Market Segment

February 12, 2023

Final Thoughts

We are in moving into an interesting period here for spot markets for hot rolled coil.

Steel mills are driving hard for a further rally in the face of what appears to us to be weaker year over year demand and an overall challenging macro-economic backdrop, with interest rates likely to create headwinds this year as efforts to battle inflation continue.

This backdrop has not discouraged steel producers in the US, who continue to make price increase announcements with regularity and, so far, have succeeded in reversing a trend of falling prices that had been in place since last fall.

They have even sustained a rally despite no apparent increase in real spot demand thus far, something that we have seen before. Usually, the culprit is at least in part raw materials.

That was the case a year ago with the pig iron scare that ensued following the immediate Russian invasion of Ukraine. This year, scrap prices have been on the upswing, which has no doubt helped mills in some respects.

But as I have often said in covering these markets, there is no fundamental connection or requirement that smaller mill margins necessarily justify higher prices. If that were the case, prices would never fall below breakeven production costs for the mill – which of course we have seen happen several times over the last decade.

There is also a clear element of fear at work here. Mills will naturally look to exploit the possible return to historic high levels.

Spot markets bottomed out in November of last year. As the chart below shows, the dead low of $682/ton ($34.10 per cwt) for the March ’23 futures was set all the way back on November 9. It’s been a pretty steady climb higher since that low, reaching $860/ton last week, more or less pricing in current mills offer levels.

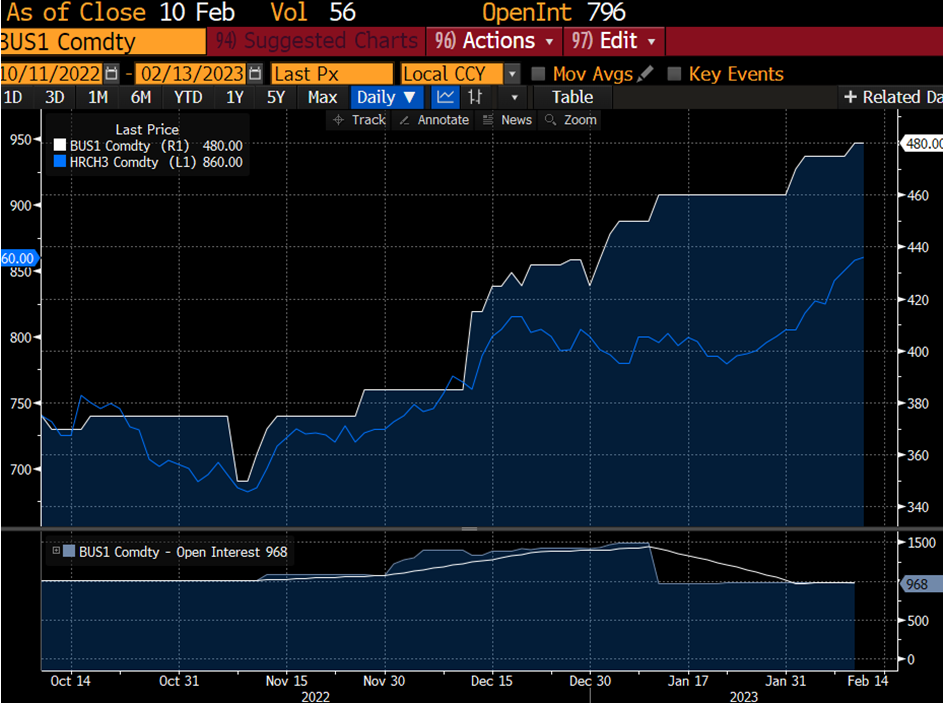

We mentioned the importance of raw materials. Look how closely the trend in busheling (BUS) has followed HRC, something that frankly had become largely disconnected on the upswing higher.

Does this spell a return to a more normal scrap/coil market connection, or a temporary aberration? It is still too early to say, but mills will continue to use raw material strength as a justification for price increases so long as the market will tolerate it.

BUS prices have reached $480/ton for March, up nearly 30% from the lows last fall. That fact sort of snuck up on the market, which was trading well below $400/ton as recently as mid-December, as you can see in the chart below.

Here is the thing that is most interesting to me in this rally as I alluded to at the outset: demand is not good. UBS projected that apparent steel demand had cratered to a 23-month low into the year-end 2022 and that year-over-year demand signals continue to look negative for flat rolled.

Demand is projected to decline year over year even more significantly in the second half of 2023. That is consistent with expectations of a higher rate environment and the lag effects of prior increases.

This demand outlook is precisely why the curve has moved into such a steep backwardation, despite months of persistent contango. The discount for July is massive and has grown massively since the outset of the year, when we were trading at a $25-30/ton premium! The white line below is March 2023 futures, the blue is July ’23, and the red December ’23.

What happens when/if the market cracks this year? Is it likely to fall from $850/ton to $780/ton? Or $580/ton? That is the question that interests us most. It may largely depend on how fast and how hard the mills will look to push the spot market in the coming week.

Editor’s note: Spencer Johnson has been trading HRC futures for 14 years at StoneX (previously FCStone).

Spencer O. Johnson

LME/Ferrous Trading

StoneX Financial Inc.

O- 212-379-5492

Spencer.johnson@stonex.com