US rig count ticks higher, Canada falls

The latest Baker Hughes rig count report showed oil and gas drilling improved in the US this past week, while Canada saw its rig count decline.

The latest Baker Hughes rig count report showed oil and gas drilling improved in the US this past week, while Canada saw its rig count decline.

Contract talks for U.S. value-added aluminum products are reaching a critical stage, with billet, primary foundry alloys, and wire rod upcharges diverging as buyers and producers race to finalized 2026 pricing.

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Past survey results are also available under that selection. If you need help accessing the survey results, or if […]

US sheet market participants say demand for hot- and cold-rolled coils has not increased, leaving them confused by mill price increases and average lead times.

Steel mill lead times extended marginally this week on most sheet products but declined for plate, according to responses from SMU’s latest market survey.

Just over half of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price on new spot orders. Mills have begun to hold a firmer stance on prices over our last two surveys.

NLMK USA is aiming to increase base prices on all products, effective immediately.

The price spread between HRC and prime scrap has widened for a second month, based on SMU’s most recent pricing data.

Plate market participants anticipated price increases from domestic producers. For weeks, sources predicted an increase. No one, however, was sure of timing due to subdued demand. Following the news that JSW increased its spot market plate prices by $40 per short ton (st), sources said they anticipate more mills will begin rolling out increases. From […]

US-flagged shipments of iron ore on the Great Lakes are on the decline. Ore shipments in October were the lowest they’ve been for that month in five years.

SMU's sheet and plate steel prices moved higher in unison this week.

US steel and manufacturing industries say they face a new set of uncertain market factors due to the government’s shutdown and the potential repeal of “reciprocal” tariffs.

ArcelorMittal sees green shoots in North America despite tepid demand.

Steel Dynamics Inc. announced Matt Bell as the new head of the company’s metals recycling platform, OmniSource.

JSW Steel USA aims to increase steel plate prices by at least $40/short ton.

Flat-rolled metals processor and pipe manufacturer Friedman Industries achieved record sales volume in its fiscal second quarter.

Domestic steel production increased last week, according to the latest figures from the American Iron and Steel Institute (AISI). Production has trended higher since mid-October, though it is not as strong as output seen over the summer months.

Russel Metals posted mixed financial results in its third-quarter earnings report. The Mississauga, Ontario-based metals processing and distribution company generated Canadian $35 million (US$53.5 million) in net income for Q3'25, representing a 1.4% increase from the same quarter in 2024.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton on Monday, Nov. 10.

North America continues to anchor Klöckner & Co.’s performance in 2025. The Kloeckner Metals Americas segment delivered robust earnings in the third quarter despite softer steel prices.

The Dodge Momentum Index (DMI) fell more than 7% in October, sliding for the first time in six months. Still, the index is up 35% year-to-date, according to the latest data released by Dodge Construction Network.

The latest Baker Hughes rig count report showed oil and gas drilling improved in both the US and Canada in the first week of November.

Nippon Steel is positioning U.S. Steel as a cornerstone of its global growth strategy, highlighting the US as the most developed and demand-rich market, especially for premium steel products used in the automotive, energy, and infrastructure sectors.

Tania Archibald will assume the role of managing director and chief executive at the Melbourne-based company as of Feb. 1, 2026.

AMU's latest survey of aluminum market participants shows widening gaps in lead times, with extrusions lengthening dramatically.

Nippon Steel is making good on the big capex promises it made to secure its purchase of United States Steel Corp. This week, the Japanese company and American steelmaker together unveiled various capital investments they plan to make across U.S. Steel’s footprint.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

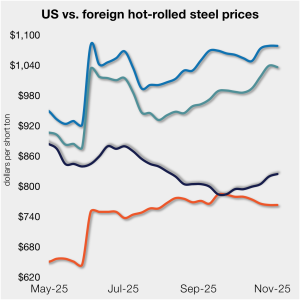

The gap between US hot band prices and imports narrowed slightly. But with the 50% Section 232 tariffs, most imports remain more expensive than domestic material.

Latin American steelmaker Ternium SA is increasing its stake in Brazilian flat-rolled steel producer Usiminas.

ArcelorMittal Dofasco and Stelco joined recent moves by US mills to push sheet prices higher.