Prices

March 12, 2023

CRU: Turkish Rebuild Plans Boost Metallics Prices

Written by Puneet Paliwal

By CRU Senior Analyst, Puneet Paliwal, from CRU’s Scrap, DRI/HBI & Pig Iron Monitor

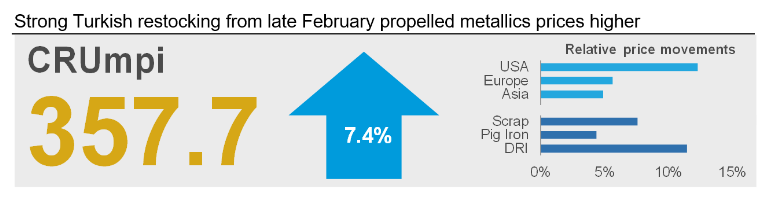

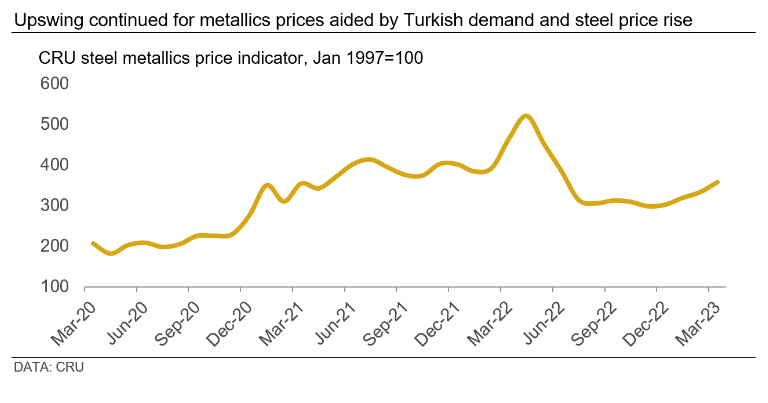

The CRU metallics price indicator (CRUmpi) for March rose by 7.4% month on month (MoM), to 357.7, which is its highest value since June 2022.

Strong Turkish buying of scrap and pig iron since the second half of February is the key factor that led to metallics price increases worldwide. These prices have also found the support of recent spikes in North American and European steel prices, particularly that of sheet.

Meanwhile, supply of metallics is on a gradual path to recovery, especially with scrap collection and processing gaining momentum across key supply regions, aided by current high prices. Supply is likely to catch up with demand in Q2, but fresh demand from Turkish reconstruction efforts will keep prices supported at much higher levels than our previous expectation.

Prices of metallics across the globe have either moved up or stayed stable MoM in March. The primary support to metallics prices came from the developments in the Turkish market. The tragic earthquakes that hit the country in early February had initially halted steel and scrap market activity. Since the second half of February, however, scrap buyers came back to the market with restocking demand, concluding deals at prices higher than those in early February. This was driven by the speculations around strong steel demand and production growth as the country initiates massive reconstruction efforts in the affected regions. We have published an Insight to assess these efforts: Earthquake reconstruction will be a big deal for steel demand.

Speculative buying was such that it caused HMS 80:20 scrap import price to rise by $32 per ton, to $450 per ton CFR, over the past three weeks in Turkey, further leading to a rebar price rise of $45 per ton, to $765 per ton, in the past week. This opportunity to promptly pass on cost changes to consumers, while gradually raising margins, has encouraged Turkish steelmakers to book larger volumes of scrap and pig iron imports over the past few weeks, thereby pushing prices higher in other markets as well.

In the US, trades were still being settled in the scrap market at the time of writing, but scrap prices have moved higher by $50-70 per long ton. Supply of both prime and obsolete grades continues to remain limited, while export demand to Turkey has increased, particularly for supplies from the northeast. Meanwhile, domestic steelmakers also have healthy buy programs given the support provided by the recent spike in finished steel prices, particularly sheet. Moreover, the price spread between US pig iron and prime scrap has narrowed since its peak in 2022 Q4, encouraging mills to purchase more pig iron, leading to a reduction in inventories as supply continues to remain tight from Ukraine and Brazil. This has caused US pig iron prices to also move up by $30 per ton MoM to $555 per ton CFR NOLA.

In the European Union (EU), Turkish restocking demand pushed a $20 per ton rise in scrap prices across all grades as well as for pig iron. Turkish buyers are bidding higher for European scrap, which has negated the impact of weak domestic end-user demand conditions for steel as high inflation continues to persist in the region. Construction sector activity has stayed subdued pulling longs prices lower, although sheet prices have found some support from restocking and supply tightness. Meanwhile, CIS-origin pig iron exports continue to make their way into the EU, particularly in Italy and Poland, despite overall sanction threats regarding trading with Russia.

In the Asian market, Chinese domestic scrap prices have stayed unchanged MoM as mills with low margins and sufficient scrap supply kept their bids unchanged and waited for industry guidelines from The National People’s Congress and the Chinese Political Consultative Conference (“Two Sessions”). EAF utilization rates have increased sharply in the past few weeks – from 23% in mid-February to 57% in early March – leading to a ferrous scrap consumption rise of 16% MoM. Since domestic supply kept up with demand, prices could remain rangebound.

Meanwhile, in the Southern and Eastern Asian markets, scrap import prices have moved up in line with changes to Turkish prices as key suppliers are largely the same. Key buyers in the region are facing political and economic hardships, which have affected steel demand, production and, thus, demand for metallics. For instance, Southeast Asian steel demand has weakened due to political turmoil and delays in public spending. Moreover, Bangladesh and Pakistan continue to face acute dollar shortages, forcing government to restrict opening of fresh Letters of Credit, which are a key payment method for imported scrap.

Outlook: Weaker Speculation and Higher Supply to Test Scrap Prices

Looking forward, we expect prices of metallics in key regions to continue finding support for the remainder of March, aided by strong order books of leading scrap suppliers. However, we believe that prices will not sustain these elevated levels for long as supply will get seasonally stronger, especially in response to current high prices and margins. One of the key factors which may taper down prices across metallics, particularly scrap, is a development from last week wherein the Turkish government has entered into an agreement with steelmakers to put price caps on finished steel during the reconstruction period to curb speculation.

While finer details of this price control mechanism are still being worked out, what it means is that steelmakers will not be able to raise finished steel prices substantially from here on. Thus, they are likely to start bidding lower for scrap purchases as higher prices of scrap, if not passed through, will squeeze their margins. Given that scrap availability is expected to rise seasonally in key supply markets and the fact that Turkey will be an even stronger volume driver in the coming 12-15 months, buyers may end up dominating near-term scrap price negotiations.

This article was originally published on March 9 by CRU, SMU’s parent company.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com