Final Thoughts

Is a pattern finally emerging in the post-Liberation Day tariff landscape?

Is a pattern finally emerging in the post-Liberation Day tariff landscape?

Sheet and plate prices were flat or lower again this week on continued concerns about demand and higher production rates among US mills.

SMU’s Mill Order Index (MOI) moved higher in July after rebounding the month prior. The shift comes after mill orders declined from March through May.

Prices remain subdued in US pig iron market, sources said.

Don't be puzzled. Solve our crossword, and get ready for Steel Summit 2025!

With so much happening in the news cycle, we want to make it easier for you to keep track of it all. Here are highlights of what’s happened this week and a few things to keep an eye on.

While boarding Airforce One on Friday, US President Donald Trump stated that he would be setting more steel tariffs and putting ~100% tariffs on semiconductors and chips.

Cleveland-Cliffs Inc. has reportedly signed "unusually long" fixed-price supply agreements with multiple US automakers.

U.S. Steel, Allegheny County executive Sara Innamorato, and Pennsylvania Gov. Josh Shapiro clarified details from early reports about the Clairton Coke Works facility explosion just one day earlier.

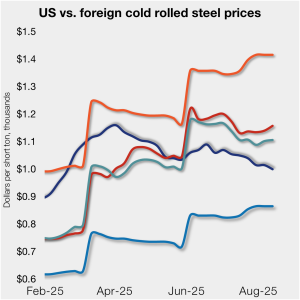

Cold-rolled (CR) coil prices continued to decline in the US this week, while prices in offshore markets diverged and ticked higher.

Reporting and enforcing steel tariffs are two top–of-mind concerns for US manufacturers, the US Customs and Border Protection agency, importers, and others across the supply chain.

In July, US service centers’ flat-rolled steel supply increased month on month, following the seasonal summer trend of inventory build with slowing shipments.

We're getting ready to initiate the 10-day countdown until Steel Summit 2025 in Atlanta. Liftoff is on Aug. 25, and the conference goes through Aug. 27. With the speed at which things have moved this year, it will be great to take a breath and reflect on what's happened so far.

Market participants said they have high hopes that the stable hot-rolled spot market will improve as the year rolls on.

On Monday and Tuesday of this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

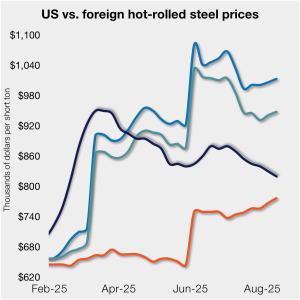

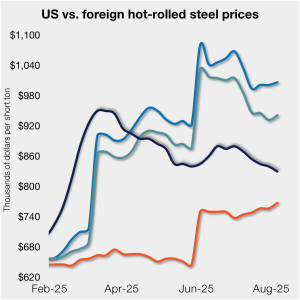

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices ticked higher again week over week (w/w).

The price spread between prime scrap and hot-rolled coil (HRC) narrowed in August, according to SMU’s most recent pricing data.

The latest SMU Community Chat webinar reply featuring Lewis Leibowitz, trade attorney and SMU columnist, is now available on our website to all members.

Yesterday’s tragedy and loss of life at U.S. Steel’s Clairton Works is a stark reminder of how important safety in the workplace really is.

All five of SMU's steel sheet and plate price indices declined this week, falling to lows last seen in February.

Sources in the carbon and alloy steel plate market said they are less discouraged by market uncertainty resulting from tariffs or foreign relations, but are instead, eager to see disruption to the flat pricing environment.

Total heating and cooling equipment shipments eased from May to June, according to the latest data released by the Air-Conditioning, Heating, and Refrigeration Institute.

The amount of finished steel coming into the US market increased 3% from May to June, climbing to one of the highest rates seen in recent years, according to SMU’s analysis of Department of Commerce and American Iron and Steel Institute (AISI) data

US steel mills have ramped up output since April, with weekly production increasing in all but four of the past 16 weeks.

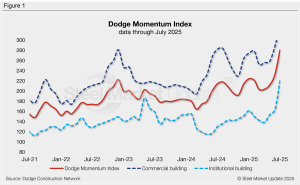

The Dodge Momentum Index (DMI) jumped 20.8% in July and is now up 27% year-to-date, according to the latest data released by Dodge Construction Network.

Nucor has implemented a double-digit price decrease on spot hot-rolled (HR) coil for the second consecutive week.

What are our scrap survey participants saying about the market?

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices increased week over week (w/w).

Oil and gas drilling in the US slowed for a third consecutive week, while activity in Canada hovered just shy of the 19-week high reached two weeks prior.

This week’s SMU survey reveals that a growing number of steel market participants are weary of tariffs and are awaiting evidence of progress reshoring. At the start of 2025, now-second-term President, Donald Trump, pronounced that his plan to implement tariffs would result in increased revenue for the US.