Overseas

February 7, 2023

CRU: Will Nat Gas Have a Role in Europe's Commodity Production?

The outbreak of war in Ukraine triggered an energy crisis in Europe. Gas and consequently electricity prices soared and remain high. European production of commodities such as ammonia, aluminum, and zinc which require significant energy and/or natural gas were and remain disrupted to differing degrees.

Natural gas is supposed to be a ‘transition fuel’ in the process of decarbonizing the energy system, akin to hybrid cars for tailpipe emissions. Yet the recent high price of gas has led to some gas-to-coal switching, increasing emissions.

In this uncertain environment, what will be the long-run role of natural gas in European commodity production? We look broadly and briefly at the gas market itself and commodities covered by CRU, including metals and fertilizers.

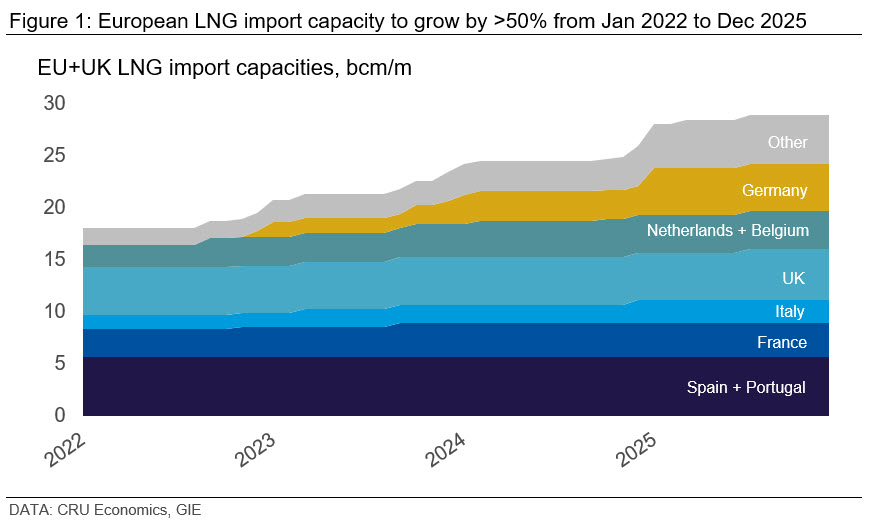

The EU has responded to the huge reduction in Russian pipeline gas by reducing industrial gas demand, allowing member states to exert some control over energy pricing, sourcing more LNG, and expanding LNG import capacities.

The EU also plans to coordinate gas import purchases, introduced a ‘price cap’, and is planning to further expand LNG regasification capacities to substitute for Russian pipeline gas imports.

While we expect high natural gas prices to remain an issue in 2023, European LNG import and global LNG export capacities expansions should help stabilize prices. European gas consumption will likely rebound from late 2022 levels over the next several years.

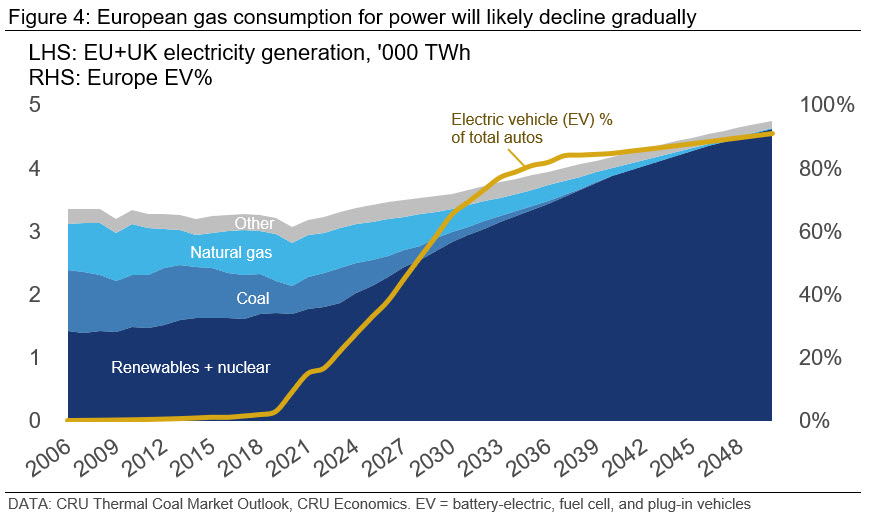

Approximately 25% of the 410 bcm total 2021 EU natural gas consumed was for electricity generation. In contrast to industrial demand, which dropped sharply, gas consumed for power did not significantly fall in 2022.

Gas had to make up the shortfall from drought-hit hydro and maintenance-hit nuclear power generation, with some subsidies also boosting demand.

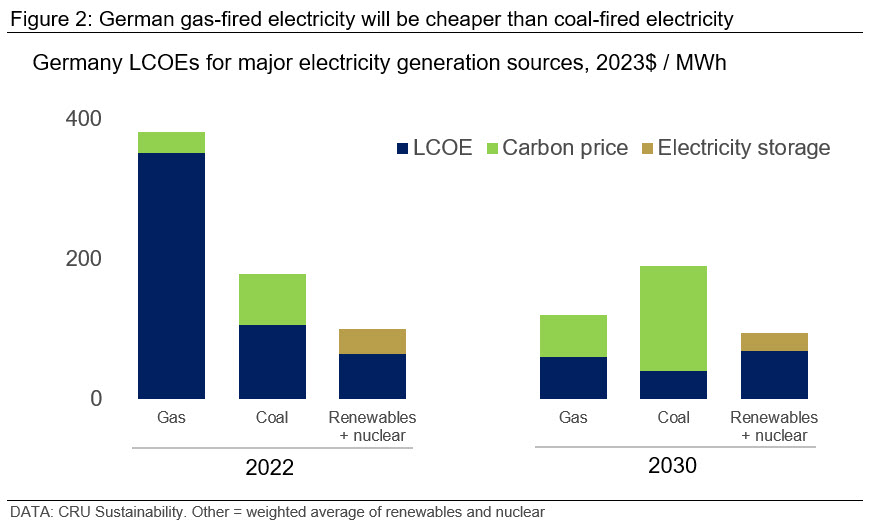

Coal was cheaper (per MWh) than gas in parts of Europe in 2022, leading to some gas-to-coal fuel switching. However, as European natural gas prices ease this year and in coming years, gas will again be and remains cheaper than coal when carbon prices are considered.

This will likely reverse current fuel switching. Renewables prices will remain cheaper than fossil fuel electricity generation.

CRU calculates levelized costs of electricity (LCOE) for different power sources across many regions. These LCOEs take account of capex, opex, and financing costs, as well as the direct cost of any fuels consumed to make power. We also forecast carbon prices, which can be added to give a holistic comparison of cost.

Our LCOE data for Germany illustrate these trends for power generation in Figure 2. Gas should regain its cost advantage over coal, as prices converge and carbon prices increase.

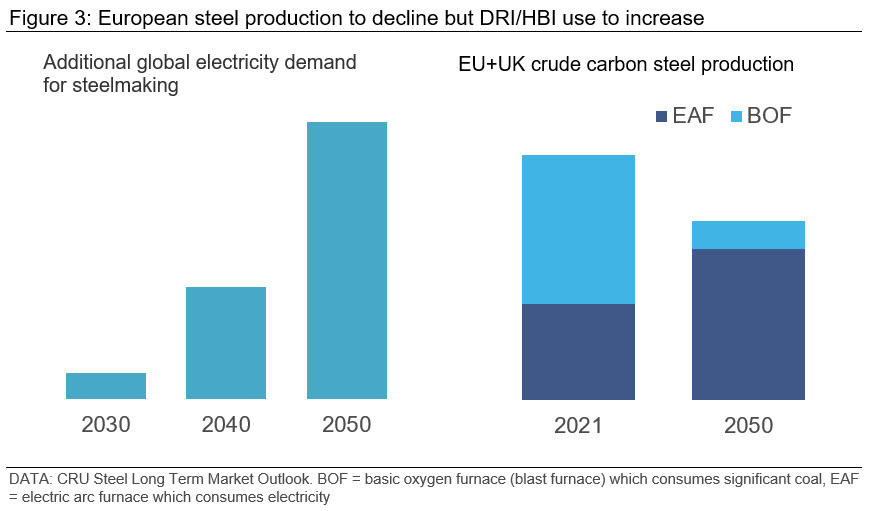

Looking forward to 2050, total European electricity generation will need to rise to meet greater electrification. Electricity will rise with greater adoption of EVs and electronic products and more industrial process electrification. For instance, steel production will become more electrified globally and in Europe by using more of the electrified arc furnace (EAF) process as scrap recycling increases and use of the coal-intensive blast furnace process declines.

At the same time, European electricity generation will become greener. Rising electricity demand may prolong use of gas and other fossil fuel power generation, but cost economics will favor renewables. Renewables will be a large slice of a bigger pie.

The European efforts to address high gas prices should make it cheaper than coal again. Gas will therefore be used as a transition fuel of sorts as more costly and higher-emission coal is phased out more rapidly.

Much of European commodity production, including primary aluminum, zinc, and some steel, already consumes electricity instead of purchasing gas. Gas will also be a transition fuel here by extension.

Most EU industrial direct gas consumption is for energy. This consumption will be under pressure if not already. Many lower- and medium-temperature industrial processes will likely be electrified. Some production may close or move abroad. However, some production may only show limited change. For instance, much of aluminum recycling may continue to directly consume gas whereas furnaces are often cheaper to run directly on gas and expensive to replace with alternative power-consuming primary production facilities.

Direct gas consumption by secondary European aluminum production may therefore depend on how much facilities change, in addition to how much recycling increases.

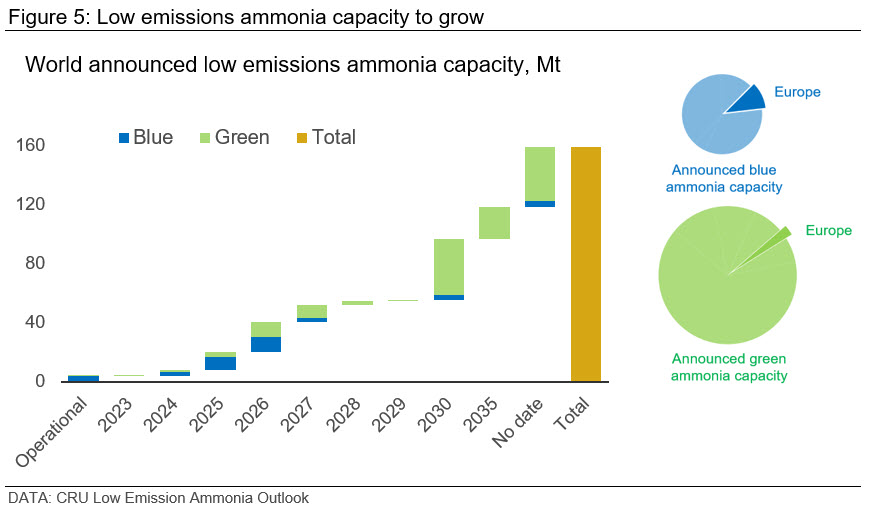

Natural gas is also used as an industrial feedstock. A small but very significant amount of non-energy gas is consumed in the EU. Most of the gas consumed as feedstock in Europe ends up in chemical production, particularly ammonia, but also acetylene, methanol, and others. Ammonia is primarily made by extracting hydrogen from natural gas feedstock and is mostly used in fertilizer manufacture and as a chemical intermediate. Ammonia production in the energy transition is set to continue using gas feedstock but with carbon capture and storage to produce ‘blue ammonia’, before use of ‘green hydrogen’ (electrolyzed from water using renewable power) as feedstock to produce ‘green ammonia’ increases.

Europe will likely consume slightly more hot-briquetted iron (HBI) and direct-reduced iron (DRI) instead of iron ore in the long term for steel production. HBI and DRI production consumes natural gas as feedstock. However, Europe will likely import much of this HBI and DRI.

The outbreak of war in Ukraine disrupted Europe’s natural gas markets, raising questions about the role of natural gas in the energy transition. After some adjustments, Europe will likely continue using natural gas for power generation and industry, with a gradual move towards other sources of energy and feedstock. Natural gas will therefore remain an important transition raw material for European commodity production.

Editor Note: CRU has expertise in commodity markets relevant to the European energy transition, including steel, coal, and fertilizers, as well as new capabilities in sustainability and carbon markets. We are also available to discuss economics and energy markets. Please contact us for more information about these areas and products.

This article was originally published on Feb. 3 by CRU, SMU’s parent company.

By CRU Power Sector Lead Analyst, Glen Kurokawa from CRU’s Economic Insight

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com