Mexico

June 12, 2025

Flack: HR futures still on a wild ride

Written by Gaby Ain

Another eventful week in the steel market comes to a close, marking a fortnight since the 50% tariff announcement. During this time, we’ve seen bullish euphoria, headline shocks, and bearish recalibration. Now, we see a return to cautiousness as uncertainty unfolds over policy clarity, mill pricing strategies, and end-user demand.

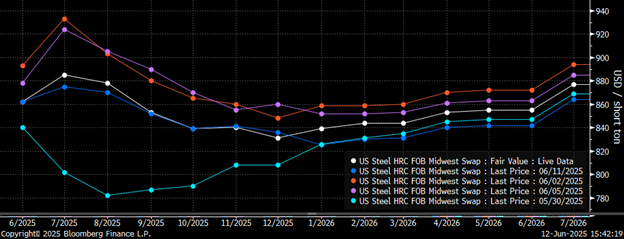

CME Midwest HRC Futures Curve

(June 12 in white, June 11 in blue, June 5 in purple, June 2 in orange, May 29 in teal)

Before we get into the development this week: reports of Mexico nearing a quota-based exemption deal, which has sparked discussion for the potential of broader tariff renegotiations with Canada and Brazil, let’s briefly retrace our steps.

Immediately following the surprise tariff announcement, the hot-rolled (HR) coil futures curve exploded, as illustrated in the jump from the pre-announcement curve (May 29, teal) to the post-announcement surge (June 2, orange). In the following days (June 5, purple), the curve held most of its gains, albeit with some notable volatility and intraday swings (as discussed in my previous column on June 3).

But as quickly as bullish optimism emerged, skepticism followed. The main headline of the week of Mexico nearing an exemption caused the curve to sharply retrace roughly $50-70 (June 11, blue). Today’s updated curve (June 12, white) underscores this ongoing recalibration.

Notably, the back end of the futures curve, 2026, snapped back down to pre-announcement levels following the Mexico news to lifting back up a bit today, a subtle but meaningful indication that long-term optimism is cautious at best. Futures remain elevated relative to pre-announcement levels. But sentiment has cooled on growing skepticism that the tariff increase will have the lasting teeth marks initially priced in. It’s also cooled as the reality of exemptions and more nuanced outcomes sets in.

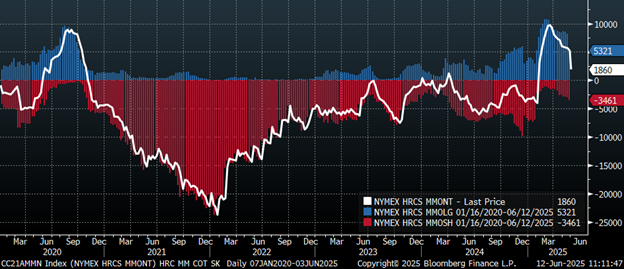

Positioning data tells a complementary story. Speculative net length sharply unwound as traders liquidated bullish bets. Concurrently, gross shorts ticked up, suggesting a growing bearish tilt – or at least defensive caution. Market positioning now appears relatively neutral, leaving room for volatility to spike again as more headlines come out and real-world impacts become clearer.

CME HRC money-manager positioning

Recent precedent has increased awareness that policy announcements are not necessarily policy implementations. And we’ve seen that volatility doesn’t always mean follow-through. So, is Taco Thursday a thing?

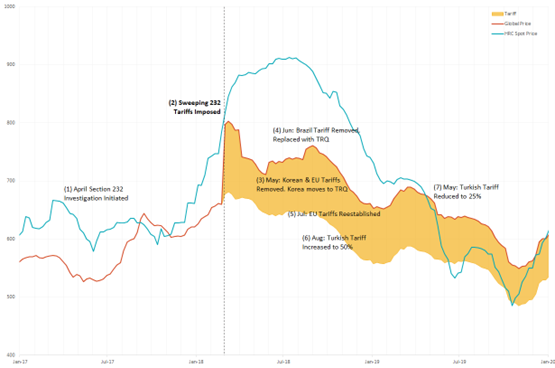

These recent developments also underscore the initial implementation of Section 232 tariffs in 2018. In the months following the original policy rollout, five significant adjustments occurred as denoted in the chart below. Considering this and recent developments, it could be safe to say that more is to come, contributing to ongoing uncertainty.

Section 232 2018 timeline

While the tariff news injected considerable volatility in the futures market, the implications on fundamental market conditions are a bit of a question mark. It’s not lost on me that we are in the early stages of the dog days of summer, where end-user demand hardly shoots through the roof.

Yes, policy shifts have provided a higher price floor due to increased import prices. And, yes, lead times have stopped shortening. But maybe those trends represent not significant upward momentum but instead that the bleeding has stopped. In technical terms, the market now appears to be coiling, with lower highs and higher lows. That’s indicative of a market consolidating rather than one making a decisive directional move.

However, another notable point to consider in all of this is mill leverage. The recency bias of mills’ swift and aggressive response to the across-the-board 25% tariffs in Q1 caused prices to increase rapidly and peak. So mills might show some restraint this time around. We saw evidence of that in Nucor’s CSP being upped by only $20/ton this week. We will have to see what Monday brings, when the steelmaker next updates CSP.

One thing remains clear: volatility isn’t gone. As the market weighs policy developments, seasonal demand headwinds, and supply implications, uncertainty is again the order of the day. The futures market may have completed one round trip. But it’s unlikely to be its last.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.