Trump to impose new tariffs after SCOTUS rules IEEPA usage illegal

The latest 10% tariff is expected to be enacted over the next several days using Section 122.

The latest 10% tariff is expected to be enacted over the next several days using Section 122.

Global steel plate prices are expected to trend upward as North American restocking and European regulatory costs will drive the market, even as recovery in Asian markets remains gradual and cost-dependent.

The latest Baker Hughes rig count report shows steady drilling for oil and gas in the US, while drilling in Canada improved slightly.

Participants in the domestic sheet market say they experienced lighter inquiries and fewer orders than in previous weeks, rendering domestic mill price increases for spot-market hot- and cold-rolled coils irrelevant.

The spread between domestic hot-rolled coil and prime scrap prices widened slightly in February. It has been trending in that direction since October.

SMU's Steel Buyers’ Sentiment Indices continue to show that steel buyers are optimistic for their businesses’ chances of success.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

SMU’s Mill Order Index (MOI) rose again in January, maintaining momentum from the month prior. The increase came as service center intake levels ticked up, supported by a jump in shipments, according to our latest service center inventories data.

Waiting for possibly more changes to tariffs.

Hot rolled and galvanized lead times are about half a week longer than they were three months ago, while production times for cold rolled, Galvalume, and plate products are one to two weeks longer.

The export scrap market from both North America and Europe has quieted down over the last week.

US ferrous scrap prices continued to rise in February, scrap sources told SMU.

Since late 2025, mills have begun to hold a firmer stance on prices, tightening their grip at the start of this year and holding on since

The final panel of last week’s Tampa Steel Conference brought together executives from three different service center, all of which were optimistic for 2026.

Once wintery weather gives way to sunnier spring conditions, plate sources foresee the market accepting the $50-60 per short ton spot price increases issued by Nucor Plate Group, Oregon Steel Mills, and SSAB.

The extreme cold we've seen over the last month or so might be passing. But it's still stormy out there when it comes to trade issues. The latest trade matter that’s led to more pings than usual on my phone and in my inbox: Ternium México filed a trade petition against imports of cold-rolled (CR) coil from China, Malaysia, and the United States.

Three of SMU’s price indices increased this week, while two remained steady, all holding at multi-month highs.

US service centers’ flat-rolled steel supply declined in January, after trending higher in December. Shipping days of supply slipped to 58.5 on an adjusted basis at the end of January, according to SMU data.

Barry Zekelman used his Tampa Steel Conference fireside chat to deliver one of the bluntest assessments yet of the forces shaping North American steel. He warned that a flawed tariff structure and an impending power crunch threaten the industry more than most realize.

US ferrous scrap prices rise in February.

I want to say a big thank you to everyone who attended the Tampa Steel Conference. More than 600 people – smashing the record we set last year.

Following November’s nine-year low, heating and cooling equipment shipments rebounded 19% in December.

Last week, news stories (first in the Financial Times) appeared that the Trump administration was working on adjustments to steel and aluminum derivative tariffs. Ostensibly, these tariffs are only imposed on the steel or aluminum “content” of derivative products. But Customs has not provided clear guidance on how to calculate content. Confusion and controversy are running rampant.

Tales from the sidelines of Tampa Steel Conference 2026.

A narrow range has emerged, suggesting the market’s repricing of downside risk is starting to stick.

Hot-rolled coil hovering near $970 per ton could push toward $1,000, but Timna Tanners cautioned at the Tampa Steel Conference that anything “much above that” becomes difficult to sustain. Still, she argued that mills’ slow, disciplined price increases are working in their favor.

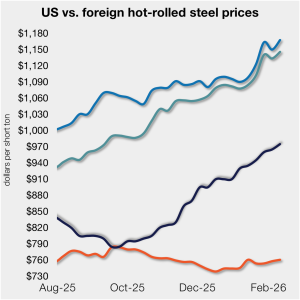

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product was largely flat this week, as price movements stateside and abroad mirrored each other. Still, the premium for US hot band over imports has remained in a relatively tight band since early December.

SMU’s sheet price indices inched up to new multi-month highs this week, while plate prices held steady.

Gone conferencin'. Yes, it's about that time when some of our staff are already en route to Florida, as the Tampa Steel Conference kicks off on Wednesday.

There has been some recent activity of exports of basic pig iron from Brazil. Sources there agree on the activity but diverge on the pricing. What is new to the market in Brazil is the buying interest from the European Union, in particularly, Italy.