Dodge Momentum Index rises 7% in December

The Dodge Momentum Index (DMI) increased from November to December, according to the latest data released by Dodge Construction Network (DCN).

The Dodge Momentum Index (DMI) increased from November to December, according to the latest data released by Dodge Construction Network (DCN).

Steel mill lead times increased for both sheet and plate products this week, according to responses from SMU’s latest market survey.

US steel shipments fell month over month in November but rose year over year.

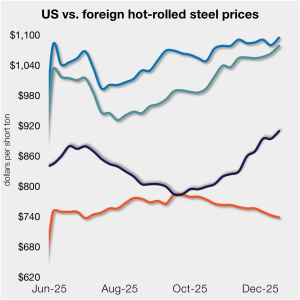

Steel sheet and plate prices rose across the board to start the year on limited spot availability at some mills, expectations of higher scrap prices, and hopes of stronger demand in 2026.

Domestic raw steel production inched higher last week but remains low compared to recent months, according to the latest data released by the American Iron and Steel Institute (AISI)

The Chicago Business Barometer increased in December after hitting an 18-month low in November, according to Market News International (MNI) and the Institute for Supply Management (ISM)

The Institute for Supply Management’s (ISM) latest report finds that December 2025’s market conditions in the manufacturing sector continued to soften.

The latest American Iron and Steel Institute (AISI) data confirms that US steel mills have pulled back production during the end-of-year holiday season. Still, year-to-date figures show higher output and utilization rates compared with last year.

The number of oil and gas rigs operating in the US ticked higher this week, while Canadian activity tumbled, according to the latest data released from Baker Hughes.

The total amount of raw steel produced around the world slipped 3% from October to an estimated 140.1 million metric tons (mt) in November, according to World Steel Association (worldsteel) data. This marks the lowest monthly production rate since December 2023.

Domestic raw steel production edged lower last week, according to the latest data released by the American Iron and Steel Institute (AISI).

Metalforming manufacturers are more upbeat on the prospect of improved near-term economic activity despite lower shipping levels in December, according to the Precision Metalforming Association’s (PMA) December report.

The US and Canadian rig counts both fell this week, according to the latest Baker Hughes data released on Friday, Dec. 19.

SMU’s Mill Order Index (MOI) declined in November after surging the month prior. The fall came as service center intake levels sharply declined, supported by a cut in shipments, according to our latest service center inventories data.

The price gap between stateside hot band and landed offshore product continues to narrow, inching closer toward parity. The premium is now, on average, at its lowest level since July.

Architecture firms across the United States continued to grapple with weak billings in November, amid uncertain economic conditions, according to the AIA.

Apparent steel supply rose to 8.64 million short tons in September, driven primarily by higher domestic mill shipments despite a sharp drop in finished imports.

In this Premium analysis we examine North American oil and natural gas prices, drill rig activity, and crude oil stock levels through December

Following last week’s pause, SMU’s price indices were overall steady to higher this week, holding at or near multi-month highs.

US shipments of heating and cooling equipment fell 11% in October from September to the lowest monthly rate of the year, and an eight-year low, according to AHRI.

Following August’s modest 4% uptick, the volume of steel shipped outside of the country slipped 8% in September to 594,000 short tons, according to recently released data from the US Department of Commerce.

The volume of raw steel produced by US mills ticked higher last week, according to the latest figures published by the American Iron and Steel Institute (AISI).

Business activity in New York state retreated in December, according to the Empire State Manufacturing Survey conducted by the Federal Reserve Bank of New York.

According to recently finalized US Commerce Department data, US steel imports tumbled to a near five-year low in September

US plate market participants hope the new year will bring favorable market conditions. But they remain leery of making big purchases because of lingering uncertainty.

The latest SMU’s Steel Buyers’ Sentiment Indices showed mixed results.

The US rig count edged down this week while the Canadian count inched up, according to the latest Baker Hughes data released on Friday, Dec. 12.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

Steel mill lead times held relatively steady this week on both sheet and plate products, according to responses from SMU’s latest market survey.

Less than half of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price on new spot orders