Analysis

June 18, 2026

HR Futures: Market sees longer rally, higher peak

Written by Gaby Ain

In my previous column, on May 21, I continued to question the effectiveness of the usual supply response mechanisms in this current environment. Since then, the US HRC futures curve has continued to move higher, particularly in the deferred months, suggesting the market is pricing a slower return to balance.

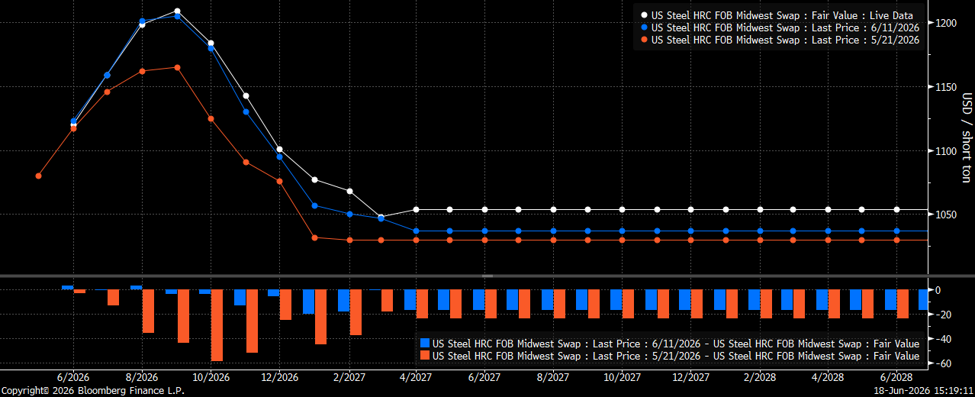

CME Midwest HRC futures curve (6/18 in white, 6/11 in blue, 5/12 in orange)

A month ago, the HRC futures curve (orange) was already reflecting a longer-lasting tightness scenario. The peak had shifted further into late summer, deferred months had lifted, and the market was questioning supply response. That question has not gone away. If anything, it has become more pointed.

The curve today (white) is higher across most of the strip compared to May 21. The nearby months are only modestly higher. June and July are up roughly $5-15/st. But August and September are up closer to $40-45/st, with the peak breaking through another threshold, $1,200-1,210/st. October and November have increased by approximately $50-60/st. Meanwhile, the 2027 contracts have gained roughly $15-45/st.

That is the key shift. The market is not simply pricing a higher peak. It is assigning more value to the possibility that tightness lasts into Q4 and early 2027. Those would potentially be the months when the usual supply response mechanisms (domestic production, imports, rebuilt inventories) would typically begin acting as a release valve for higher prices.

Instead, the curve has lifted. Week over week (blue), the signal is more restrained. The front of the curve is little changed. But the deferred months have continued to inch higher, suggesting the market is still adding a risk premium further out. The curve remains backwardated after September. So it is not necessarily pricing indefinite tightness, but it is pricing a higher normalization later. Physical market indicators continue to support the market. A notable one being inventories remaining lean, in part because of delayed mill shipments. The means service centers remain limited by what they can receive and ship. In an availability-driven market, what I referred to as effective supply in my previous column, that distinction matters. Lower shipments do not necessarily mean weaker demand if the supply chain cannot access enough tons to move. It can also extend the time it takes for inventories to rebuild.

Imports continue to be at suppressed levels, albeit have been increasing, which is a counterpoint. However, imports arriving in the right products, in enough volume, and consistently enough to become a pressure-release valve (their effectiveness to respond) is just something we have yet to see. Domestic raw steel production remains relatively elevated, even after cooling week over week, and the planned spring outage season should wrap up this month.

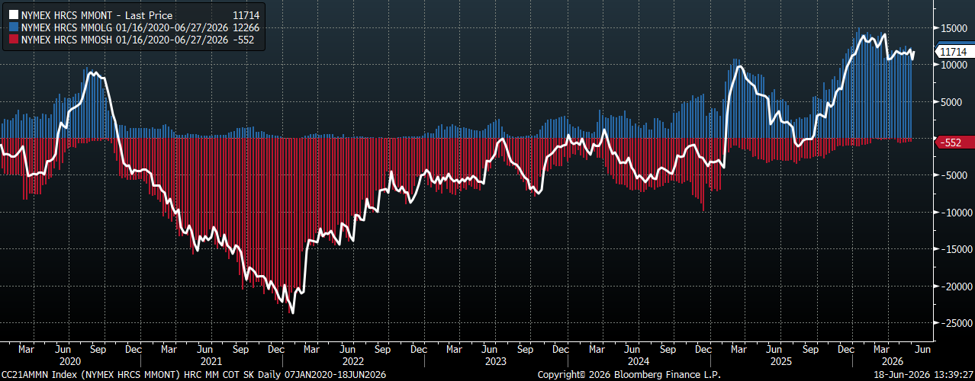

CME HRC money-manager positioning

CME HRC Positioning adds another layer. Money managers remain heavily net long, suggesting participants are positioned for continued tightness, higher prices, or at least a higher floor. But net length has largely moved sideways in recent months. This suggests recent strength is not being driven by a fresh short squeeze but instead by existing long conviction and physical tightness. The setup is constructive, but mature. With little short-covering fuel left, the curve increasingly needs the physical market to keep confirming the story.

In short, the market remains supported. But it is no longer early-cycle bullish. The focus has shifted more toward how long tightness can last. For now, availability remains the dominant theme. The risk is that if inventories, lead times, or imports begin to turn, the futures market may have less room for hesitation.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his or her opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice of a financial professional before taking action in financial markets.