Tepid sheet market conditions preceded wintry weather mix: Sources

Participants in the hot- and cold-rolled coil markets said winter storms in the East and Midwest may disrupt weekly order volumes and prices.

Participants in the hot- and cold-rolled coil markets said winter storms in the East and Midwest may disrupt weekly order volumes and prices.

At SMU, we ask the big questions: To be or not to be? Hot band at a grand? On the one hand, whether hot-rolled coil price can or can’t go above $1,000 per short (st) is a silly argument. It’s just a number. On the other hand, round numbers are something that we tend to fixate on. They can be psychologically important to a market – even if they shouldn’t be.

All but one of the steelmaking raw materials we track increased in price over the last month

A coalition of US steel industry CEOs has formally urged President Trump to maintain—and fully enforce—current Section 232 tariffs on steel and steel‑containing goods.

SMU interviews Worthington Steel CEO Geoff Gilmore about the recent Kloeckner & Co. buy.

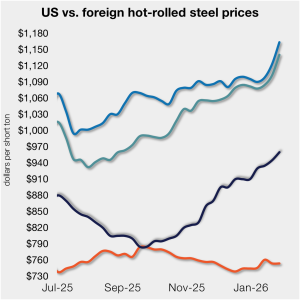

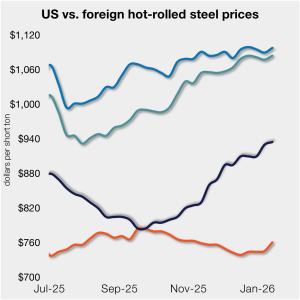

The price gap between US hot-rolled coil and landed offshore product inched higher, even as prices stateside and abroad mostly moved in tandem vs. last week.

SMU polled steel buyers on an array of topics earlier this week, ranging from market prices and demand, to inventories, imports, and evolving market events.

The pig iron market has entered an upward phase now that ferrous scrap in both Europe and North America has also been increasing in price.

What do SMU's latest survey results show about the current market take on tariffs and where HRC prices are going?

Sheet prices mostly continued their uneven but steady march higher this week, according to SMU’s latest check of the market.

Alton Steel Inc. (ASI), a special bar quality (SBQ) steel producer, said it will close operations later this week.

The US scrap market has come under pressure due to the extremely debilitating winter weather across the eastern half of the country.

President Donald Trump in a post on Truth Social threatened to impose 100% tariffs on all exports from Canada into the US. It would be boastful (but not entirely inaccurate) to say you read it in SMU and heard it on Aluminum Market Update (AMU) first.

A trip to Tampa is the perfect remedy for the winter blues. The 37th annual Tampa Steel Conference will bring together executives from across the steel supply chain, as well as leading analysts and policy experts.

A report on the sheet market this week.

SMU columnist Daniel Doderer looks out over the economy as it regards the steel industry.

SMU’s Steel Buyers’ Sentiment Indices both increased this week to multi-month highs

The total amount of raw steel produced around the world slipped 0.4% from November to an estimated 139.6 million metric tons (mt) in December, according worldsteel data.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

A crossword featuring clues about SMU's Tampa Steel Conference 2026.

Architecture firms across the US continued to face weak business conditions through the end of 2025, as economic conditions added to the uncertainty, said AIA.

Steel mill lead times held steady on most products this week following the surge seen in early January, according to responses from SMU’s latest market survey

The plate market’s swell of optimistic sentiment marking the start of 2026 dissipated this week.

The price gap between US hot-rolled coil (HR) and landed offshore product has been relatively flat to begin the year.

Just over a third of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price to secure new spot orders.

The Italian authorities have seized a Russian cargo of hot-briquetted-iron (HBI) for violating European sanctions on Russian ferrous imports, according to media reports.

Does the level of geopolitical uncertainty get to the point where it impacts not only the stock market but also the broader steel market? Could we see a repeat of Liberation Day, or will the news cycle move on to something else by the end of the week? I don't pretend to know what might happen in Davos. Suffice it to say, it’s going to be a newsy week.

The volume of raw steel produced by US mills grew last week, holding on to the gains seen the prior week, according to the latest figures released by the American Iron and Steel Institute (AISI).

SMU’s sheet price indices climbed to new multi-month highs this week, while plate prices marginally declined.

Speculation has already begun on what February has in store for the US scrap market after it rose $20-30 per gross ton (gt) in January,