Analysis

March 5, 2023

Final Thoughts

Written by Michael Cowden

A sheet supply squeeze is on and, according to some market participants, chances are it’s only going to get tighter.

There is no one thing, a war or pandemic, that’s causing the squeeze this time. Instead, it’s a litany of comparatively smaller events that combined have created some real havoc.

You know that list by now: new capacity in the US being slow to ramp up, production problems at AHMSA, low imports, etc. Here are a couple new ones to add to that list.

Several key locks along the Illinois River system, which connects Lake Michigan to the Mississippi River, will be closed from approximately June 1 through Sept. 30 for maintenance. The US Army Corps of Engineers has the details here.

The Illinois River is a key route for everything from corn and soybeans to steel and scrap. Market contacts have told me that the lengthy closure could slow steel imports moving upstream from the Gulf Coast and scrap moving southbound to southern electric-arc furnace (EAF) mills. That might delay or soften any price correction stemming from imports arriving this summer. It’s also possible that some EAFs might buy more scrap now to get ahead of the lock closures, they said.

Also, several of you have noted the potentially widespread impact of the bankruptcy of Radnor, Pa.-based Phoenix Services. The company manages everything from scrap, to slag, to melt shop equipment for several top steelmakers – among them, Nucor.

The Philadelphia Inquirer has a good writeup of the situation. Also, we’ve been told that Nucor might not be the only steelmaker impacted by the bankruptcy. But details of the Nucor-Phoenix Services relationship have been made public because of legal wrangling between the Charlotte, N.C.-based steelmaker and private equity firm Apollo Global Management, which controls Phoenix Services.

A couple notable points from the Inquirer article: ~160,000 tons of slag and other waste have “piled up” at Nucor mills. Nucor, according to the Inquirer, has said the situation could compel it to trim output, something that could lead to “potential shortages or price hikes.” (Nucor did not respond to a request for comment on the matter.)

Neither of these events individually is enough to rock the market. But I wonder whether one of them might be the proverbial straw that breaks the camel’s back.

And those are just the issues we know about. Here are a couple I’ll be keeping tabs on in the weeks ahead.

For starters, February service center inventory data, which we’ll release later this month. Why? We saw inventories decline and shipments rise in January. If that trend continues, do we risk getting to a point, as we did in 1H 2021, where lead times are roughly on par with months of supply?

Also, what is the contract/spot mix this year compared to last year? I ask that because there was a consensus in 2H 2022 that the market would return to something resembling normal cyclicality in 2023. That meant it made sense to scale back on contract tons and ride the spot market. How many people did just that? And if more companies are relying on the spot market, could that explain some of the volatility we’ve seen over the last two months?

I was discussing the current price spike with an industry contact. He suggested we’re seeing the classic stages of grief – about expectations for 2023 being so wildly different from reality to date. Recall those stages are denial, anger, bargaining, depression, and acceptance. Based on feedback we’ve received, I think it’s fair to say we’re still in the first three stages.

I’ll set aside for a moment the discussion of whether US mills will get the $1,150 per ton base price for HRC some announced last week. The way things are going, the new target base price might be higher still by the time you read this column.

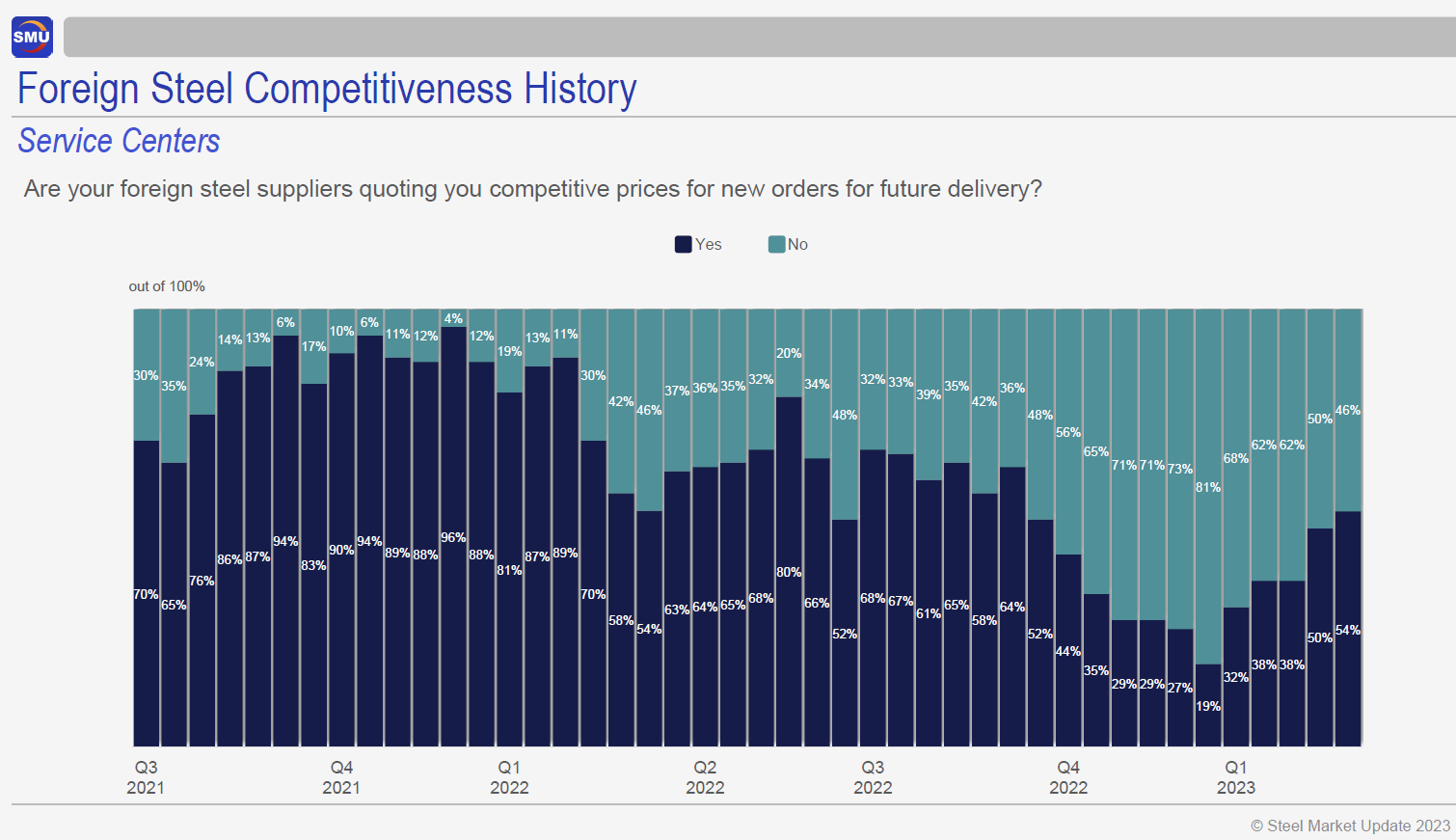

And I’m not sure I see any end to the volatility any time soon. Supply squeezes can be fragile things. What happens if/when AHSMA resumes normal production or when new capacity finally ramps to its full potential? Also, we’ve seen an uptick in the number of steel consumers reporting competitive import pricing. See the chart below, for example.

Fifty-four percent of service center respondents say import pricing is competitive with domestic offerings now, up from only 19% late last year. Any material ordered now might not arrive until this summer. But what happens when it does arrive?

Finally, I’ll leave you with one from the way-back machine, this one from June 2007 at one of the first big industry conferences I attended. I recall Lakshmi Mittal, not far removed from his hostile acquisition of Arcelor, saying two things (1) that steel’s success hinged on customer service and (2) that steel futures had no future.

Futures, it turned out, did have a future – even if it took a while for the market to warm to them. What about customer service?

OK, perhaps that’s not fair. What about supply chains might be a better way to put it. Are prices so much more volatile now because it serves the interest of various industry players? Or are they volatile in part because the supply chain has yet to adapt to a post-Covid, post-Ukraine war, high-inflation reality? I’d be curious to know your thoughts.

By Michael Cowden, michael@steelmarketupdate.com