Analysis

May 17, 2025

Final Thoughts

Written by David Schollaert

The market is giving way, declining, and it might just be the beginning of a steady grind for the next few months. Though that last part is just speculation at this point.

The turmoil from President Trump’s tariff wars is a major component of the shift, but it’s not the only one.

While I would anticipate market sentiment to pivot and improve if all the questions around tariffs were answered, that still leaves us with a few other factors. Like the fact buyers are stocked, demand is pulled back, and the summer doldrums look to have arrived early – and, dare I say, will “wear out their welcome.”

That’s ultimately a recipe for a not-so-enjoyable summer.

There’s a lot of interesting data in this week’s survey results. You’ve probably already caught some of it – mill lead times are down, buyers’ sentiment is also down, and not surprisingly, mills are willing to talk price.

April service center data was also released this week, and make sure you catch our Mill Order Index report. Orders dropped again in April, and service centers are feeling the drag.

There really is a lot to cover from this week’s survey results, so I encourage you to check it out. But here are just a few items that stood out to me (including some direct market comments).

Survey says it’s going to be a downhill ride from here

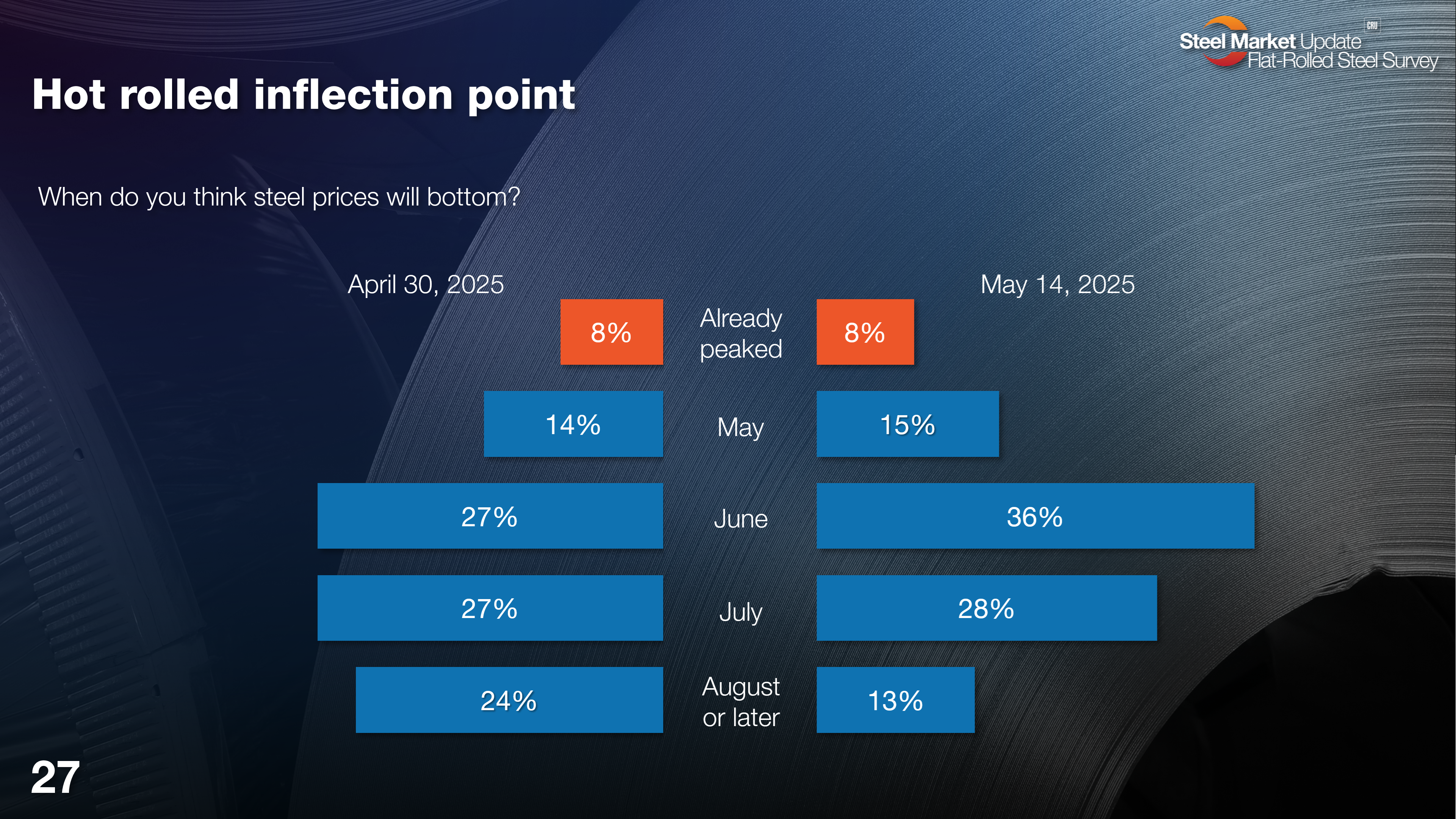

For starters, it was late March when the wisdom of the crowd said prices would peak between May and June – to the tune of nearly two-thirds. Fast forward to now, most expect we won’t reach bottom until summer, with another 41% saying bottom won’t come until July or later. (Editor’s note: You can click on any of the images below to expand them.)

Regardless of how you cut it, market sentiment is we’re in for a steady price decline. If the mills have it their way, it will be a slow grind. We’re already hearing of mills cutting back operating hours and melt schedules to match demand and keep prices as steady as possible.

Here is what some survey respondents had to say:

“Uncertainty prevails.”

“I am not sure.”

“I think prices continue to slide for a bit, just depends on how quick they go down, so either June or July.”

“We don’t see any bottom in sight – no reason to think it’ll turn around until after the summer doldrums.”

“It should bottom in 30-45 days.”

“The mills seem to have a little more control in this environment. Based on that, I’m not expecting a fast decline, but a slow decline that may bottom out in July or August.”

“Mills will adjust capacity to stop the slide.”

“Demand is low and inventories are moving slowly.”

“Lack of automotive demand. Pre-tariff ordering is over, and now real demand will drive the market. US consumers keep setting records for total debt. Can’t afford to buy things.”

How low can it go?

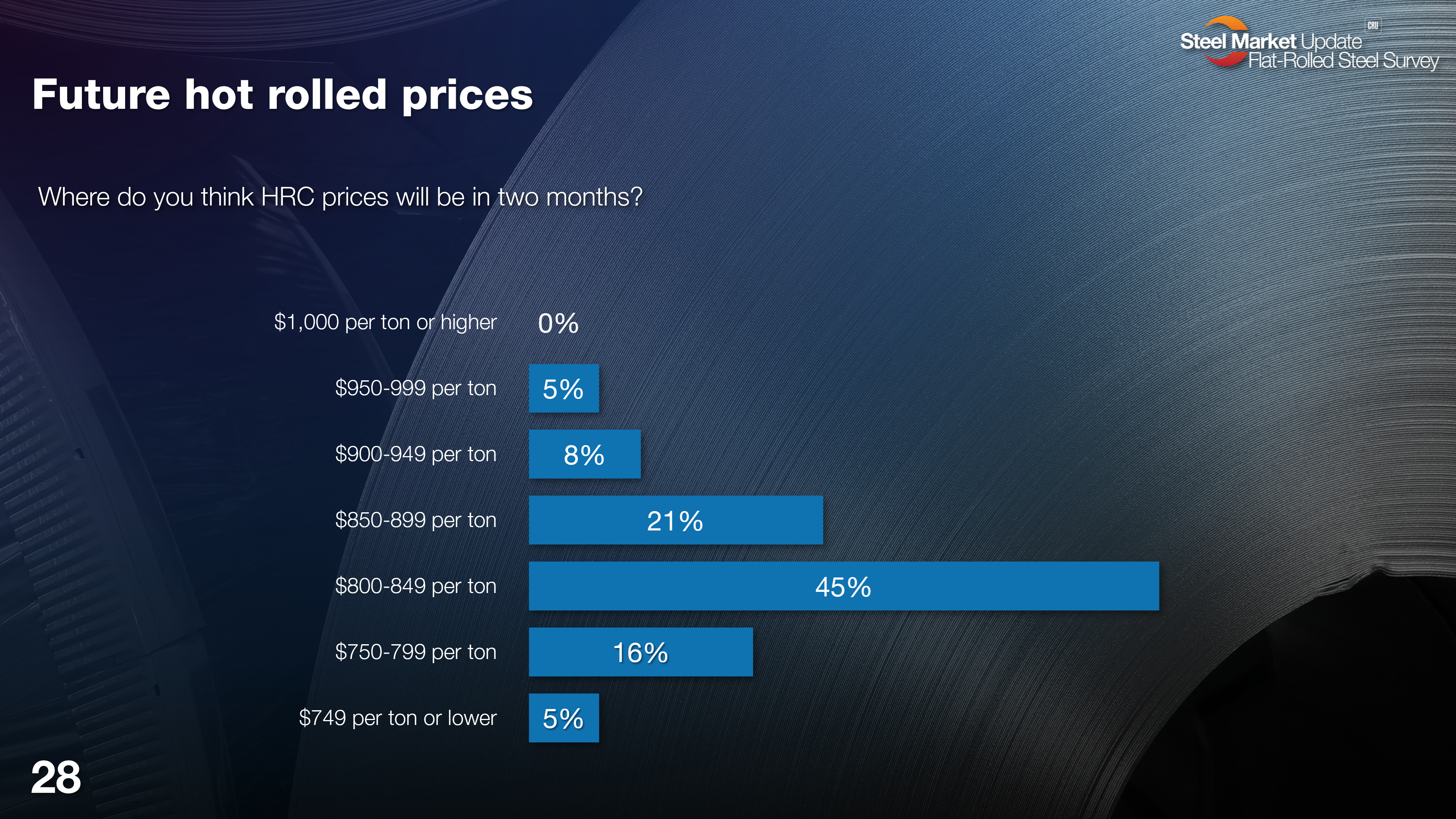

Not surprisingly, the view of where prices will be in two months from now has shifted as well. While a solid 21% of respondents believe prices will be $799/st come July, there’s still a solid 45% that think prices will be roughly were they are now.

But hot rolled coil prices are presently at $845 per short ton (st), according to SMU’s latest market check on May 13. Hot band is down $105/st over the past eight weeks and trending lower.

One could argue expectations might be too good to be true. And that we’ll be sniffing the $700s very soon. But the wisdom of the crowd might indeed be saying we’ll be on the upswing come July. It’s hard to tell, but I’ll let some of the comments speak for themselves:

“Prices will keep adjusting down, but I think $800/st is the physiological bottom.”

“Plenty of steel has already been imported. Demand has not increased. Tariff yo-yo has caused everyone to freeze.”

“I think we get there within two months, not sure it will last long, but seems to be headed down and quick.”

“Soft demand. Reluctant buyers. Low raw material cost. Low energy costs. Decreasing inventories. Could be setting up for a quick rebound when the market starts to rebound in 3rd quarter.”

“I am still forecasting sub-$800/ton by this summer. Demand is still too weak.”

“Right around $900; low inventory today.”

Steel buyers agree… mostly

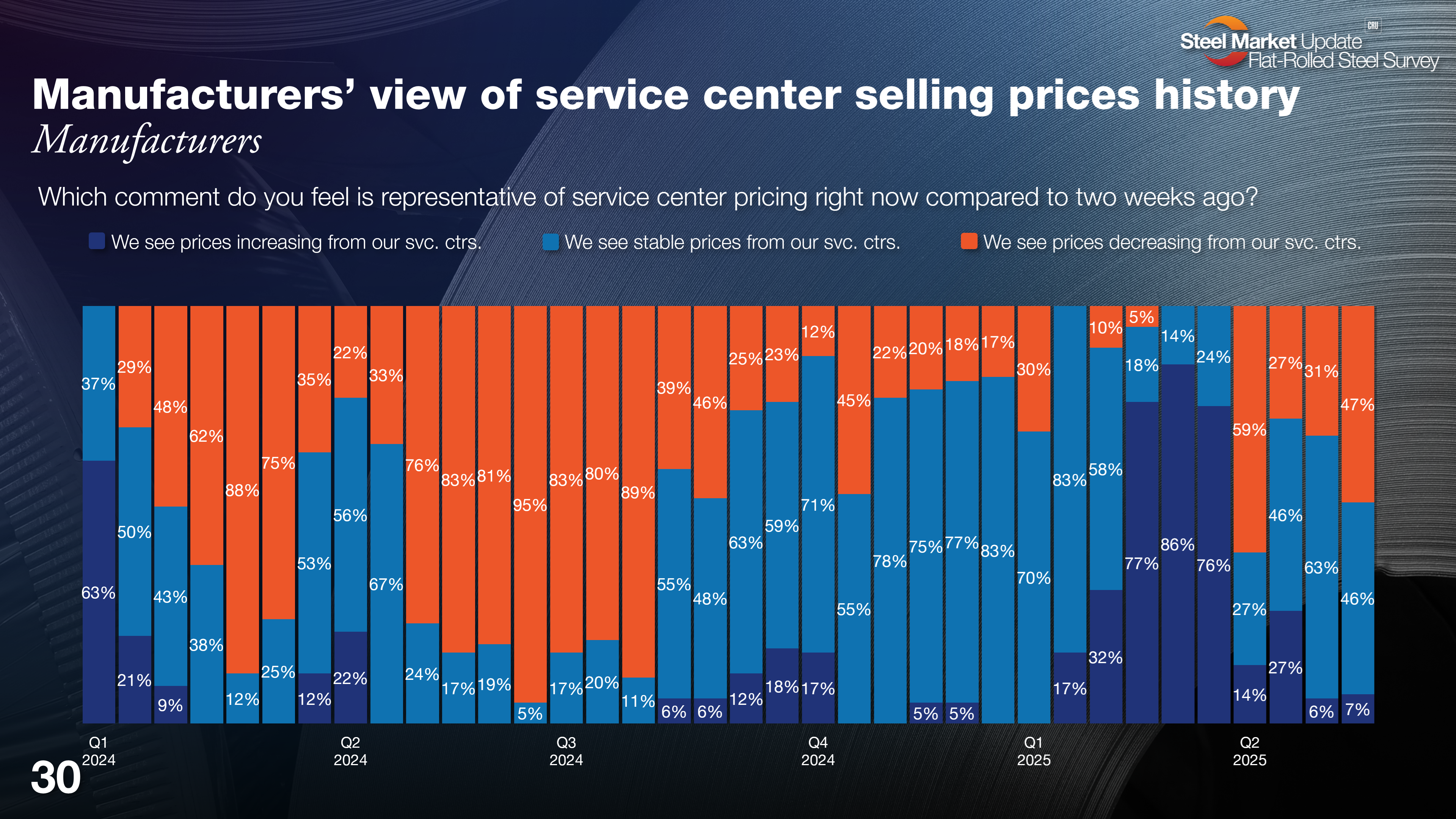

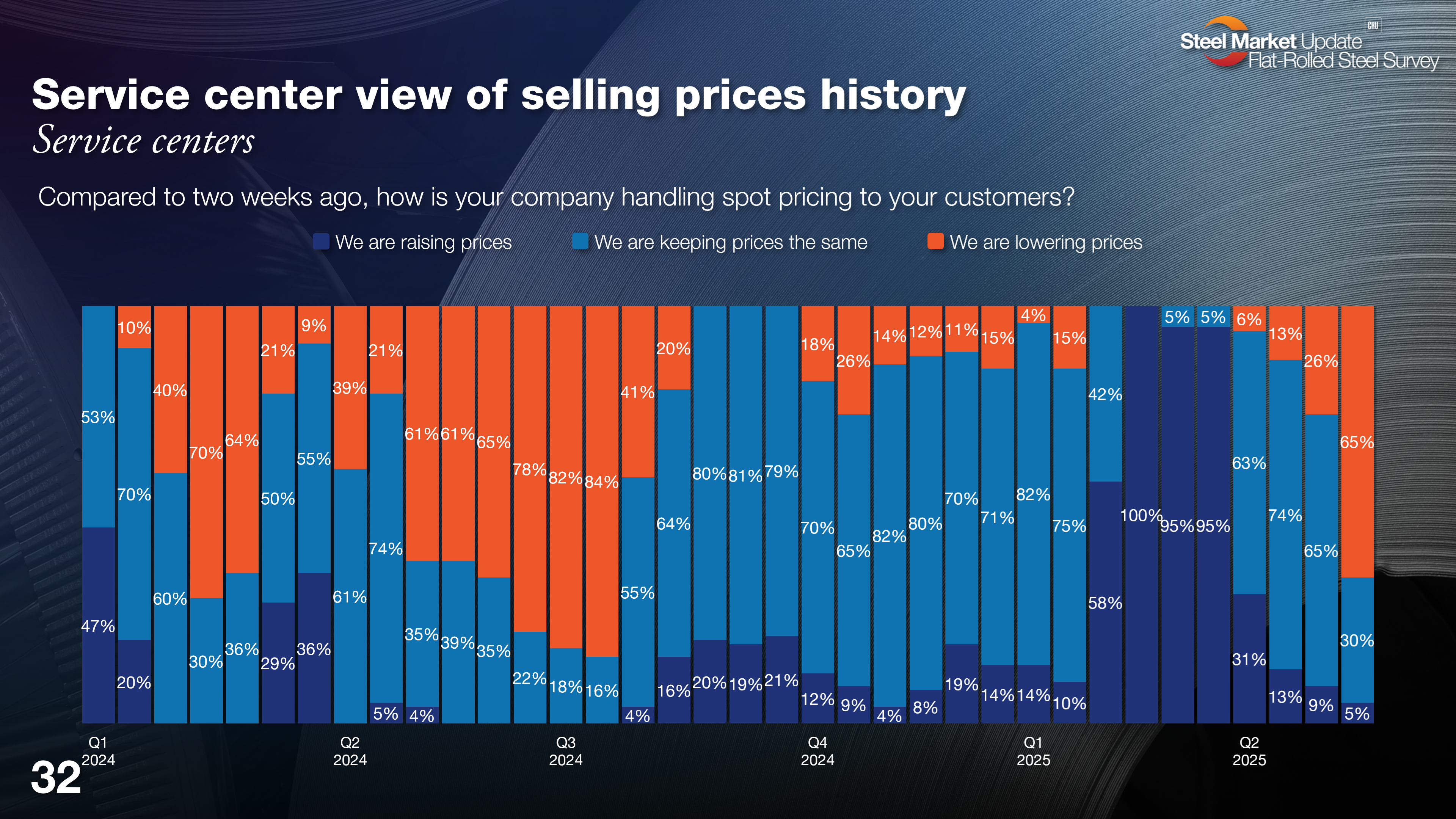

Service centers and manufacturers alike (next two charts) are still reporting a very similar price trend. The pivot we saw in April continues strong. We really haven’t seen a reversal like this in some time.

You know the story. You’ve been living it, but in early/mid Q1, mills began pushing prices higher, backed by tariffs. Buyers pulled forward demand, and they jumped to the sidelines once covered. Buying tailed off, and so have prices. The question now is for how long?

A few comments:

“We’re adjusting based on an order-by-order basis.”

“For the last month or so we’ve seen service centers really take their pricing down, especially on hot rolled.”

“Noticeable competitiveness between service centers.”

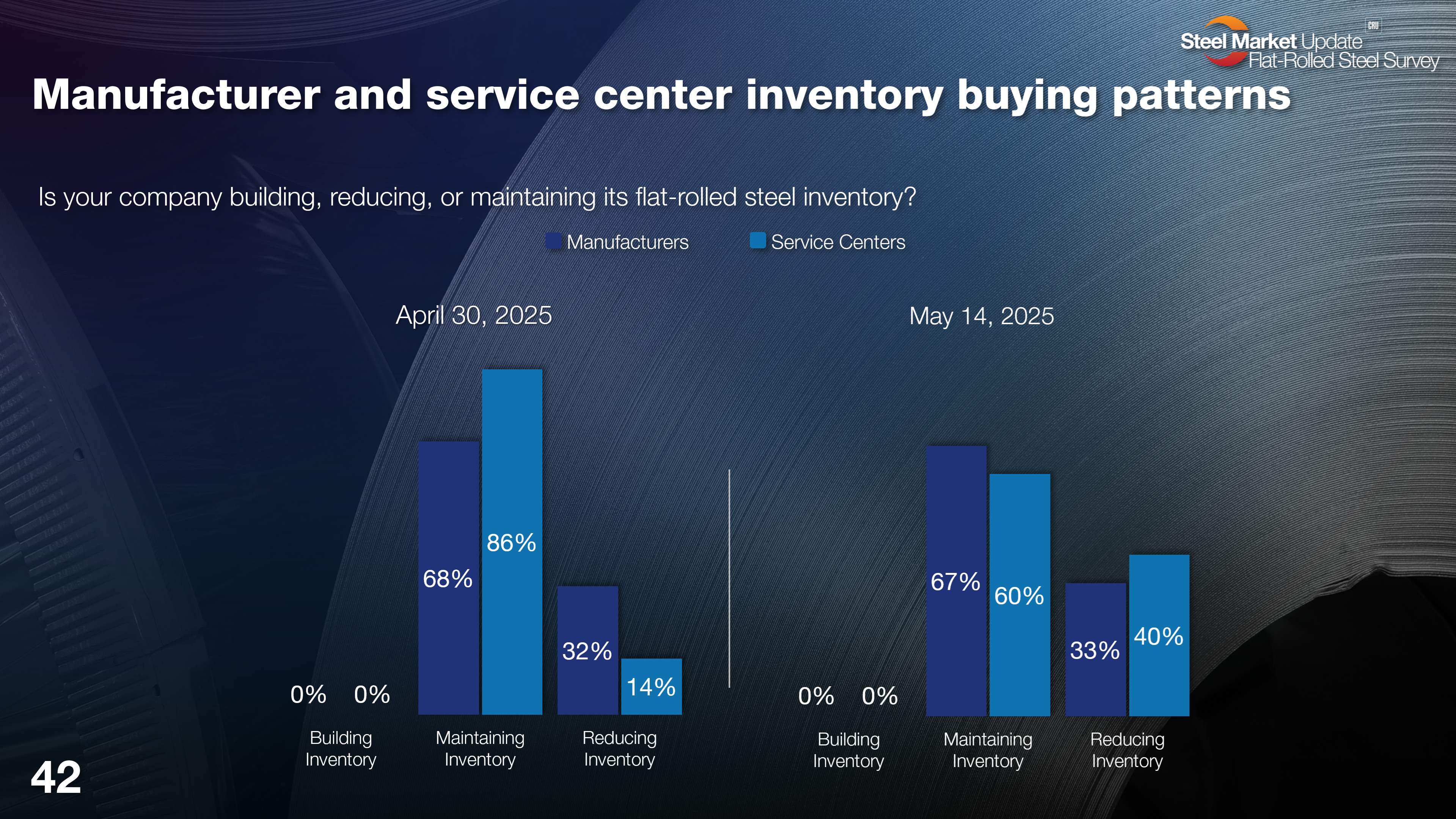

Pivot! Pivot! PIVOT….! (if you know, you know)

In mid-April, some buyers were still building inventories – even if marginally – to the tune of 4%-9% between service centers and OEMs. By the end of the month, it had shifted, and that shift remains in effect. Few, if any, steel buyers are building inventory.

This shift is unusual. Neither service centers nor manufacturers have reported restocking.

But perhaps, what’s even more unusual is that for at least the past month, buyers have clearly pivoted and are working hand-to-mouth. The name of the game is to reduce inventory costs and improve cash flow.

Here is what some survey respondents had to say:

“Maintaining number of tons, but our days inventory is dropping due to increased sales from our new mill. Volume is slightly down year-over-year on our legacy mills.”

“It seems we’re far below our inventory levels of the previous several months.”

“Definitely no reason to go long on inventory right now.”

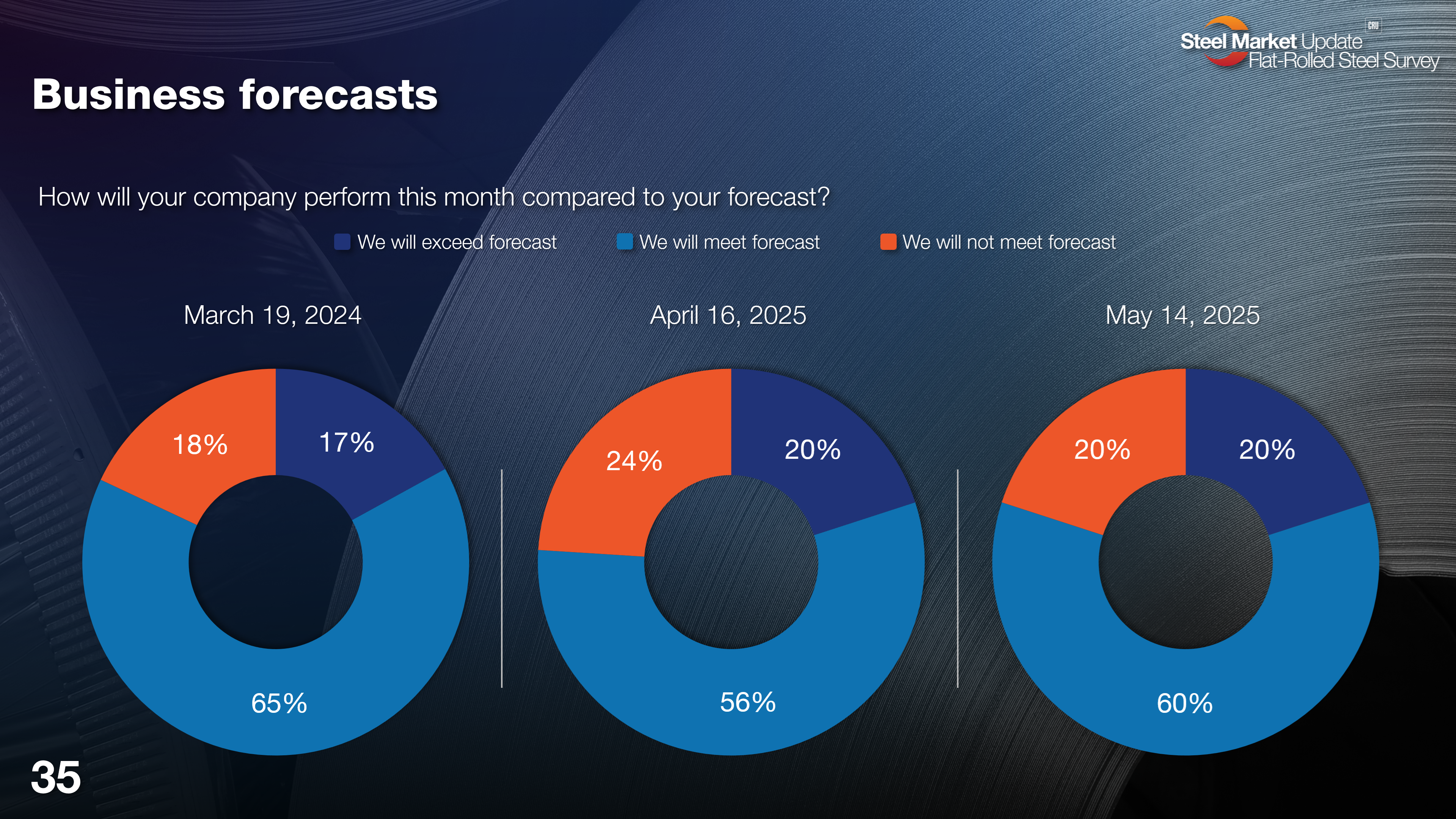

But it’s not all bad

Despite all the noted headwinds, more than three-quarters of survey respondents are meeting or exceeding forecast. What’s more, we’ve written a whole lot through Q4’24 and into early Q1, how more people were reporting missing forecast.

But they’re not as problematic as they recently had been. And that hasn’t been the case since prices and demand started picking up in mid-to-late February.

And here’s why:

“Too much uncertainty on market strength.”

“Prices are not going up. Scrap is not going down enough.”

“We’ve slowed, but still seem to be doing well enough.”

There you have it. There’s a lot more in there to unpack. We hope you find value in it too.

Our premium-level subscribers can find the full flat rolled survey results here.

And, as always, we appreciate all your support.