Analysis

June 18, 2026

SMU Steel Demand Index moves higher

Written by David Schollaert

SMU’s Steel Demand Index ticked back up from late May, remaining in elevated territory, according to mid-June indicators.

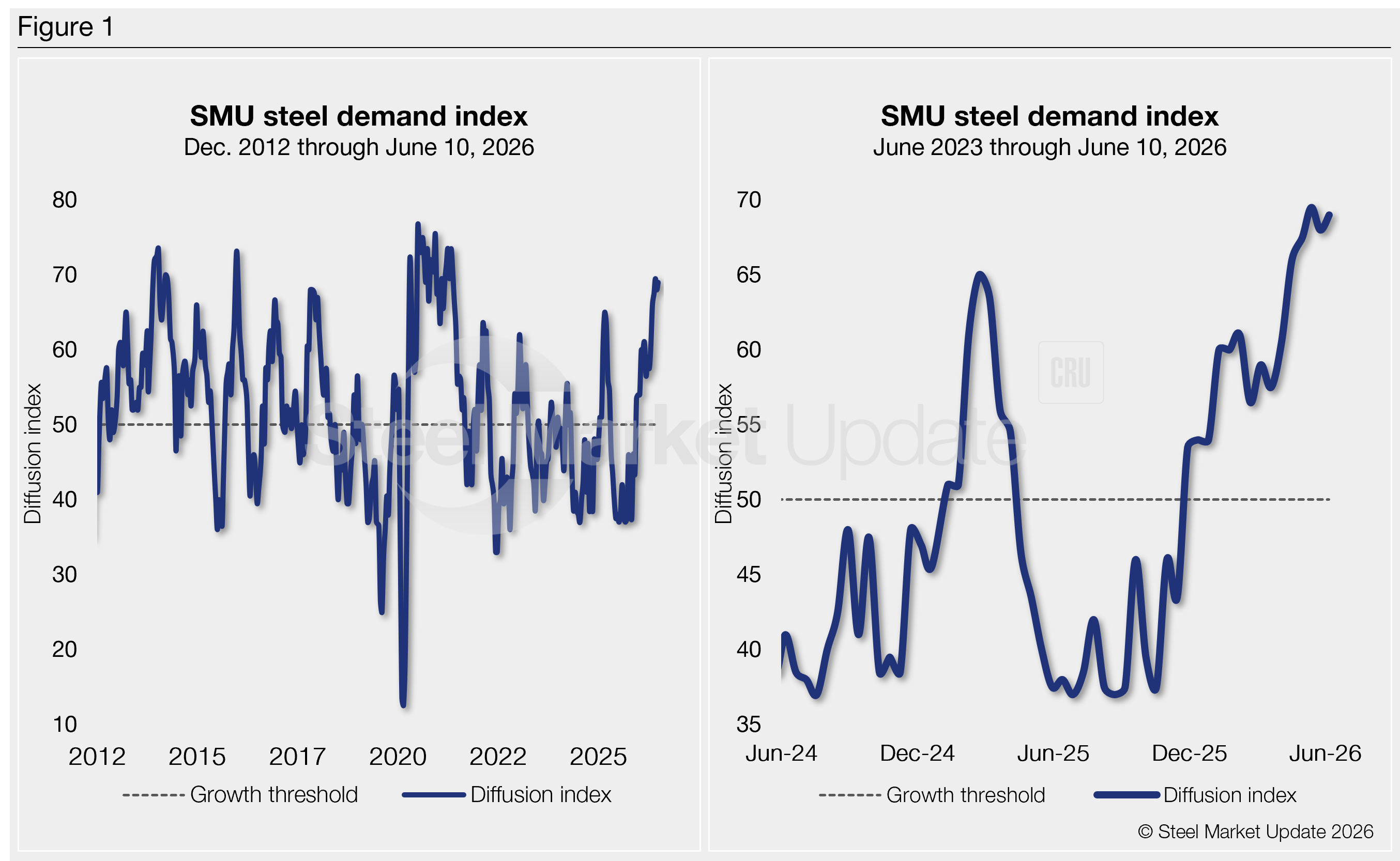

The Steel Demand Index, compiled from our survey data, now stands at 69.0, up from a reading of 68.0 in late May and near a five-year high of 70.5 from June 2021.

The index has been in expansion and gaining momentum since late November. The trend continues to underscore steady-to-rising demand as supply remains tight.

The positive movement began to take shape with an early buying frenzy ignited by the onset of undiluted Section 232 steel tariffs last March. And after a slight decline post-rush, the erosion of imports resulted in steady, widespread positive momentum in demand.

Methodology

Derived from the market surveys SMU conducts every other week, the Steel Demand Index is a diffusion index and a statistical tool to measure the breadth of change across our overall demand data series. It effectively helps identify widespread demand trends or turning points.

This index has historically preceded lead times. This is notable given that lead times are often seen as a leading indicator of steel price moves. An index score above 50 indicates rising demand, and a score below 50 suggests declining demand.

Figure 1 shows the nearly 13-year history of the index on the left and provides a closer look at the Steel Demand Index readings of the past two years on the right.

Rearview mirror analysis

Last year, demand had a bit of a seesaw buying pattern. Though improved from 2024, it was heavily impacted by a shift in the tariff regime, which resulted in a slightly higher pricing floor despite uneven demand.

But that dynamic shifted, as has sentiment, demand, and prices as well. The current sheet price rally has been ongoing for nearly nine months. We haven’t seen that since the post-pandemic snapback.

Mills have been very disciplined, and tariffs continue to be a barrier for imports—a likely driver of the present rally.

What’s currently in play

The upward grind appears as if it will continue, especially with few, if any, talking about the summer doldrums.

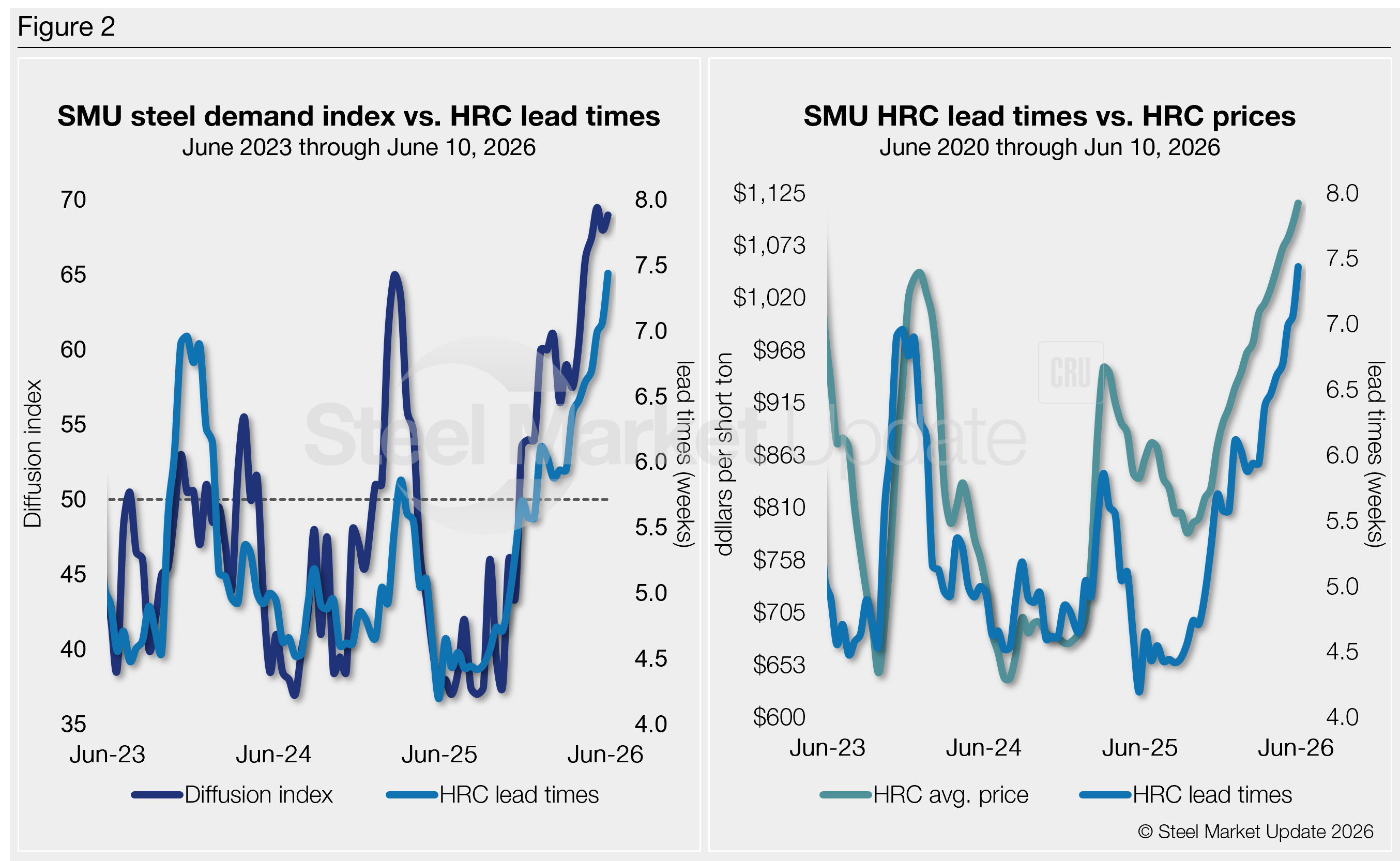

Lead times for hot-rolled coil are now more than seven weeks on average, and easily into September. Depending on the mill, that could even spill over into Q4. The dynamic is starting to cause some in the market to believe it could carry through the balance of the year.

HR coil prices have followed a similar trend, reaching an average of $1,115 per short ton (st) in early June. They are up, and pointing higher, according to SMU’s latest market check on Tuesday, June 16; domestic hot band ranged from $1,100/st to $1,160/st, with an average of $1,130/st.

Lead times have moved up as well. Production times have risen since last November and are now at multi-year highs. Current levels are significantly longer than those seen last summer.

Some mills are beginning to catch up on orders following their spring outages, but others are reportedly still struggling to keep up with demand and are quoting significantly longer production times.

The average production time for HR coil is 7.5 weeks, the highest it has been in four and a half years.

For nearly a decade, SMU’s steel demand diffusion index has preceded moves in mill lead times (Figure 2, left side), and SMU’s lead times have also been a leading indicator of flat-rolled steel prices, particularly for HRC (Figure 2, right side).

In their own words

Here are a few quotes from our latest survey about how flat-rolled steel buyers see demand:

“We’re starting to get some panic calls.”

“Shortages in many products, from flat rolled to tubing to structural.”

“Super busy.”

“Business is steady, but supply is the problem.”

“Demand is strong.”

“Improving/stable at high levels.”

“Larger sales projects are lagging due to instability in the economy.”

“The last four months have been strong. Last week, I started to see a little slowdown.”

“If the steel mills can get us the steel we ordered on time.”

“Depends on supply options.”

“We seem to be doing very well.”

“Still some uncertainties to contend with.”

“It’s too hard to get anything on the spot market. We are relying on contracts.”

Signals ahead

Demand is steady, but buying remains largely tied to contracts—in many cases, buyers are being held to minimum volumes and actively looking to add through spot.

And while inventories were initially closely monitored to start the year, the dynamic has shifted. Stretching lead times and intake delays have led to double-buying and an increased search for spot tons.

This has been the trend for much of the past six-plus months.

But lead times and prices are moving up. In fact, HR coil prices are in the middle of one of their most sustained rallies in nearly a year. And while few, if any, expect demand to rally at a significant rate, tariffs have cut import competition, providing a stronger base for domestic products and thus prices.

Add that to lean inventories and firm raw material costs, and you have the current pricing support in play. And pair that with many reporting trouble finding available tons, and pricing gains might remain on the horizon for the time being.

Pockets of demand vary from sector to sector, but overall buying has picked up. The trend is still significantly driven by a noticeable squeeze in supply, as tariffs have been a significant inhibitor to imports. But, with domestic prices rising and offshore markets trending in the opposite direction, the arrival of imports could impact the market.

But time will tell. We don’t forecast at SMU. We leave that to our colleagues at CRU, but ultimately, we’ll have a clear picture post-summer and hopefully just in time for the SMU Steel Summit in late August.

In the interim, we’ll continue to report on indicators, looking for smoother sailing ahead.

Editor’s note

Demand, lead times, and prices are based on the average data from manufacturers and steel service centers participating in SMU’s market trends analysis surveys. Our demand and lead times do not predict prices but are leading indicators of overall market dynamics and potential pricing dynamics. Look to your mill rep for actual lead times and prices.