Prices

July 17, 2025

HR Futures: Summer doldrums prevail

Written by David Feldstein

David Feldstein is the president of Rock Trading Advisors. Rock Trading Advisors is a National Futures Association Member Commodity Trade Advisory. It provides commercial clients with price risk solutions in ferrous, energy, and interest rate derivatives markets.

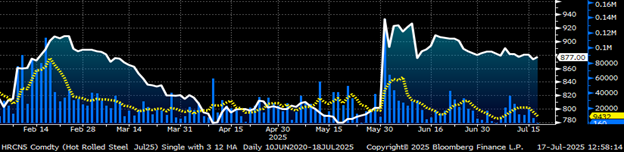

Not much to report on from the sleepy hot-rolled coil (HRC) futures market in the thick of the summer doldrums, with trading volume nearly grinding to a halt.

July CME HRC future $/st w aggregate curve volume & 5-day avg.

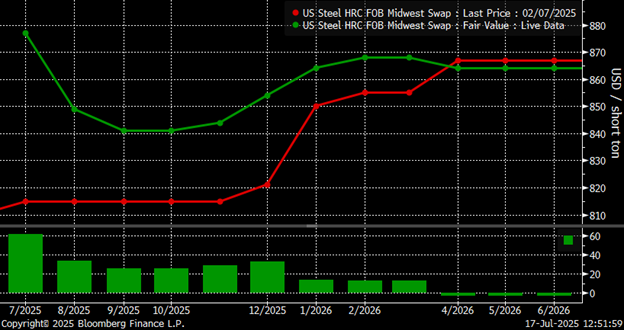

Trump announced a 25% tariff on steel on Feb. 9 and then increased it to 50% on May 30. This chart shows how today’s curve compares to the curve on Friday, Feb. 7. Surprisingly, the curve has seen little change considering the circumstances.

CME hot-rolled coil futures curve $/st

Each Friday, the CFTC publishes a breakdown of open interest as of the previous Tuesday’s close, detailing the long and short positions held in aggregate by each participant group.

Open interest is the number of outstanding futures contracts, or tons in this case, across a product’s curve. The Commodities Futures Trading Commission (CFTC) categorizes futures market participants into four categories: commercials, managed money, swap dealers, and others. The commercials category includes producers, merchants, processors and users.

This chart shows the long futures position for the commercial participants surge in response to the 25% tariff announcement.

On Tuesday, Feb. 4, commercial players held 217.5k tons. On March 18, the long position peaked at 363k tons. The bulk of the long position was held in the April, May, and June futures. The long position took a step lower after the expiration of the April future, then it drifted lower following May’s expiration.

Then it tanked to 175k tons when the June future expired, indicating that commercial participants have moved away from taking on medium or long-term fixed priced deals, and opting to go naked instead.

Does this provide a glimpse into the steel buying community’s physical purchasing strategy? That is, a strategy of shifting towards a focus on short-term buys, while ignoring the potential upside risks.

CFTC Commitment of Traders –commercials long position

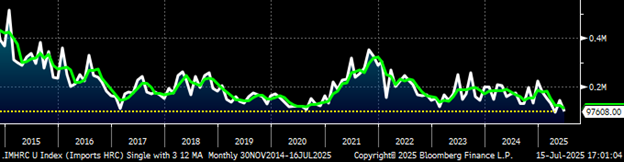

Flat rolled imports are down significantly in 2025. In fact, June’s HRC sheet imports of 97.6k tons fell to their second lowest month since 2009, and that was second behind April’s. Imports of HR, CR, HDG, and galvalume sheets combined were down a whopping 911k tons, or 42%, in Q2’25 vs. Q2’24.

Imports – HRC sheet

Domestic steel production has seen a revival, climbing from around 74% capacity utilization in Q1 to around 79% over the past few weeks. Domestic mills have gained market share at the expense of their international competitors, putting them in a solid position with HRC lead times weeks away from being in September.

AISI raw crude steel production

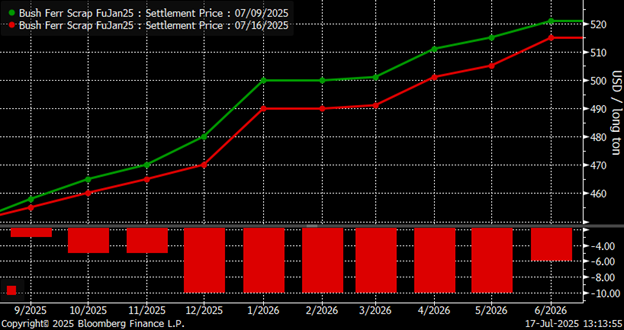

Last Friday, President Trump announced 50% tariffs on imports from Brazil. In Tuesday’s Steel Market Update, Stephen Miller reported Brazil has shipped 1.62 million metric tons of pig iron into the US so far in 2025, which equates to ~67% of year-to-date (YTD) pig iron imports through May. Shockingly, the Chicago futures market has declined since the announcement. Perhaps this is the summer doldrums, or perhaps it is a reflection of a market that refuses to believe the tariffs will remain in place.

CME Chicago Busheling Futures Curve $/lt

Who can blame the doubters? There has been a tremendous amount of tumult out of the Trump administration on the trade front over the past few months. However, below I provide you with the following collection of headlines made by Brazil’s President Lula since Trump’s announcement and ask you to decide for yourself:

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Mr. Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.