Cliffs opens May spot order book at $975/ton HR

Cleveland-Cliffs opened its May order book for spot material at $975 per short ton (st).

Cleveland-Cliffs opened its May order book for spot material at $975 per short ton (st).

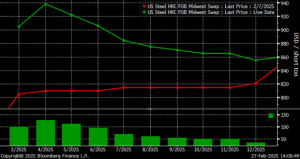

A look at the HR futures market.

This week is the first time all of our indices have moved lower in unison since July 2024.

The imposition of reciprocal tariffs by President Trump as explained on Wednesday afternoon has rattled virtually every market. This policy has some advantages for the steelmaking sector, but there may be some disadvantages that were not considered, especially for the EAF producers of flat-rolled.

Nucor’s consumer spot price (CSP) for hot-rolled (HR) coil remains unchanged again this week. The pause over the past two weeks stands in contrast to the nine-week rally that saw the company increase prices regularly by double-digits. The Charlotte, N.C.-based steelmaker told customers on Monday that this week’s consumer spot price (CSP) for HR coil […]

Market dynamics are shifting rapidly, with futures pricing diverging from physical fundamentals, creating a complex landscape for steel traders.

Sheet and plate prices were mixed on Tuesday as the market took a wait-and-see approach to the Trump administration’s “Liberation Day” tariffs.

The price of pig iron for the US market remains firm despite a potential drop in domestic ferrous scrap prices going into April.

Another eventful week in the physical and financial steel markets is coming to a close, but with a markedly different tone than the last update at the end of February.

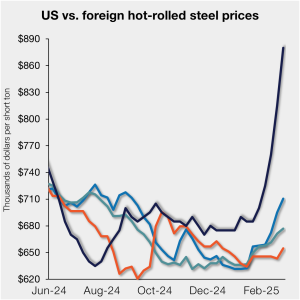

The threat of tariffs over the past two months has been a springboard for US prices. But the Section 232 reinstatement on March 13 narrowed the domestic premium over imports on a landed basis.

SMU's steel price indices moved in differing directions this week but remained largely stable as cautious buyers await clarity on pending steel tariffs and trade cases.

After eight weeks of double-digit price increases on hot-rolled (HR) coil, Nucor slowed the price rise this week with an increase of $5 per short ton.

Over the past couple of weeks, Midwest HRC futures have been drifting lower on light volume. This begs the question if the rally has run out of steam, or is it catching its breath after ripping roughly $150 in less than two weeks? The April CME Midwest HRC future made an intraday high at $976 […]

Steel prices were stable to higher this week for the second consecutive week across the sheet and plate products tracked by SMU. Three of our price indices increased from the previous week, while two held firm.

The HRC vs. prime scrap spread increased again in March.

This marks the eighth week of increases

While overall steel demand remains weak in the near term, there are reasons to expect metallurgical coal prices will increase over the course of the year, Ramaco says.

“The next months are going to be good ones for pig iron producers," according to one source.

Uncertainty has remained a dominant theme in the US ferrous derivatives markets over the past month. And the Trump administration's tariffs on steel and aluminum are still top of mind for market participants.

After over a month of increases, steel prices paused this week for some of the products tracked by SMU. Three of our price indices continued to climb, while two held steady from the prior week.

Nucor has increased its weekly HR coil spot price for seven consecutive weeks.

Headline risk has returned to the ferrous complex, with both hot-rolled coil (HRC) and busheling ferrous scrap (BCH) markets surging in response to fresh trade restrictions.

The majority of the steel buyers responding to our latest market survey reported that domestic mills are not open to negotiating prices on new orders this week.

Steel prices climbed across the board this week, with every steel product tracked by SMU rising to multi-month highs.

Nucor has increased its list price for hot-rolled (HR) coil to $900 per short ton (st), according to a letter to customers on Monday. The Charlotte, N.C.-based steelmaker’s list price for HR is up $40/st from $860/st last week and up $125/st from $775/st a month ago, according to SMU’s mill price announcement calendar. The […]

US plate prices have moved up at a sharp clip over the past three weeks. The gains come on the heels of a unified mill pricing blitz, bolstered by the threat of looming tariffs and the expectation of sharply higher scrap prices. Prices hit their lowest level in more than four years in late January, […]

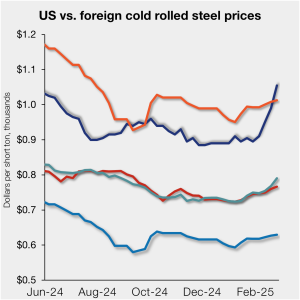

The price spread between stateside-produced CR and imports reached its widest margin in over a year.

Four weeks have passed since the last article from Rock Trading Advisors on January 30. The paint has dried, and Midwest HRC futures have exploded higher in response to President Trump’s declaration of impending 25% tariffs on all imported steel products. The rolling 2nd month CME Midwest HRC future erupted through the top end of its downtrend, one that dates back to the peak of the winter 2022 rally. It also broke out of its narrow range seen dating back to June of last year.

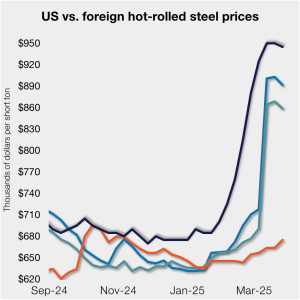

Hot-rolled (HR) coil prices continued to rally in the US this week, quickly outpacing price gains seen abroad. The result: US hot band prices have grown widely more expensive than imports on a landed basis. The premium US HR tags carry over HR prices abroad now stands at a 14-month high. SMU’s average domestic HR […]

One buyer summed up the prevailing sentiment: “Everything is pointing up — pricing, sentiment, order activity. But the real test will come once the immediate reactionary buying subsides. Will there be enough true demand to support these levels through mid-year? That’s the big unknown.”