Analysis

September 18, 2025

Final Thoughts

Written by David Schollaert

We’ve been talking about a potential inflection point for the past couple of weeks. And the market does appear to be nearing one. While prices are still slipping – average HR prices are below the $800-per-short-ton mark – larger discounts might be done, or nearly there.

And it’s not just prices. Lead times are showing some early signs of a turn, and mills are not as eager to talk price.

But there are still some varying views on what comes next.

Some expect prices to move higher this fall on fewer imports and lower inventories, coupled with mill maintenance outages. There’s hope that better demand will follow the typically slower summer months. For those who believe, it’s just a matter of time, and it could be soon.

But others expect the only real impact of fall outages will be a cut in prime scrap prices, thanks to reduced scrap demand from sheet mills. Not to mention, they expect new domestic capacity will largely replace imports.

But all agree that, ultimately, a demand shift is necessary. And all are hoping it happens soon.

While we wait on that to happen, here’s a sneak peek at just a couple of data points in our latest survey results, which will be made available to premium members tomorrow.

Survey says

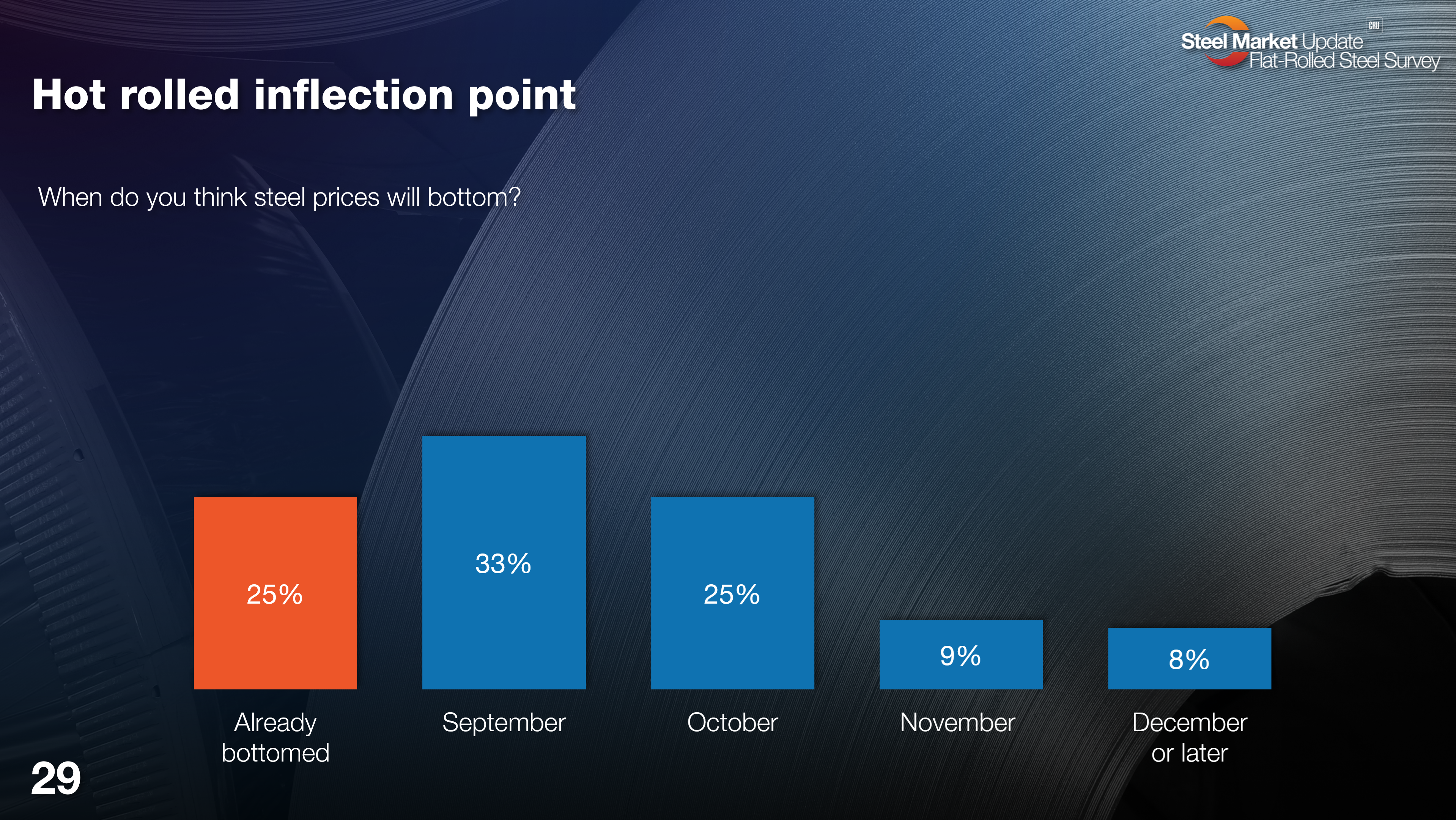

For starters, a quarter of survey respondents think HR steel prices have bottomed (see Figure 1). Prices have been largely trending down since late March – even with a short-lived bump in prices in June. Still, another third of respondents believe they will bottom this month. Yet, 42% think prices will move lower and won’t bottom until Q4.

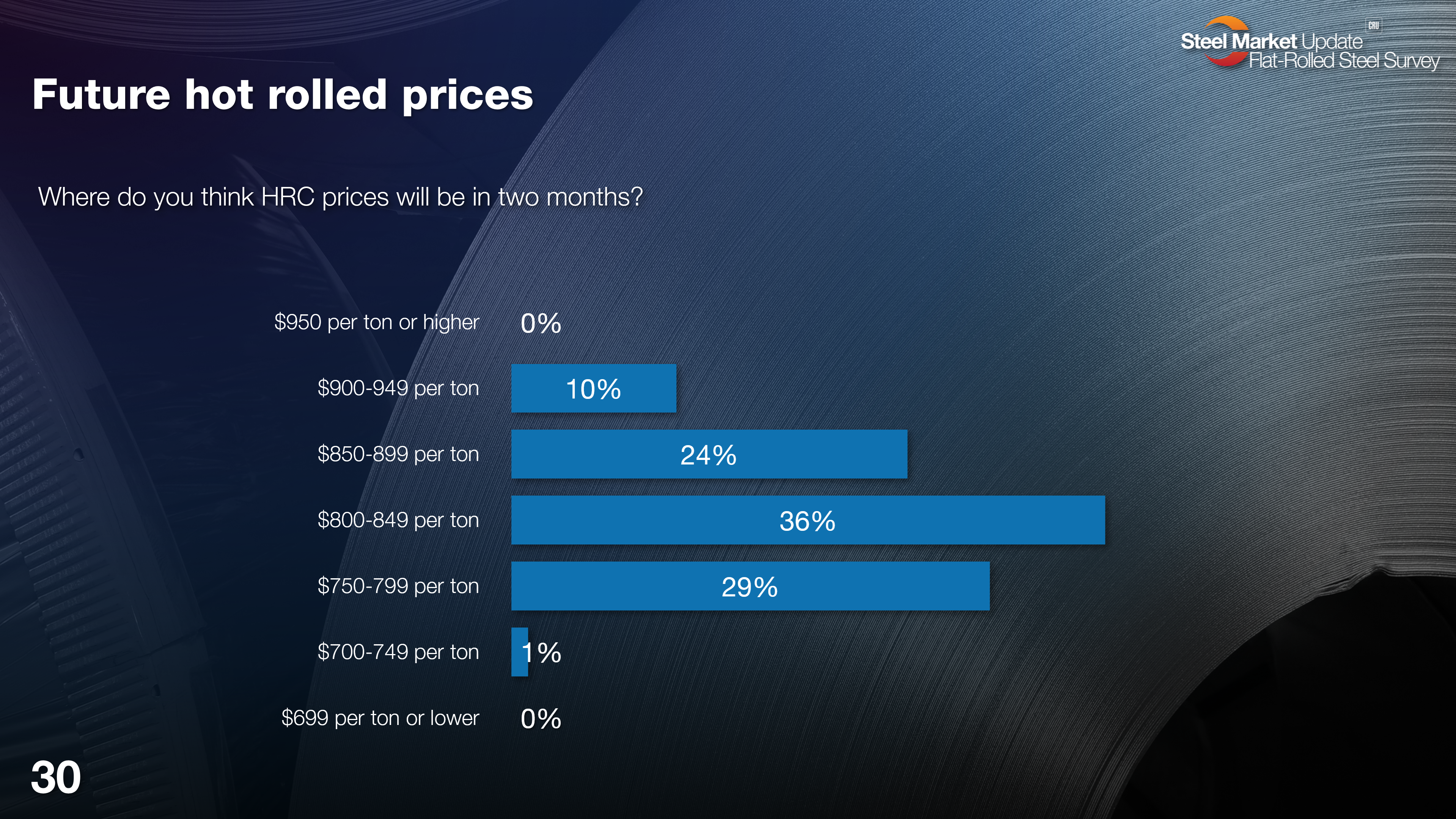

Surprisingly, though, 70% of those surveyed (see Figure 2) expect prices to rebound and trend higher two months from now.

(Editor’s note: You can click on any of the charts below to expand them. Note, too, that the numbers in the bottom left-hand side of the tables indicate which page you can find them on in the survey slide deck.)

You can see from the comments below that buyers feel like they’re just trying to keep their footing between bells, taking cover from tariff blows:

“Prices will increase due to lack of imports and mill outages.”

“I expect the bottom to come soon if we haven’t seen it already.”

“Planned outages combined with low inventories will cause prices to rise.”

“Seeing signals from the mills, pricing is going up.”

“I think we’re pretty close to the bottom of this cycle right now.”

“I think we might see a temporary floor coming up, but then the slide will continue early next year.”

Tariff turbulence real

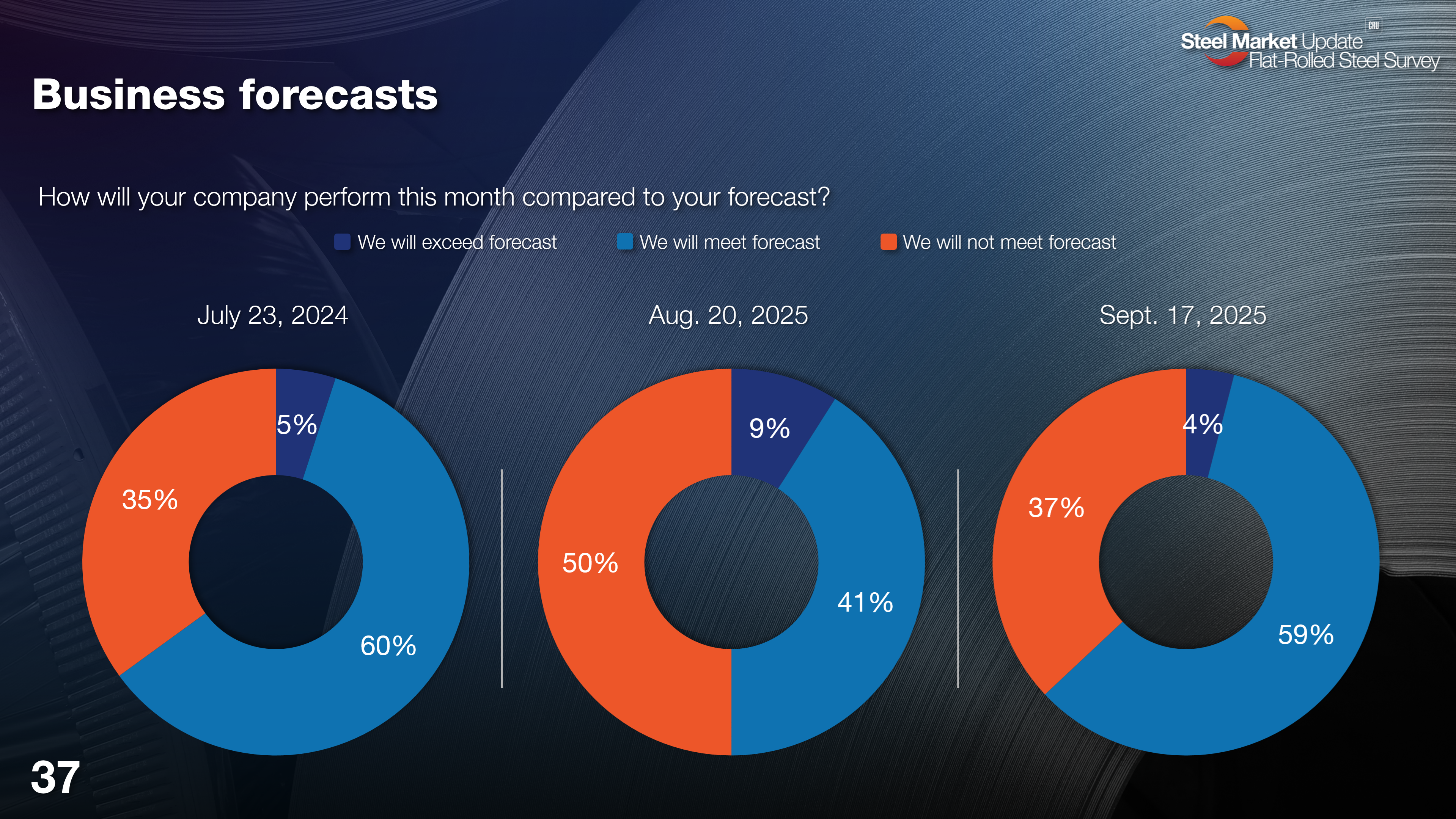

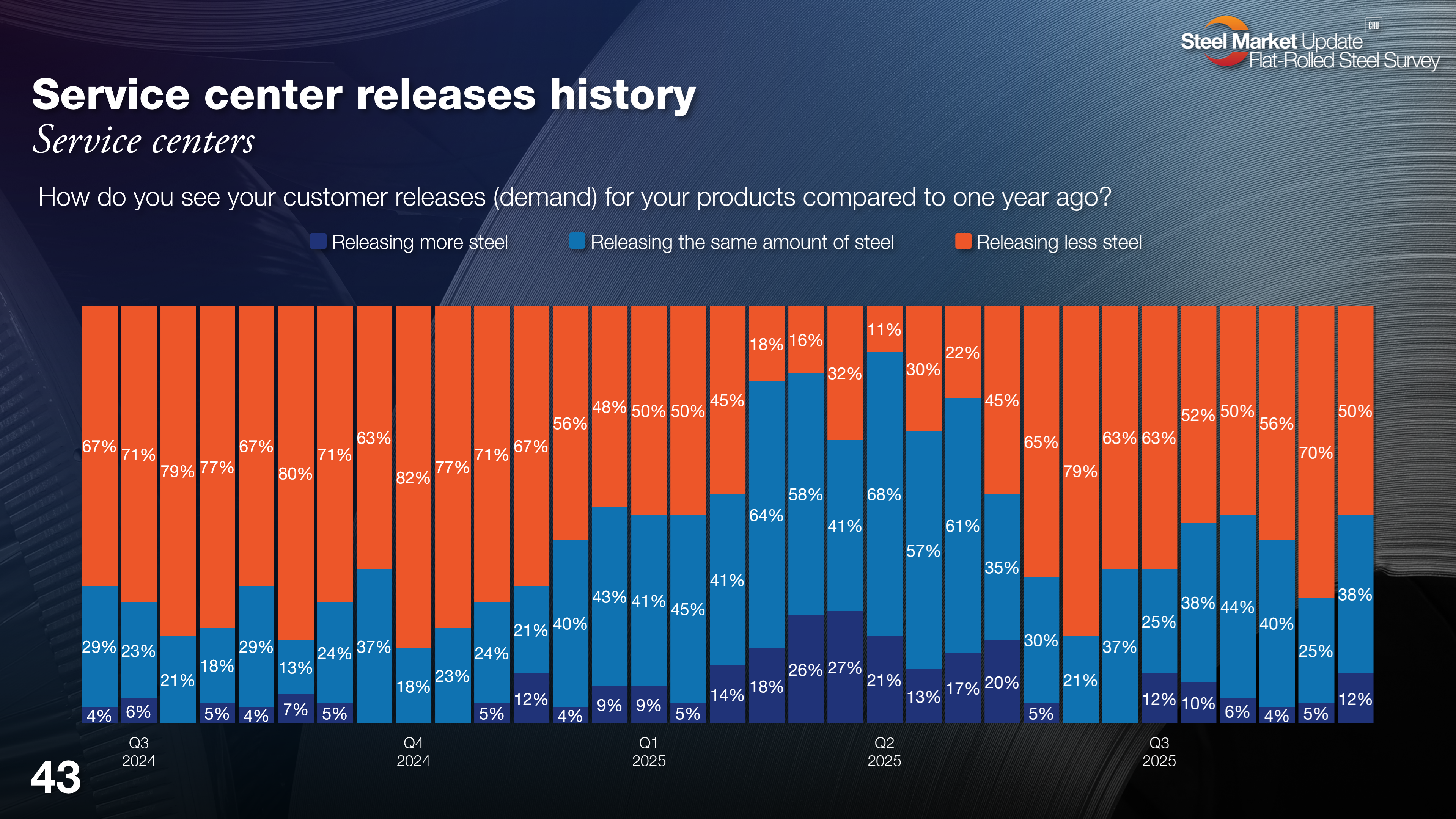

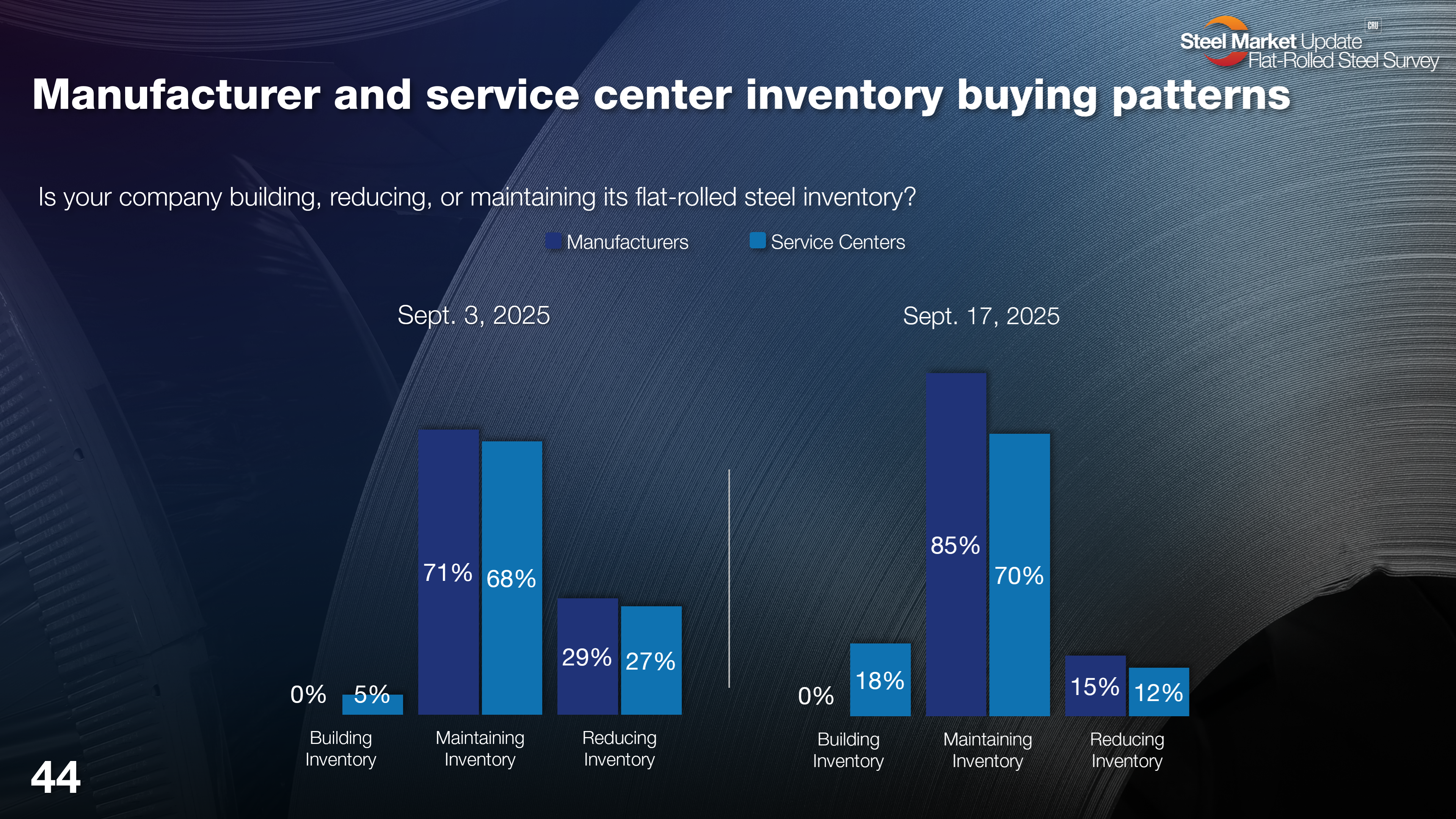

There’s been a clear shift since Section 232 tariffs were doubled to 50% in June, backed by a bit of seasonality. Whatever the case, we see that many steel buyers aren’t meeting forecasts. It’s a trend we’ve been seeing since late May, and it’s not letting up. Also, half of service center respondents say they are releasing less steel than they were a year ago. It’s been a rough go since mid Q2. Meanwhile, there’s been a slight shift, with some now building inventory – perhaps indicative of an inflection point? Those trends are detailed in the following three charts.

But it’s not all bad

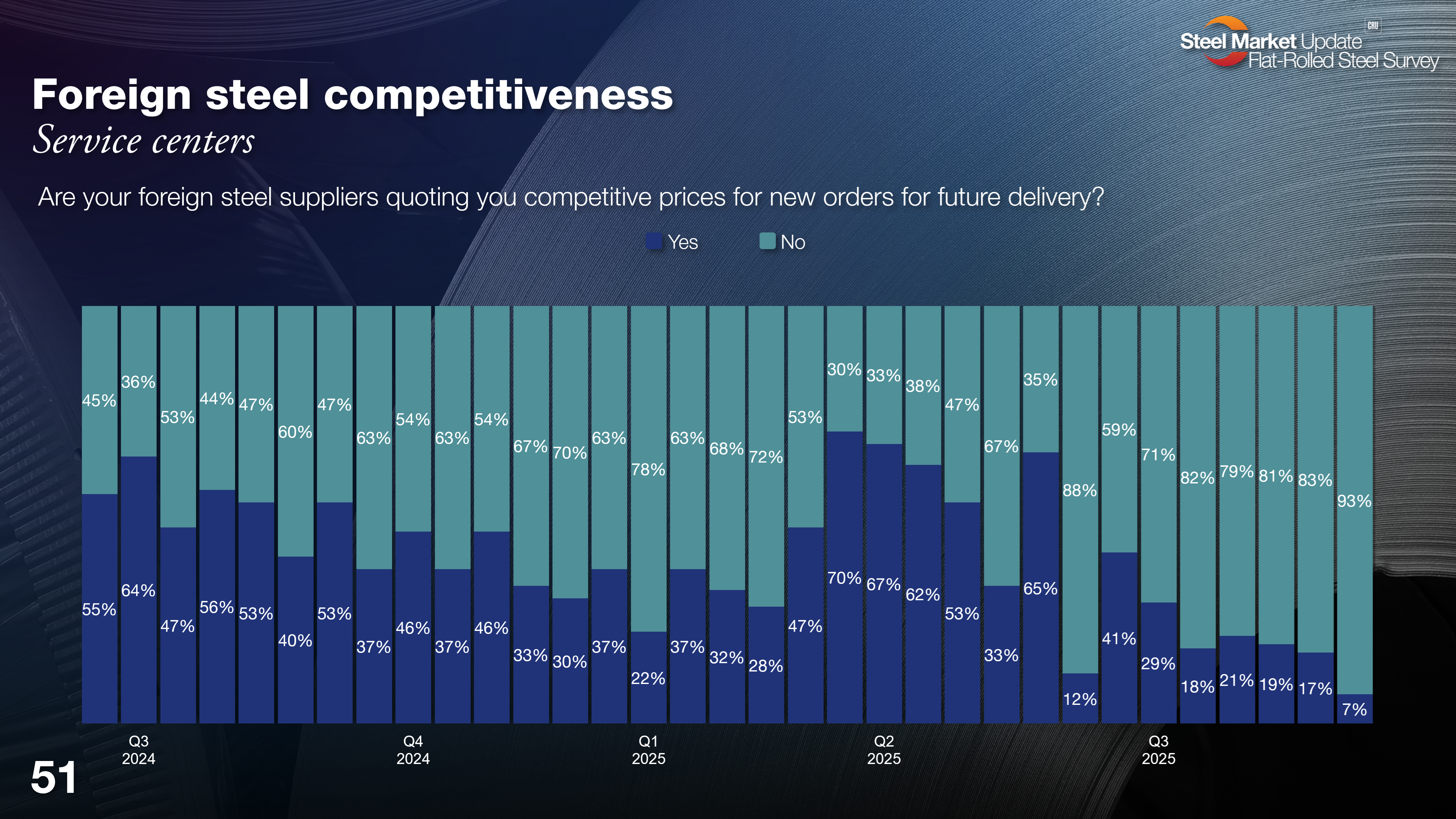

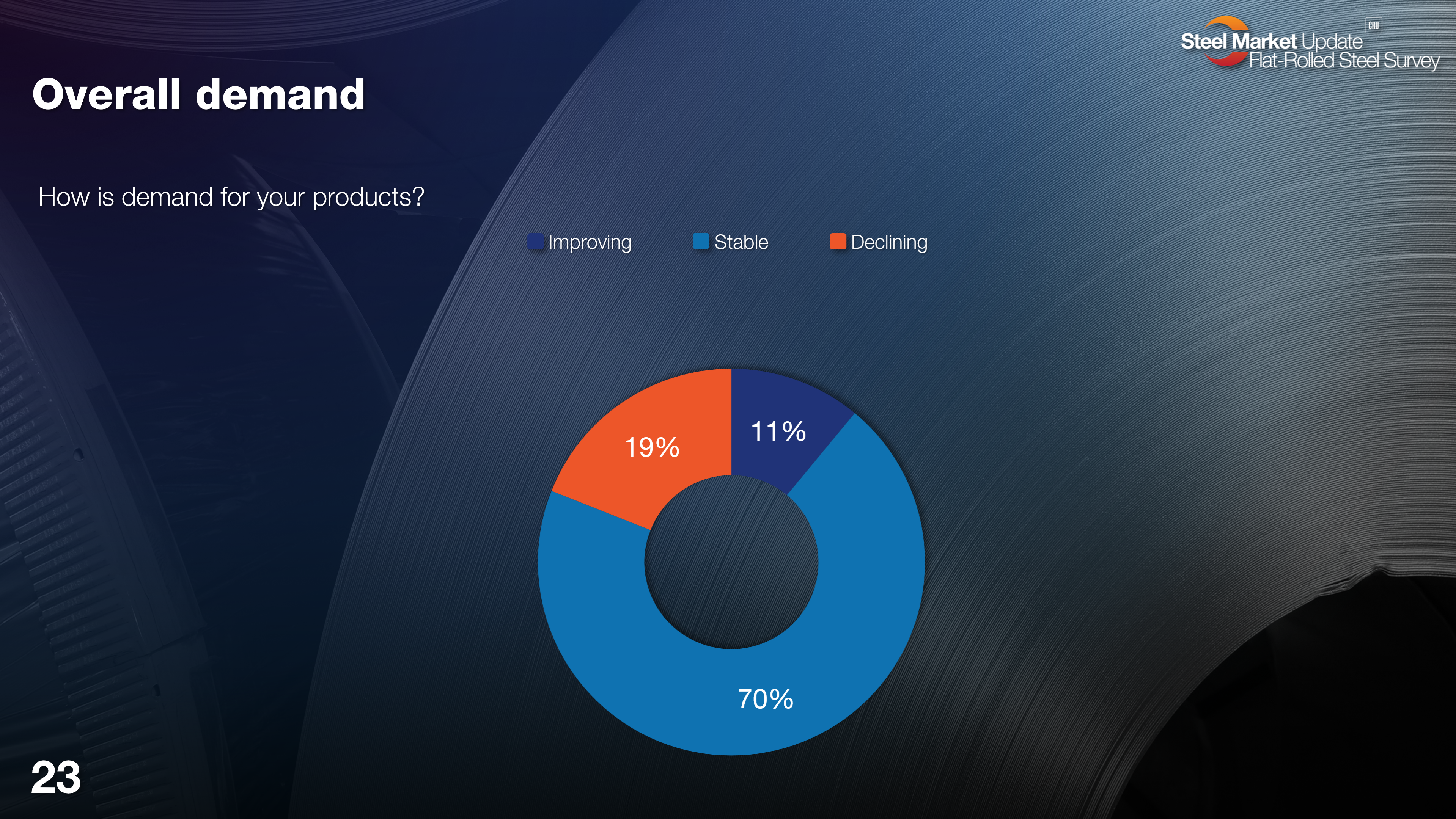

There is no import competition. Over 90% of survey respondents say imports aren’t competitive with the 50% Section 232 tariff and declining domestic prices. When the tariff was 25%, most still said imports were competitive. If there is some good news, it’s this: Despite all the tariff noise, most survey respondents say that demand is relatively stable. They’re still on their feet and fighting.

Well, there you have it — just a few data points from our latest survey. Be sure to check it out when it lands tomorrow. And if you don’t have a premium-level membership, reach out to Luis Corona at luis.corona@crugroup.com, and he’ll set you up.

As always, we appreciate all your support.