Mexico

June 26, 2025

HR Futures: Oil, Mideast tensions fail to move steel

Written by Mark Novakovich

After a raucous start to the month, the temperature has cooled in the past several weeks in the CME ferrous derivatives complex.

Futures prices have drifted lower since President Trump’s 50% Section 232 tariff announcement near the start of the month. Open interest and trade activity have also fallen, along with futures.

While tariff uncertainty still looms over the market, reports that Mexico may get a quota-based exemption has served to take some steam out of the most recently rally.

The Aug’25 CME HRC futures are still trading $80 per short ton (st) above their contract lows seen at the end of May, but the contract has given up $50/st since peaking earlier this month after the initial headline. It settled most recently at $868/st.

The Dec’25 HRC futures contract has also lost $50/st since its June 2 high, closing at $840/st today.

Neither mill prices hikes, nor oil price volatility, nor recent geopolitical events have done much to support flat prices or drive activity. In fact, the market has slowly ground lower.

Service center participants are said to be reluctant to lock in tonnages at the higher posted prices, some claiming that end-user demand remains soft.

The shape of the curve has also flattened since last writing. This corroborated the physical market weakness as the backwardation structure comes under pressure with nearby softness. After peaking at the end of May at $85/st, the Jul’25-Dec’25 spread now sits at $40/st.

Despite the brief spike in activity following the early June announcement on Section 232, open interest the HRC futures contract has fallen dramatically since the expiration of the May’25 futures contract. At that time ~140,000 st fell off the board.

After reaching nearly 800,000 st of total interest at the end of May, current open interest now stands at roughly 660,000 st, as fresh positioning failed to return to the market during the month.

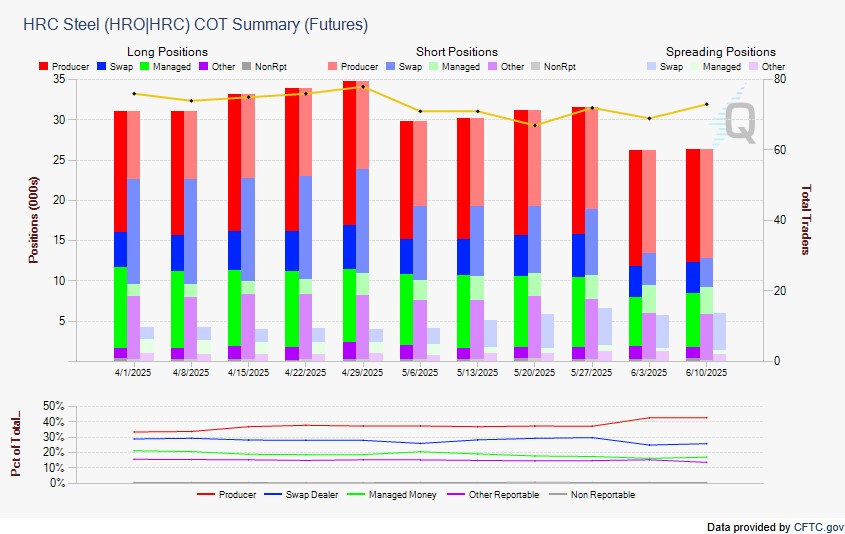

As the Commitment of Traders (COT) report shows below, all reporting groups have seen their activity decline since April.

There’s little to report on the CME’s No. 1 Busheling scrap futures, as paper trade activity remains practically nonexistent. Since the last writing on June 5, the second month Aug’25 BCH futures contract is unchanged at $460/st.

Open interest in the BCH has fallen slightly, currently standing at 44,000 gross tons (gt) total, down from 50,000 gt at the end of May.

Overall, the futures markets remain headline driven, and any new tariff announcement or trade deal could potentially drive the direction one way or the other. Absent any trade/tariff related announcements, however, it appears that the looming dog of days of summer have an early grip on the market.