SMU Price Ranges: Sheet and plate markets tick higher

Prices for both sheet and plate products climbed higher this week, with some rising to multi-year highs, according to SMU's latest market canvass.

Prices for both sheet and plate products climbed higher this week, with some rising to multi-year highs, according to SMU's latest market canvass.

Heating and cooling equipment shipments declined in January to the second-lowest rate recorded over the past nine years.

US steel exports jumped 33% in January but remain historically low, according to recently released US Department of Commerce data.

Raw steel production declined last week for the third-consecutive week but remains historically strong, per AISI.

The Canadian government has placed limits on salaries, bonuses, and other forms of compensation for top executives at Algoma Steel, according to a local media report.

Steel imports remained close to multi-year lows in January and February, according to US Commerce Department data released this week.

This week sources said spot prices on hot-rolled coils increased modestly.

The latest tally of active oil and gas rigs increased in the US this week but declined in Canada, according to figures recently released from Baker Hughes.

A month ago, the steel market was defined by stability. Prices had firmed and held, and the HRC futures curve appeared to be absorbing strength and follow-through rather than rejecting it. Since then, that stability has evolved into something more meaningful, repricing.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Nucor Plate Group notified customers it is increasing prices on all rolled products by $40 per short ton (st) and $60/st on all heat treat products.

SMU's sheet and plate prices were flat or higher this week in a US market that remains characterized by extended lead times and limited spot availability.

This CRU insight demonstrates how the conflict in Middle East supports metallurgical coal prices and iron ore will be impacted by a potential decline in demand from China and rising costs, while the pellet market will be severely disrupted.

The state of the US export market for recycled ferrous scrap is in extreme flux due to events of the last 10 days.

Raw production has trended upwards since the start of the year, reaching a four-year high in February.

The Dodge Momentum Index (DMI) pulled back in February, as planning momentum normalized after a strong second half of 2025.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $1,010 per short ton (st), up $5/st from last week.

Participants in the US hot- and cold-rolled sheet market cautiously called the week a win as prices inched north and demand picked up.

Steel buyers remain optimistic for their current and future business prospects, though not as strong as they did one year ago.

SMU’s March ferrous scrap market survey results are now available on our website to all premium members.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

The main impact on the ferrous value chain from the Middle East conflict will be the higher energy costs in a prolonged scenario.

Following extensions in February, steel mill lead times held steady or extended further for both sheet and plate products this week, according to buyers responding to our latest market survey.

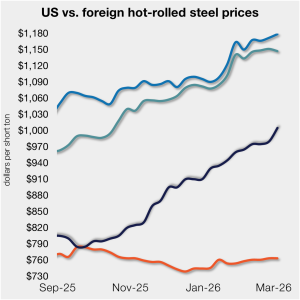

The price gap between US hot-rolled coil (HR) and landed offshore product tightened this week, as stateside tags continue to rise.

Most steel buyers responding to our market survey this week said domestic mills remain unwilling to negotiate lower prices for new spot orders.

Economic activity across the US increased at a light-to-modest pace in seven of the 12 Federal Reserve Districts, according to the US Federal Reserve’s latest Beige Book report.

US steel shipments increased sequentially and on-year in January, according to the latest data from the American Iron and Steel Institute (AISI).

The American Metals Supply Chain Institute (AMSCI) said increasing insurance premiums, potential vessel diversions, and contractual risk evaluations began in the global freight market as geopolitical conflict escalates in the Persian Gulf region.

SMU's sheet and plate prices increased this week to new multi-month highs.

The US surpassed Japan in annual steel production in 2025 for the first time in 26 years, according to the World Steel Association (worldsteel).