Analysis

June 2, 2026

SMU Survey: N. American demand edges higher while import interest stays selective

Written by Laura Miller

US steel buyers report firmer domestic demand, but long lead times, rising freight costs, and geopolitical uncertainty continue to cause caution on imports.

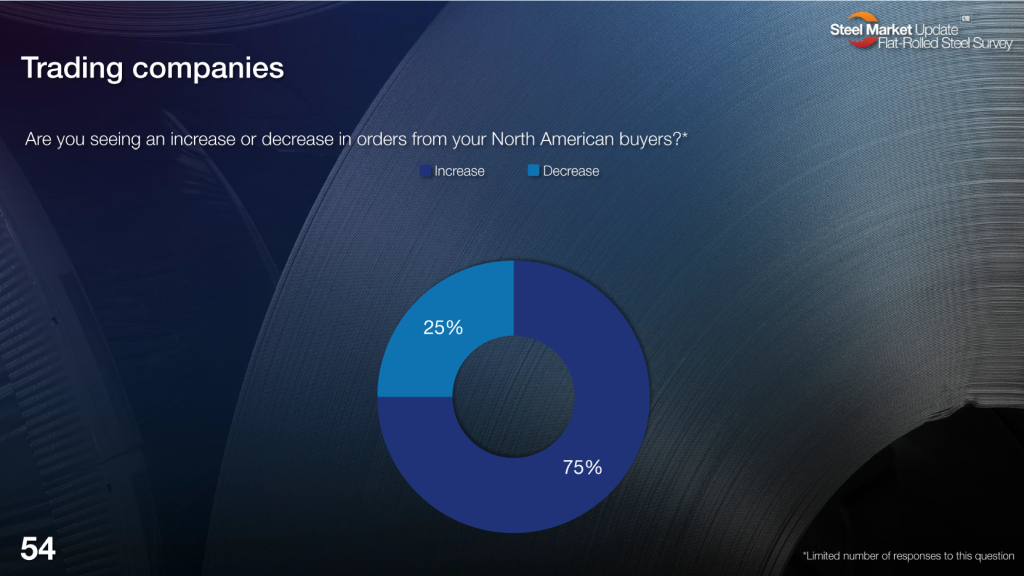

North American orders are ticking up, according to multiple traders responding to SMU’s May 29 steel buyers’ survey. Three-quarters of traders reported demand as increasing (slide 54 below). One trader noted “sentiment is positive,” even as supply tightness persists. Another said demand is higher, but it’s “hard to source competitively.”

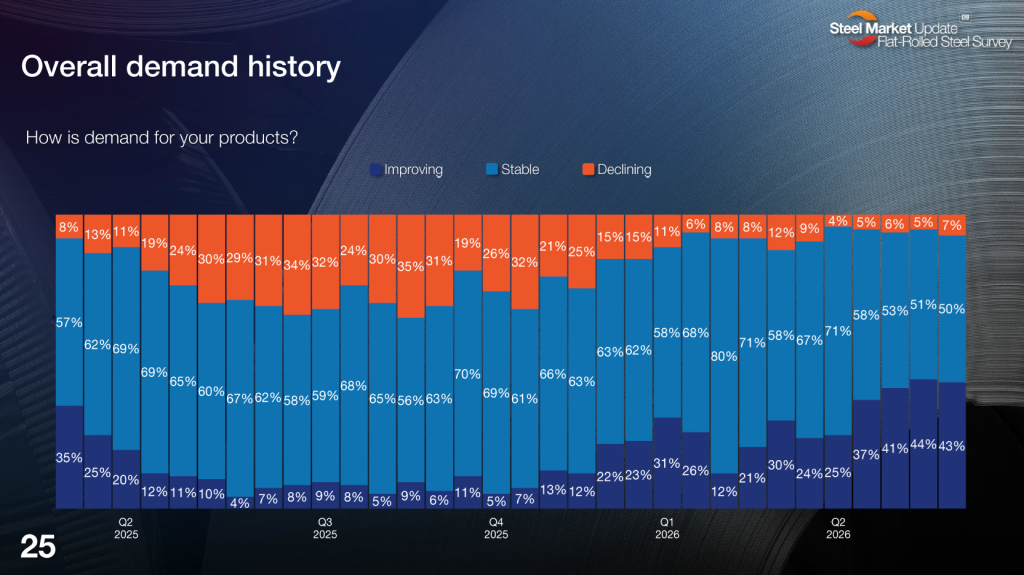

Of all surveyed steel buyers, around 40% have reported improving demand in our last four surveys. Half of buyers said demand is stable in our latest survey, while just 7% reported contracting demand (slide 25).

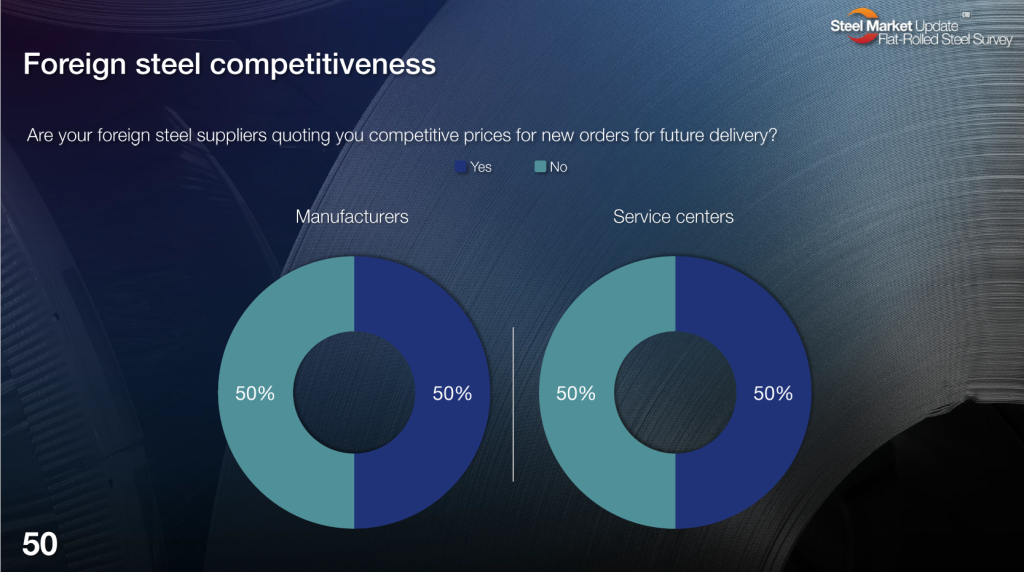

Competitive import pricing remains available, but not compelling enough to shift buying patterns. While 100% of surveyed traders reported that foreign products are attractive to US buyers, only 50% of service centers and manufacturers reported competitive import offers (slide 50). Increased transportation costs have eroded expected discounts, according to one trader. One service center respondent added they “wish we would have taken advantage of prices… in February and March,” but are now avoiding foreign tons with October arrivals.

Hot-rolled import offers were reported at $925 DDP US port compared to average domestic prices of $1,095 per short ton (SMU’s price as of Tuesday, May 26. We will update our prices on the evening of Tuesday, June 2). However, traders highlighted long lead times – typically 4-5 months for imports – that are limiting buyers’ appetite. Lead times for domestic HR are currently 7.1 weeks on average. Imports are “attractive on price but not on lead times,” commented one trader, while others described interest as “very selective.” One trader said Korean hot rolled is competitive but still faces timing risks.

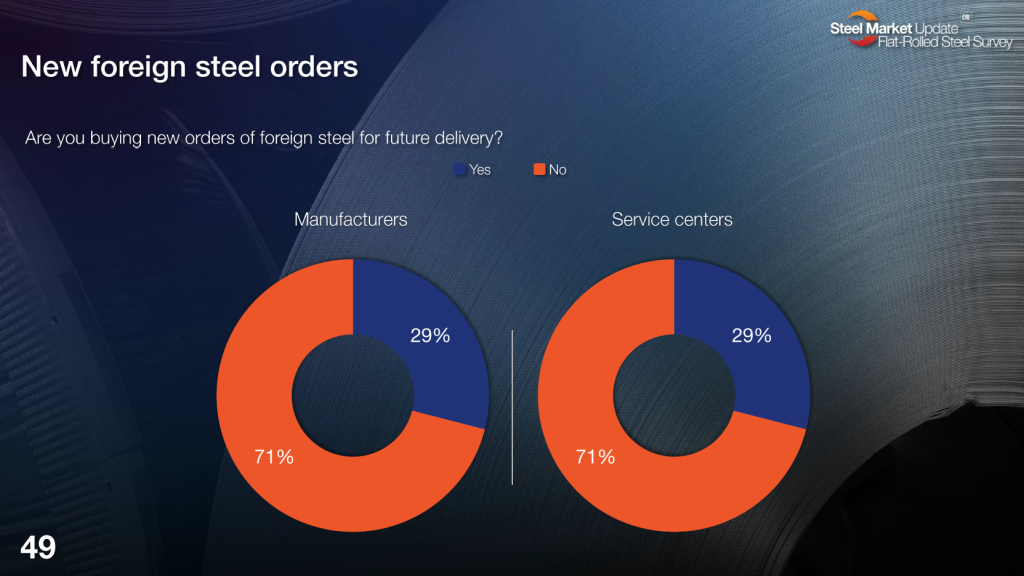

Some buyers are stepping back entirely. A manufacturer said they are not placing new foreign orders, noting that landed import prices are currently “the same as domestic,” even as Asian pricing trends lower. Only 29% of manufacturers and service centers said they are buying new orders of foreign steel for future delivery (slide 49).

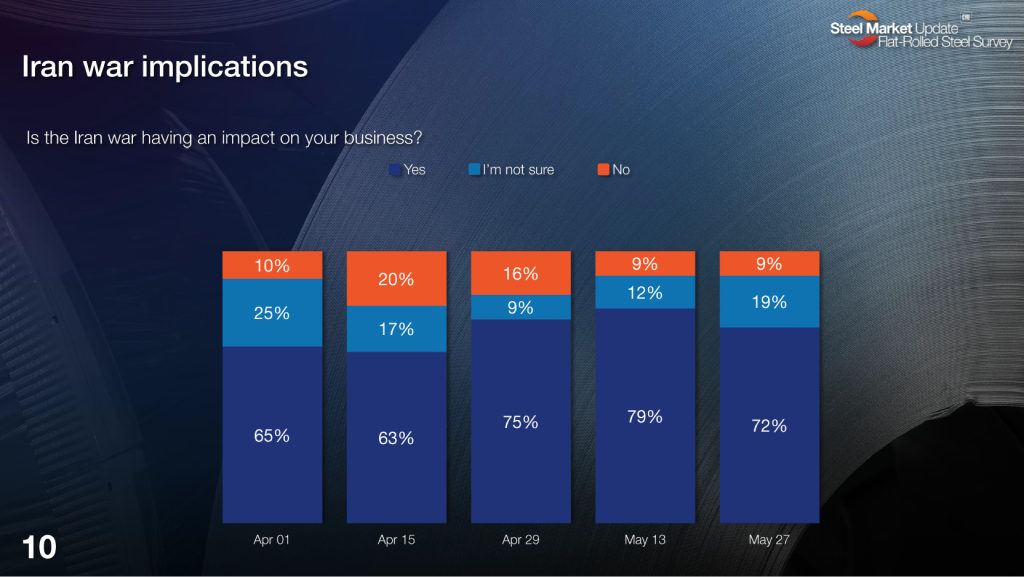

Respondents across the supply chain overwhelmingly continued to flag rising costs tied to the Iran conflict. While 72% of respondents said the Iran war is affecting business (slide 10), nearly every segment – mills, service centers, traders, manufacturers, and suppliers – cited rising costs for fuel, freight, energy, insurance, and logistics. Respondents described higher diesel prices, fuel surcharges, and supply chain interruptions. One manufacturer called the impact “brutal” on gas/oil pricing alone.

Looking ahead, uncertainty reigns. SMU’s Steel Buyers’ Sentiment Indices slipped last week, but remain relatively strong. One respondent, a scrap supplier, summed up the near-term outlook bluntly: business levels will be “worse, if the conflict in the Middle East continues.”