Analysis

June 23, 2026

SMU Price Ranges: Sheet's hot streak continues

Written by Brett Linton & Michael Cowden

US sheet prices continue to move higher on extremely limited spot availability, solid demand, and extended lead times.

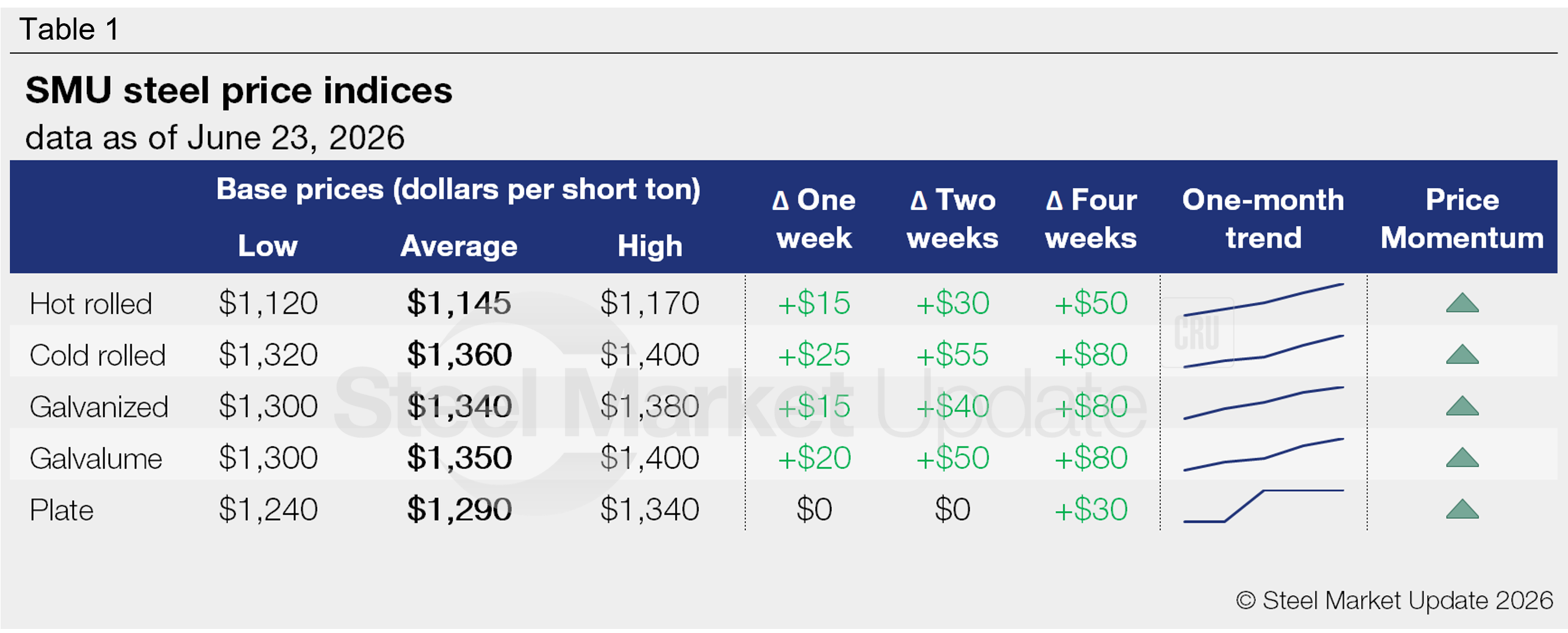

SMU’s hot-rolled (HR) coil price now stands at $1,145 per short ton (st) on average, up $15/st from last week and up $50/st from a month ago.

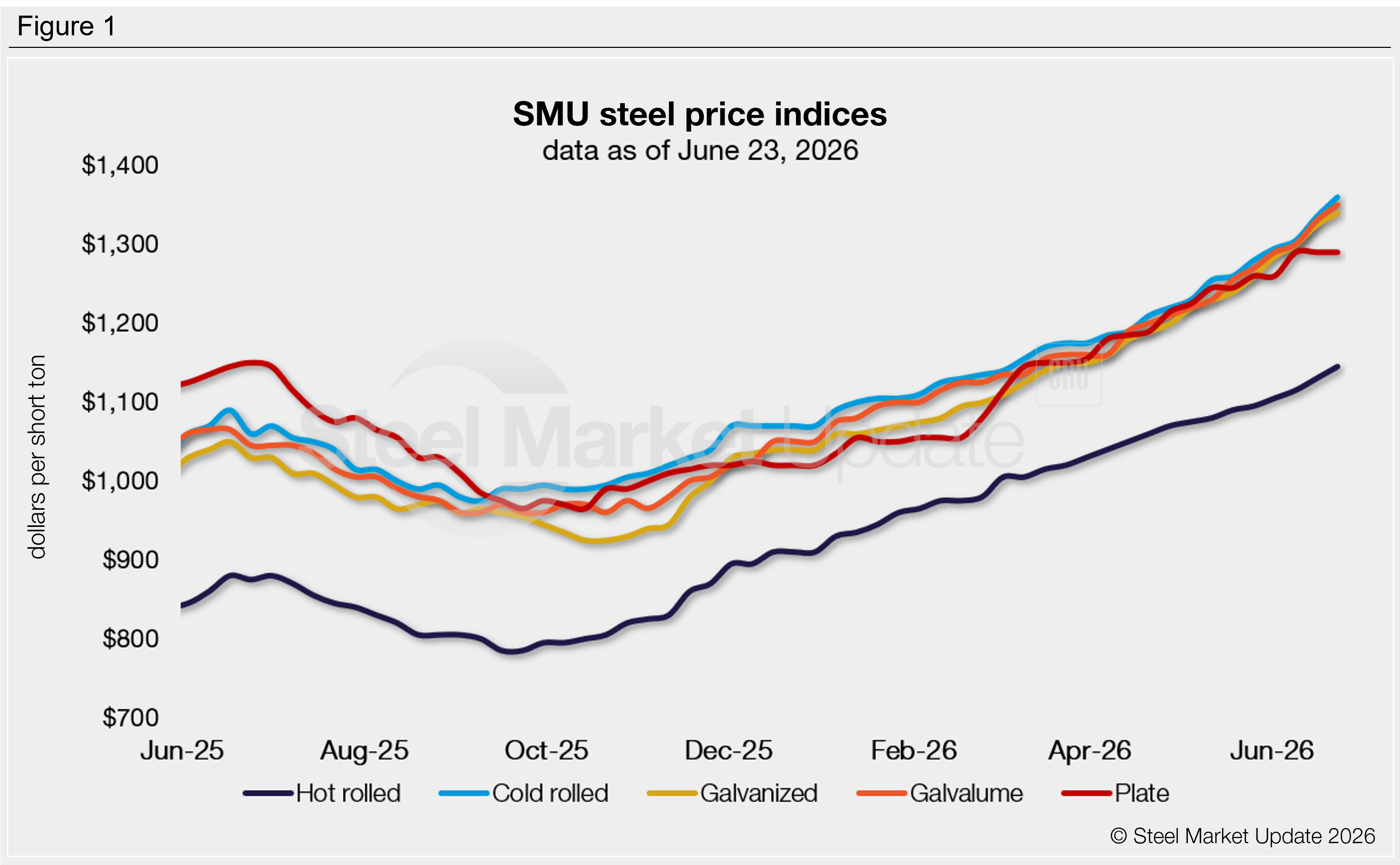

HR prices are also at their highest point since April 2023 – more than three years ago. It’s a similar story with cold-rolled and coated products.

And some sources said the very idea of a HR spot price was almost theoretical. Why? There are few tons available outside of contracts, and some mills have closed July order books but not yet opened August.

“No one has any availability, and I don’t know what’s going to change that,” one Midwest service center source said. The good news, he said, is that demand remains firm. “I can’t make a bad buy. If I can find it, we can sell it.”

Market participants said there was generally more availability when it comes to coated material, even if spot prices remain elevated.

Prices for tandem products continue to rise as fast or faster than those for HR. Cold rolled (CR) was up $25/st week over week (w/w). Galvanized base was up $15/st w/w. And Galvalume was up $20/st w/w. The result: the spread between base prices for HR and base prices for CR and coated products has widened to roughly $200/st on average.

Plate prices held steady at $1,290/st on average.

Most market participants think prices will continue to move upward in the short term. The main point of disagreement is among buyers who think prices might peak in late Q3 or Q4 and those who think prices will continue to rise into 2027.

“Demand isn’t bad at all. I’m just not sure whether it’s strong enough to absorb imports plus restarted capacity in Q4,” said a second Midwest service center source. He made the comment in reference to the No. 14 blast furnace at U.S. Steel’s Gary Works, which is scheduled to restart in August.

In the meantime, SMU’s price momentum indicator remains at “higher” for both sheet and plate products, reflecting expectations that prices will continue to increase in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $1,120–1,170/st, averaging $1,145/st

The lower end of our range is up $20/st week over week (w/w), while the top end is up $10/st. Our overall average is up $15/st w/w.

Hot rolled lead times range from 5–10 weeks, averaging 7.4 weeks as of our June 11 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil: $1,320–1,400/st, averaging $1,360/st

The lower end of our range is unchanged w/w, while the top end is up $50/st. Our overall average is up $25/st w/w.

Cold rolled lead times range from 7–12 weeks, averaging 9.1 weeks through our latest survey.

Galvanized coil: $1,300–1,380/st, averaging $1,340/st

The lower end of our range is unchanged w/w, while the top end is up $30/st. Our overall average is up $15/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,399–1,479/st, averaging $1,439/st FOB mill, east of the Rockies. Note that this spec includes $99/st in mill extras, and extras may vary by mill.

Galvanized lead times range from 6–12 weeks, averaging 8.8 weeks through our latest survey.

Galvalume coil: $1,300–1,400/st, averaging $1,350/st

The lower end of our range is unchanged w/w, while the top end is up $40/st. Our overall average is up $20/st w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,900–2,000/st, averaging $1,950/st FOB mill, east of the Rockies. Note that this spec includes $600/st in mill extras, and extras may vary by mill.

Galvalume lead times range from 7–10 weeks, averaging 8.6 weeks through our latest survey.

Plate: $1,240–1,340/st, averaging $1,290/st

Our range is unchanged w/w.

Plate lead times range from 6–10 weeks, averaging 8.1 weeks through our latest survey.

Brett Linton

Read more from Brett Linton