US CR tags still nearly 30% more than imports

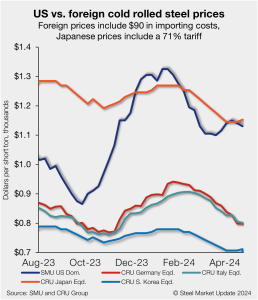

Foreign cold-rolled (CR) coil remains much less expensive than domestic product, according to SMU’s latest check of the market.

Foreign cold-rolled (CR) coil remains much less expensive than domestic product, according to SMU’s latest check of the market.

If successful in its overtures to Anglo American, BHP will create the world’s largest diversified miner by a country mile. The rationale for this merger is scale and in mining, size matters.

Hot-rolled coil and plate lead times contracted this week, with most other products remaining flat, according to SMU's most recent survey data. Cold-rolled products, however, saw lead times extend 0.1 weeks to an average of 7.5 weeks vs. two weeks earlier. Hot rolled and plate lead times both contracted 0.3 weeks from our last market check.

Sheet steel buyers said mills are more willing to talk price on spot orders, according to our most recent survey data.

Steel imports held steady in March, up just 1% from February according to preliminary Census data released earlier this week.

Algoma Steel Inc. expects to wrap up a previously announced outage on its plate mill by the end of this month, a company spokeswoman said. The outage is part of the Canadian flat-rolled steelmaker’s $130 million CAD ($95 million USD) modernization project. It began in mid-April.

Lower demand and prices for steel plate impacted SSAB Americas’ results in the first quarter, Swedish parent company SSAB said in its Q1'24 interim report.

Cleveland-Cliffs is working on a solution for its recently idled mill in Weirton, W.Va., that will address pent-up demand for transformers, increase the need for its electrical steel, and get its workforce back to work.

Sheet prices were again mixed this week – all seemed to highlight the momentum shift seen over the past two weeks.

Cleveland-Cliffs Inc. continued to lose money in the first quarter, with the steelmaker blaming the loss in part on the idling of its tinplate facility in Weirton, W.Va.

Zekelman Industries will invest up to $120 million to expand the manufacturing capabilities and product offerings of its Atlas Tube subsidiary in Mississippi County, Ark.

Last week gave us a glimpse into the effect of the 2024 election campaign on trade policy. In a major announcement, the Biden administration pressed the US Trade Representative (USTR) to triple certain Section 301 tariffs on steel and aluminum. It’s a lot to unpack. You can find the full text of the announcement here. […]

Steel sheet prices in many regions of the world were steady week over week in the week ended April 17.

After receiving a hefty federal tax credit, ArcelorMittal plans to produce non-grain-oriented electrical steel (NOES) in Alabama. ArcelorMittal Calvert LLC received a tax credit of $280.5 million for the project, according to a Department of Energy (DOE) announcement on Friday. The Qualifying Advanced Energy Project Credit (48C) tax credit is meant to accelerate clean energy […]

Drilling activity increased in the US but declined in Canada, according to the latest data from Baker Hughes.

The steel market appears to be finding a new, higher normal with the shocks of the pandemic and the Ukraine in the rearview mirror. The good news: a more profitable and consolidated post-Covid US steel industry has been able to invest in operations. That includes efforts to decarbonize. The bad news: That “new normal” could be tested. Because it’s not just domestic sheet prices that have been volatile. Geopolitics are too.

Sheet prices varied this week. While hot-rolled (HR) coil pricing was largely flat, cold-rolled (CR) coil and tandem product pricing eased slightly reflecting the momentum shift seen last week for HR coil. SMU’s average HR coil price was flat from last week at $835 per short ton (st) – potentially emphasizing the tension between competing […]

Does the price of ferrous scrap depend on the price of finished steel product? And how much of an influence do billet and slab prices have on scrap prices?

Drilling activity decreased in the US but rose in Canada in the week ended April 12, according to the latest data from Baker Hughes.

The market appears to be taking a pause after the heavy buying that occurred in March.

For those of you old enough to remember The King and I, the April scrap market seems to be a puzzlement. While it is now clear that everything went sideways, one could clearly make an argument for prices to have been down.

Over the last several years, I have noticed widening spreads between #1 Heavy Melting Steel (ISRI 201) and Shredded (ISRI 210,211), as well as Plate & Structural (ISRI 232).

Sheet prices saw a slight momentum shift this week after consecutive gains in the prior two weeks. Plate edged lower on greater competition off easing demand, according to our latest check of the steel market.

The number of active rigs in the US eased to a nine-week low, while Canadian activity continued it’s seasonal wind down.

April scrap prices came in sideways in the US, sources told SMU.

Low manufacturing activity and higher interest rates took a toll on Radius Recycling’s profits during the Oregon-based company’s most recent quarter. Radius reported a net loss of $34 million, or $1.19 per share, during its fiscal second quarter. In the previous quarter, Radius saw a net loss of $18 million, or 64 cents per share.

Steel shipments from US mills were lower in February, both from January and from last year.

Several large buyers in the North came into the market on a sideways basis from prices paid in March. The development comes after recent speculation about what prices US-based steelmakers would pay for scrap for April shipments.

On the eve of the April ferrous scrap buy, there is no firm consensus on the market’s direction. The safe predictions are “soft” sideways to “strong” sideways. That may mean down $10 per gross ton (gt) to up $10/gt.

Sheet prices moved higher this week for the second consecutive week, while plate prices ticked lower, according to our latest canvas of the steel market.