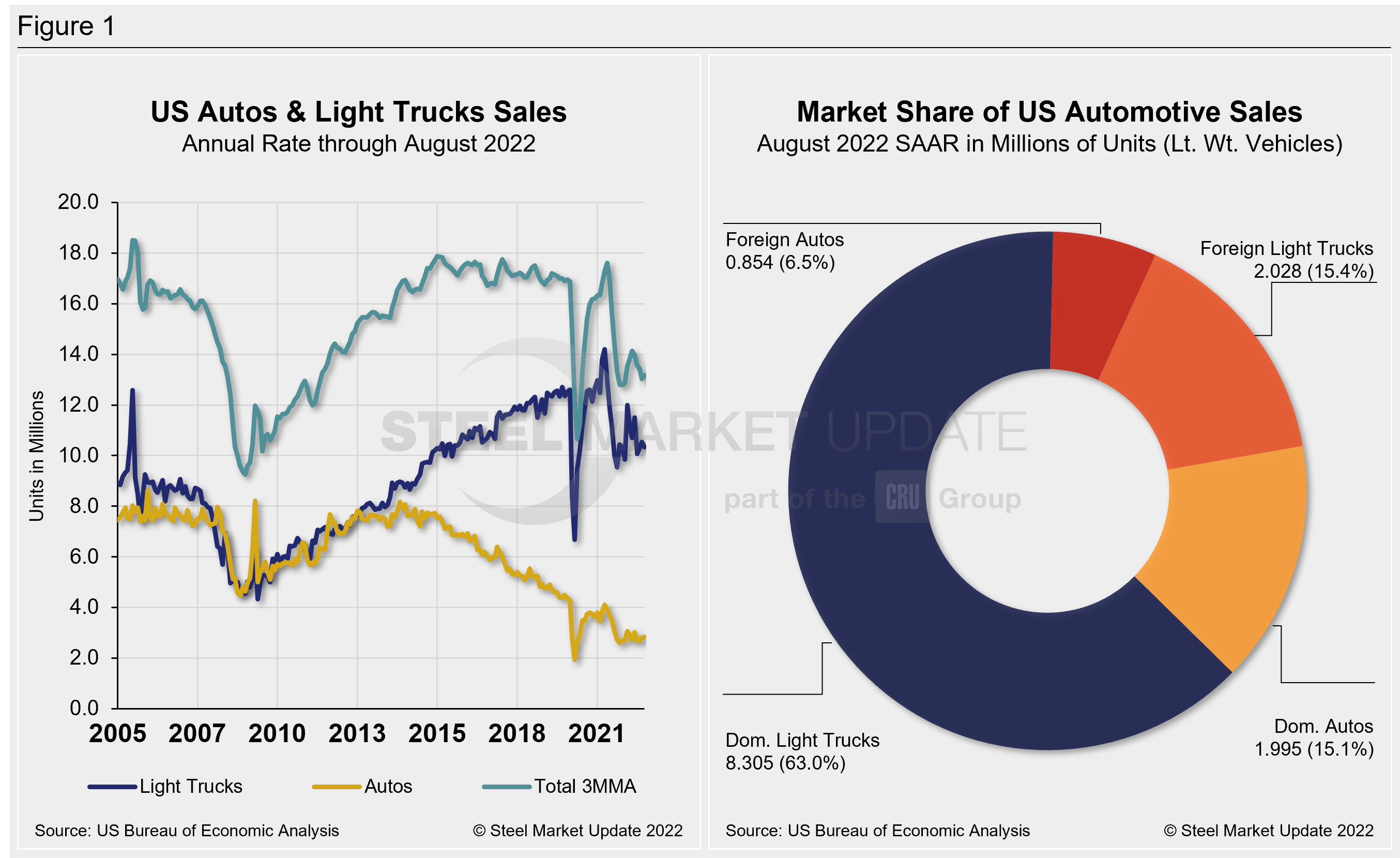

The pullback in annualized sales in August was entirely concentrated in the light trucks (-2.0% MoM) segment, while passenger vehicles (2.2% MoM) recorded a modest gain. Light trucks accounted for 78.7% of last month’s sales – up 2.0 percentage points from August 2021.

Below in Figure 1 is the long-term picture of sales of autos and lightweight trucks in the US from 2005 through August 2022, as well as the market share sales breakdown of July’s 13.3 million vehicles at a seasonally adjusted annual rate.

The current inventory mix heavily favors more expensive and less fuel-efficient vehicles, helping to limit the buyer base. The pullback in last month’s sales of light trucks seems to corroborate this idea. Until there is further normalization in production – bringing more affordable vehicles to market – sales are expected to remain restrained, said LMC Automotive.

The combination of elevated prices, rising interest rates, and record low incentive offers have put a serious dent in vehicle affordability. While pent-up demand remains, current conditions risk demand destruction.

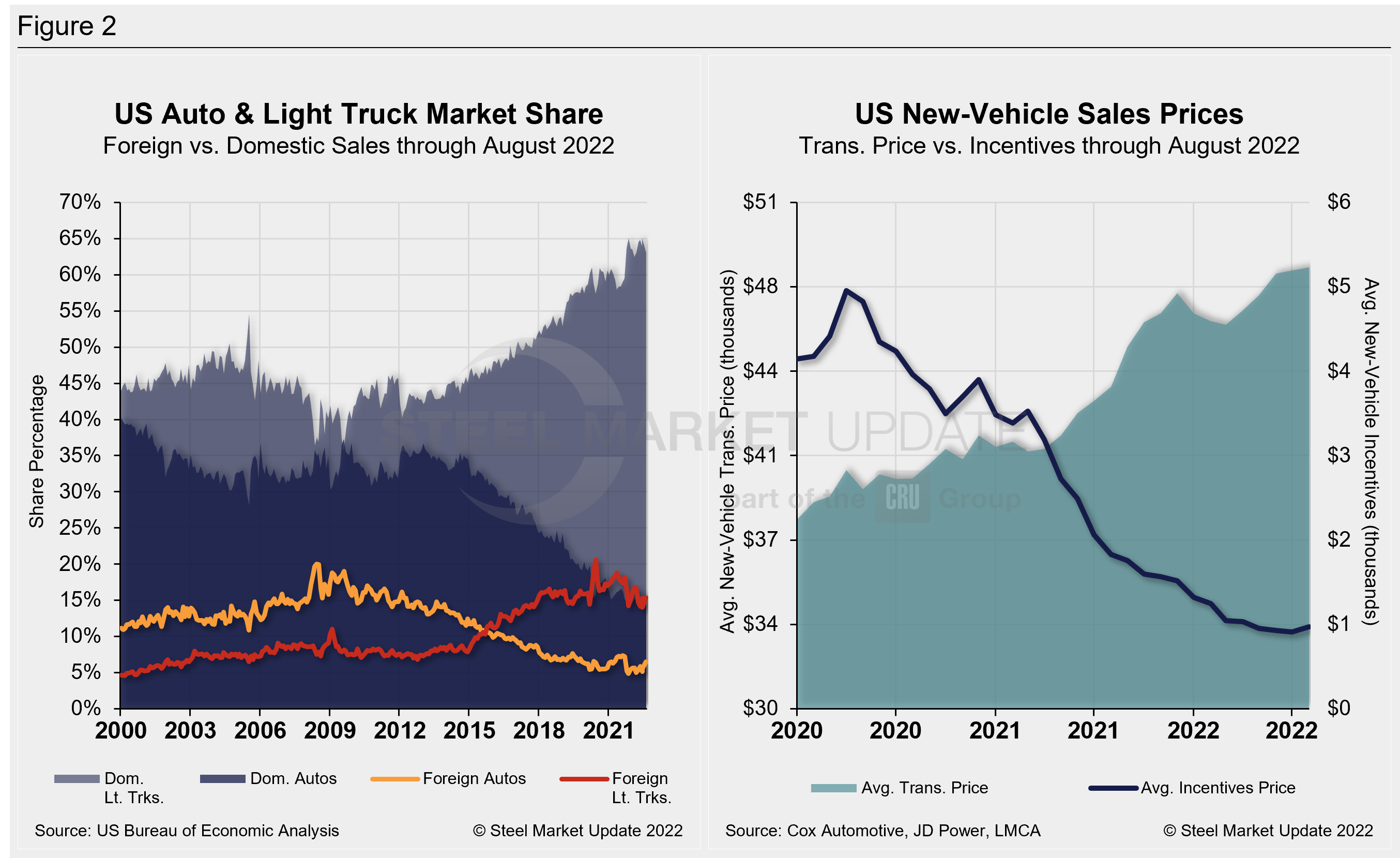

New-vehicle ATPs rose to $48,301 in August, rising for the fifth straight month and hitting a new record high. Prices were up just 0.2% (+$119) in August versus the prior month and are 11.4% (+$4,946) above the year-ago period, according to Cox Automotive data.

Incentives edged up slightly to $969 in August after reaching a record low of $911 the month prior. The slight improvement in incentives was the first gain since March 2021. But despite the 6.4% increase MoM, incentives remained below the $1,000 mark for the fourth straight month, just roughly 2% of the average transaction price. Incentives are down 47%, or $861, YoY.

In August, the annualized selling rate of light trucks was 10,333 million units, down 2% versus the prior month but still 3.2% better YoY. Auto annualized selling rates reversed during the same periods: up 2% but down 7.6%, respectively.

Figure 2 details the US auto and light-truck market share since 2010 and the divergence between average transaction prices and incentives in the US market since 2020.

Canada and Mexico saw opposing dynamics in August.

Canadian LV sales are estimated to have fallen by 12.9% YoY in August, to 128,000 units. The selling rate is thought to have declined to 1.44 million units annualized for last month, from 1.58 million units annualized in July. The result comes as the market continues to struggle against low inventory, while interest rates are rising and inflation is elevated.

Mexican auto sales grew by 16.1% YoY in August to 91,000 units. That is their strongest YoY gain since June 2021. The selling rate accelerated to 1.08 million units annualized, from 1.04 million units annualized the month prior.

Editor’s Note: This report is based on data from the US Bureau of Economic Analysis (BEA), LMC Automotive, JD Power, and Cox Automotive for automotive sales in the US, Canada, and Mexico. Specifically, the report describes light vehicle sales in the US.

By David Schollaert, David@SteelMarketUpdate.com