SMU Survey: Steel Buyers' Sentiment Indices increase

SMU’s Steel Buyers’ Sentiment Indices both rose this week, with Current Sentiment rebounding 14 points.

SMU’s Steel Buyers’ Sentiment Indices both rose this week, with Current Sentiment rebounding 14 points.

Most steel buyers responding to our market survey this week reported that domestic mills are considerably less willing to talk price on sheet and plate products than they were in recent weeks.

Ternium closed the third quarter with steady shipments and improving margins. But trade policy uncertainty and subdued demand in Mexico weighed on the Latin American steelmaker’s results.

Steel mill lead times marginally extended for both sheet and plate products this week, according to responses from SMU’s latest market survey.

Flack Global Metals (FGM) announced Thursday that it would expand into Texas by assuming the Houston operations of NSPS Metals.

North American auto assemblies declined in September, down 5.1% vs. August. And assemblies were also down 1% year on year.

Algoma Steel’s net loss more than quadrupled in the third quarter on trade woes and its EAF transition. Separately, the company announced a change in leadership, as CEO Michael Garcia will retire at the end of the year.

Algoma Steel Group Inc. CEO Michael Garcia will retire at the end of the year, the company said on Tuesday. Rajat Marwah, CFO of the Canadian flat-rolled steelmaker, will be appointed president on Nov. 1 and CEO on Jan. 1.

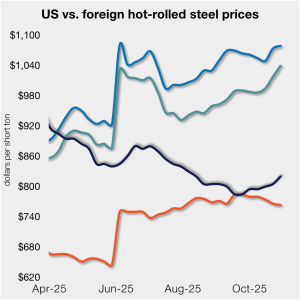

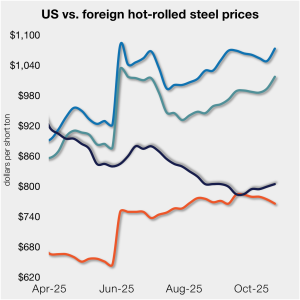

In dollar-per-ton terms, US product is on average $141/st less than landed import prices (inclusive of the 50% tariff). That’s down from $148/st last week.

Executives framed the all-stock deal as a path to scale, efficiency, and long-term growth despite ongoing weakness in the metals market.

SMU’s hot-rolled coil price increased for a third consecutive week. And the gains were more pronounced this time following a price hike initiated on Friday by NLMK USA.

Sheet steel indices increased across the board this week, while plate prices held steady. All five of SMU’s price indices are higher than they were two weeks ago, and all but one are above levels recorded four weeks ago.

National service center chains Ryerson Holding Corp. and Olympic Steel Corp. have announced a merger between the two companies.

Nucor entered the fourth quarter with clear forward momentum: stronger-than-expected results, solid sheet and plate demand, and construction progress on a major new mill that should add capacity next year.

NEMO Industries CEO talks cost and reasoning behind a $3-billion pig iron project in Louisiana.

Nucor has pulled the plug on a planned rebar micro mill in the Pacific Northwest.

Domestic mill production inched higher last week, according to the latest figures released by the American Iron and Steel Institute (AISI). Prior to the start of this month, raw output had remained historically strong since June.

SMU digs into the vault to look back at an old survey, and to tell what exciting things are still to come.

US President Donald Trump took to social media late Thursday night to announce he was canceling trade talks with Canada.

US buyers want to drop pig iron prices to levels commensurate with the decline in prime scrap in their domestic market. Prime price shed $20 per gross ton (gt) in September and another $20/gt in October.

GrafTech reported higher shipments and sales in the third quarter, but continued to lose money. It attributed the continued losses to persistent pricing pressure and global trade uncertainty.

Baker Hughes reported higher oil and gas drilling activity this week in both the US and Canada.

As another month goes by and another futures columnist starts by saying “not much to see here,” I understand that a reader might flip their brain to skim mode.

Below are some other issues that should be on your radar. Because while prices have been steady, a lot is going on when it comes to news that could impact them.

World crude steel output declined for the fourth-consecutive month in September, slipping 3% from August to an estimated 141.8 million metric tons (mt), according to the latest figures from the World Steel Association (worldsteel).

What's on steel buyers' minds this week? We asked about market prices, demand, inventories, tariffs, imports, and other evolving market trends. Read on for buyers' comments in their own words...

Demand for plate on the spot market remains soft by comparison to years past. However, this week regional demand variations grew more pronounced.

SMU’s average price for domestic HR coil moved $5 higher this week, while price movements in offshore markets varied. This dynamic...

There has been renewed activity in the scrap export market in the Mediterranean Basin during the last week. Most of the activity occurred in Northern Europe and the Baltic regions with prices basically staying sideways to up slightly.

The Americas segment of Swedish steelmaker SSAB delivered a stable third quarter, but with weaker shipments and continuing cautious demand. Plate prices held, but tariffs, slowing end-user demand, and...