With the 2023 SMU Steel Summit quickly approaching, SMU is in full-blown planning mode. Our preparations have me reflecting on last year’s event and what I personally can do to better take full advantage of all the opportunities this year’s event will bring.

(Note: CRU and SMU are hosting a free pre-conference webinar on Tuesday, June 20, on how to generate actionable takeaways from this year’s Steel Summit. Click here for more information or to register for the webinar.)

As a journalist covering the event, I took lots of notes last year. You may have seen me and the rest of the SMU team in the front row, heads down, frantically typing away on our computers. We’re not being antisocial, I promise, we are just trying to keep the SMU newsletter chock full of stories for our readers, while also attending the flat-rolled steel industry’s largest event. We’ll be there again this year in the front row – if you see us, stop by and say hello!

Thinking about last year’s event, one of the sessions that surprised me by how much I enjoyed it was the NexGen Metals Community session in which young industry leaders spoke on a variety of topics. I was greatly impressed with each speaker on the panel – they spoke articulately and confidently, knowledgeable and passionate about their topic of choice. The panel was made up of members of the NexGen Steering Group – several of whom are past winners of the NexGen Leadership Award. Hearing them speak, I immediately knew they were very well-deserving of winning that award, which is meant to recognize and celebrate the excellence of emerging leaders in the metals community.

Last year’s winner was Austin Reynolds of Ace Steel Supply, who spent a mentorship day earlier this year with Cleveland-Cliffs’ president and CEO Lourenco Goncalves as part of the award’s winning package. The 2021 winner was Eric Daniel of the NIM Group’s Metalwest who is passionate about bringing change to the steel industry. The 2020 winner was Stephen Serling of Quality Metals Stamping and the winner in 2019 – the first year of the award — was Meredith Meade of Tempel Steel. As you can see, they continue to get recognition long beyond their initial receiving of the award.

Each of the award winners are now a part of the NexGen steering group, along with three other impressive young people in the industry: Ping Liang of ArcelorMittal, Ben Snyder of J. Benjamin Recruitment, and SMU’s own Becca Moczygemba.

The group is leading the NexGen Metals Community in inspiring members to grow into future decision-makers. When I heard them speak at last year’s Steel Summit, I was indeed inspired by each of them and their drive and passion. These are movers and shakers in the industry. Keep your eye out for each of them to continue making moves that push their companies and the industry further.

There’s still time to nominate someone you know for this year’s NexGen Leadership Award – but not much, as nominations close tomorrow! If you know someone in your organization who is 35 years old or younger who exemplifies the best the steel industry has to offer, nominate them for this award. The final three nominees will receive complementary registration, airfare, and accommodations for this year’s Steel Summit conference and the winner will be recognized on stage in front of a huge group of industry peers.

I’m truly looking forward to this year’s event and not only seeing who is chosen as this year’s winner, but in hearing again from the NexGen leaders, as well as all the other distinguished speakers from across the industry.

As always, thank you for reading SMU and being a part of our community. We hope to see you in August in Atlanta!

By Laura Miller, laura@steelmarketupdate.com

Nucor Corp. said its second-quarter earnings should beat those of the prior quarter on strength in all its business segments.

The steelmaker expects its Q2 earnings to be in the range of $5.45 to $5.55 per diluted share. Although down from the $9.67 per share posted in Q2 last year, it’s an improvement upon Q1 earnings of $4.45 per share.

In April, when it released its Q1 earnings in which it posted net income of $1.137 billion on sales of $8.71 billion, the steelmaker expressed confidence that its Q2 results would be better.

Margin expansion at the company’s sheet mills should result in a sequential improvement in the steel mills segment, and improved profitability at its direct-reduced iron facilities will benefit the raw materials segment. The steel products segment’s results will be comparable to the strong performance seen in Q1, Nucor said in a statement on Thursday, June 15.

SMU will cover Nucor’s full Q2 earnings report when it is released on July 25.

By Laura Miller, laura@steelmarketupdate.com

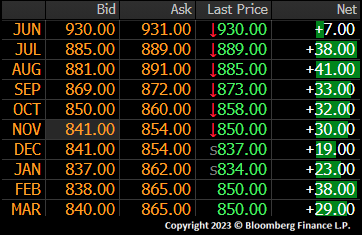

The July Midwest HRC future started February just below $800, rallied $325 in just over a month peaking at $1,115 on March 9. Over the next 81 days, the July future basically went full circle, falling $311 to just over $800 on June 1. Since the start of June, the July future has rallied almost $100 trading to an intraday high of $895 earlier today.

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. Rock provides customers attached to the steel industry with commodity price risk management services and market intelligence. RTA is registered with the National Futures Association as a Commodity Trade Advisor. David has over 20 years of professional trading experience and has been active in the ferrous derivatives space since 2012.

July CME Hot Rolled Coil Future $/st

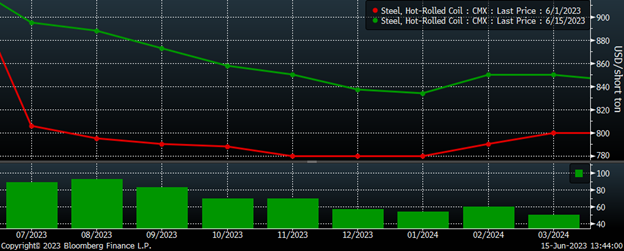

Trading in SGX iron ore futures appeared to have bottomed in early May, banged around in the $100-110 area throughout the month before starting its current rally in June. The motivation behind iron ore’s rally is a new round of stimulus ($140 billion) targeting infrastructure spending and China’s residential real estate market. This also appeared to be the driver of Midwest HRC’s move up, which started just after Beijing made headlines on June 2 that it was considering another stimulus package.

Rolling 2nd Month Iron Ore

Then, U.S. Steel announced a $50-increase to flat-rolled prices yesterday, which resulted in a $20-40 pop in the futures market today.

On June 1, the Midwest HRC futures curve was about flat, ranging between $780-800. Since then, the July future has rallied $83, August $91 and September $83. The October and November futures have gained $70 while the December and Q1’24 months gained somewhere between $50-60. Q3’s outperformance has steepened the futures curve somewhat, with the spread between July and December doubling to $52 from $26.

CME Hot Rolled Coil Futures Curve $/st

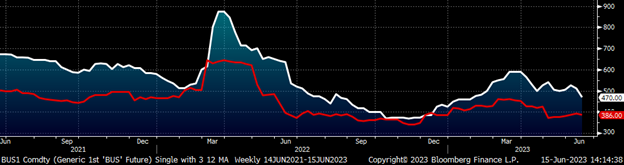

How much of June’s rally has been inspired by additional Chinese stimulus lifting all commodity boats, and how much was in anticipation of the rumored price increase announcements is up for debate. However, what I find most interesting is how the futures market largely ignored June’s much-worse-than-expected $56 decline in busheling.

Front Month Busheling $/lt (wh) & Turkish Scrap $/mt (red)

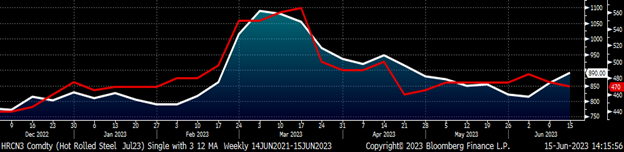

Taking this one step further was today’s surprise decline in July’s busheling future, while the July Midwest HRC future soared, resulting in a $400-425 metal spread in July through September. Which is going to give? Will busheling rally or will the rally in HRC be short lived?

July Midwest HRC $/st (white) & Busheling $/lt (red)

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.

By David Feldstein, Rock Trading Advisors

The solution to the dilemmas faced by Altos Hornos de México (AHMSA) is in the hands of the federal government, a spokesman for the Mexican steelmaker told a local news outlet.

AHMSA spokesman Francisco Orduña was responding to comments last Friday by Mexican President Andrés Manuel López Obrador regarding restructuring the company’s debt, according to an article in El Periódico La Voz on Friday, June 9.

AHMSA spokesman Francisco Orduña was responding to comments last Friday by Mexican President Andrés Manuel López Obrador regarding restructuring the company’s debt, according to an article in El Periódico La Voz on Friday, June 9.

He claimed in the article that Obrador “originated the problem four years ago.”

In 2019, the Mexican government under Obrador froze AHMSA’s bank accounts amid a corruption probe. The steelmaker claimed they were “improperly frozen,” according to a Reuters article at the time.

Orduña told La Voz that the new shareholders are already there and they “expect the government to fulfill its part.”

He said this includes plans to reactivate PEMEX gas, maintain electricity, form payment plans for accumulated debts with entities of the government, release blocked accounts, and “withdraw false accusations so that the new administration can access financing channels,” according to the article.

Recall that AHMSA announced an agreement in late-February to sell the majority of its shares to a group of foreign investors to recapitalize the company, with the shareholder later named as emerging markets credit specialist firm Argentem Creek Partners. However, some uncertainty remains around the sale.

An SMU email to Orduña was not immediately responded to by time of publication.

By Ethan Bernard, ethan@steelmarketupdate.com

Worthington Industries’ plan to split into two separate companies by early 2024 is full-steam ahead, and the man getting ready to helm the ship of the new Worthington Steel is Geoff Gilmore.

Gilmore joined Worthington in 1998, and has served as EVP and COO since August 2018. He will be the CEO of Worthington Steel, while the other company, “New Worthington,” name TBD, will be led by current Worthington Industries president and CEO Andy Rose.

Gilmore sat down with SMU senior analyst David Schollaert on Wednesday for a Community Chat to discuss the new company and what he’s seeing in the market.

First, Gilmore spoke of the honor of leading the new company, and touted the strengths of the management team coming with him.

First, Gilmore spoke of the honor of leading the new company, and touted the strengths of the management team coming with him.

“I’m just along for the ride and happy to be with this team,” he said. “I can’t wait to make it official and get on quarterly earnings calls.”

He said that Worthington Steel will be a “best-in-class, value-added steel processor with a blue-chip customer base in growing end markets.”

Gilmore cited electric vehicles, electric grid modernization, and the renewable energy markets in particular.

The company will have 31 manufacturing facilities, primarily in North America, but also in India and China.

He foresees Worthington Steel as a “market leader in automotive light-weighting solutions capitalizing on electrification, sustainability, and infrastructure spending.”

“Infrastructure is desperately needed in the US,” Gilmore said, noting the $1-trillion infrastructure bill signed in 2021 as an opportunity for growth.

Another area of focus is in the decarbonization of the auto industry, where Gilmore cited an S&P Global Mobility figure stating that 80% of vehicles sold globally in 2030 are expected to be either battery or hybrid.

He said the company’s Tempel Steel unit, acquired by Worthington in 2021, is poised to capitalize in both automotive and the energy market.

With electrification, “the automotive market is facing the largest fundamental change in decades,” Gilmore said.

Looking ahead for the next 12 months, he said the outlook for automotive is “steady as it goes,” adding that we are probably a couple of years away from auto sales at the 16.5-million level.

However, he said he is bullish on the market long term, noting that automotive accounts for 50% of Worthington’s business.

“Auto companies are not just betting on electric vehicles, they are doubling down,” Gilmore said.

If you’d like to view the entire presentation, click here.

Note the dates of our upcoming Community Chats:

June 20, 2023 – How to Generate Actionable Takeaways the SMU Steel Summit. Reigister here

July 12, 2023 – Timna Tanners, managing director, Wolfe Research. Register here

July 26, 2023 – Barry Zekelman, executive chairman and CEO, Zekelman Industries. Register here

By Ethan Bernard, ethan@steelmarketupdate.com

On Monday and Tuesday of this week, SMU polled steel buyers on a variety of subjects, including steel prices, demand levels, and import offers. Rather than summarizing the comments we received, we are sharing some of them in each buyer’s own words.

We want to hear your thoughts, too! Contact david@steelmarketupdate.com to be included in our questionnaires.

When and at what price level do you think steel prices will bottom, and why?

“$650 – I don’t foresee enough resistance in the market to stop it from eventually getting that low.”

“I suspect we will see the bottom in September or October. Foreign seems to be setting the future price, so I anticipate a base in the mid- to high-40s.”

“HRC will bottom around $700 in November/December.”

“I figure we won’t see any sort of leveling until post-summer. So, if we’re averaging $20/ton per week, it starts to get pretty scary.”

“I think prices bottom during July lead times, so in the next two weeks. Index prices make their way into the mid- to low-$800 range, while large buys get done $60-100 below that.”

“The market appears to be heading toward sub $800 HRC. Mid-July will be the turning point.”

Is demand improving, declining or stable, and why?

“Demand has been declining. Customers are aware that prices are dropping and are doing their best to ride it out.”

“Demand is softer. Customers are anticipating slower third and fourth quarters and are reducing buying to reflect this.”

“Declining slowly as backlogs are slipping and we are headed into summer slowdown.”

“Declining as OEMs are seeing demand drop.”

“Demand is declining but driven by buyers lowering their inventories; actual demand is fairly stable. Buyers are making it look way worse than it is.”

“Plate demand remains stable. Energy and infrastructure projects remain strong and continue to consume capacity.”

Is inventory moving faster or slower than this time last year – and why?

“Slower, demand has gone from high to stable.”

“Cannot keep inventory. Sales would be much better for those who actually have stock. No stock, no sales.”

“Inventory is moving at roughly the same pace as this time last year. We were in a similar market at that point.”

“Moving slower now as we slow down. It seems like it’s faster because folks are stocking less.”

“Slower, due to low manufacturing demand.”

“Inventory is moving the same, but it probably helps that service centers are trying to be lean.”

“Faster, we targeted an increase in sales this year and we are executing on that plan.”

With domestic prices still at a premium to imports, are you finding offshore product more attractive? Why or why not?

“Domestic pricing is quickly dropping to match imports, not much interest in import prices with long lead times right now.”

“Yes, imports are starting to look more attractive for specific types of business, but lead time is still a worry.”

“Absolutely. We are getting more and more calls from domestic mills trying to bat away imports. And we aren’t even that big of a consumer, so I assume the “big boys” are already seeing crazy deals out there.”

“No, the futures market is in range versus imports.”

“Yes, still a significant spread between offshore and domestic pricing.”

“No, domestic prices are falling too fast to make import buys right now.”

Do you have any recent import offers or transactions to report on either sheet or plate?

“Discrete plate offers that I have seen are not worth pursuing. Domestic prices will remain propped up.”

“$820 for August shipments.”

“$780-800 South Korea offer.”

“Galvanized offer from Turkey which is only $4.00/cwt less than domestic with a September arrival.”

“Imported plate is arriving 20% cheaper than the price of domestic plate.”

PSA: If you have not looked at our latest SMU Market Survey results, they are available here on our website to all Premium members. We refer to this as our ‘Steel Market Trends Report,’ and we publish updates every other Friday. We encourage readers to explore the full results, as we simply cannot write about all of the information within. After logging in at steelmarketupdate.com, visit the Analysis tab and look under the “Survey Results” section for “Latest Survey Results.” Historical survey results are also available under “Survey Results History.” We will conduct our next market survey next week – contact us if you would like to have your company represented.

By Becca Moczygemba, becca@steelmarketupdate.com

The US Department of Commerce’s International Trade Administration (ITA) is updating the antidumping duties on hot-rolled steel flats from South Korea.

In an administrative review of the one-year period ended Sept. 30, 2022, the ITA set preliminary dumping margins of 0% for Hyundai Steel, Posco, and 45 other Korean companies not selected for individual examination.

The all-others cash deposit rate remains set at 6.05%.

The ITA will issue the final results of the review by mid-October.

In the review of the prior one-year period ended Sept. 30, 2021, dumping rates were set at 0% for Posco and 0.84% for Hyundai and a handful of other companies.

Note that no duties are collected on de minimis dumping rates below 0.5%.

South Korea is typically one of the largest offshore suppliers of hot-rolled steel to the US. In the first four months of this year, just over 16,000 metric tons of Korean hot rolled was imported. Data from the US government shows 5,489 metric tons of import licenses for May and a June spike to 41,286 metric tons through the first 12 days of the month.

By Laura Miller, laura@steelmarketupdate.com

Domestic scrap prices continued to tumble this month on soft demand and strong inbound scrap flows, but the market could come into balance in July, sources said.

“After this more-than-expected drop in prices for June, the market next month should be sideways at worst,” one source said. He noted that the export market remains firm and the drop in shredded prices in June equalized price domestically and internationally.

“So, if export goes up, so will the US,” the source added.

Another source, describing June trading, said the region that was overpriced in May was out buying shred and prime grades at down $60 per gross ton and plate and structural at down $50 per gross ton.

“They were $20-40 above other regions last month, so this move is a price correction,” the second source said.

He said that mills that were paying less last month had less leverage to lower prices, “but other regions will be weaker too.”

A third source detailed the regional trades this month.

“Prices in the Ohio Valley all dropped to varying degrees, whereas prices in Cleveland and Pittsburgh are essentially the same for each grade,” he said.

Looking ahead, the third source was broadly in agreement that the market should level out in July.

“The expectation for July is the market should plateau as supply/demand come into balance,” the third source said.

With scrap prices settled, SMU’s June tags stood at:

• Busheling at $440-480 per gross ton, averaging $460, off $50 from the previous month.

• Shredded at $390-420 per gross ton, averaging $405, down $50 from the previous month.

• HMS at $290-320 per gross ton, averaging $305, dropping $30 from the previous month.

Editor’s note: SMU members can chart scrap prices as far back as 2007 using our interactive pricing tool.

By Ethan Bernard, ethan@steelmarketupdate.com

The forest fires raging in Canada caused rail interruptions for Champion Iron last week. With the fires now subsiding in the area, the company reports a resumption in rail services between its Bloom Lake mine and the port of Sept-Îles on the Gulf of St. Lawrence in Quebec.

Mining activities continued at Bloom Lake while rail services were suspended, and thus the operation now has a stockpile of iron ore concentrate, Champion said in a press release.

“Following the gradual ramp-up in capacity of the railway and limited additional availability of rolling stock to accommodate excess volumes beyond Bloom Lake’s production capacity,” the Montreal-based company says to expect delays in sales of concentrate from the operation.

Champion’s subsidiary Quebec Iron Ore Inc. operates the open-pit Bloom Lake Mining Complex in Quebec. Its two concentrators, ran primarily by hydroelectric power, have a combined annual capacity of 15 million tons of iron ore concentrate.

By Laura Miller, laura@steelmarketupdate.com

U.S. Steel and Wheeling-Nippon Steel have joined other domestic mills in reducing coating extras.

Wheeling-Nippon said the new, lower extras would be effective with new orders quoted for the week ending July 22.

The new extras apply to aluminized, galvanized, and galvanneal, the company said in a letter to customers dated Wednesday, June 14.

The new extras apply to aluminized, galvanized, and galvanneal, the company said in a letter to customers dated Wednesday, June 14.

One example of the new extras: Wheeling-Nippon had charged $4.90 per cwt for a 0.0849-.0600 G90. The same item is now $4.30 per cwt – a roughly 12% reduction.

U.S. Steel’s new coating extras are effective July 30, according to an updated price book. The company had charged $4.85 per cwt for an 0.085-.060 G90. The same item, under the new schedule, is $3.90 – a nearly 20% drop.

At least two other domestic mills – Steel Dynamics Inc. (SDI) and NLMK USA – have also announced lower coating extras.

We will update our website to reflect the revised extras. Announcements of lower coating extras come after zinc prices dropped to their lowest point since July 2020.

By Michael Cowden, michael@steelmarketupdate.com

U.S. Steel aims to increase base prices on spot orders of flat-rolled steel by at least $50 per ton ($2.50 per cwt.)

The move is effective immediately and applies to “all open quotations and/or negotiations where an agreement is yet to be concluded,” the Pittsburgh-based steelmaker said in a letter to it sales executives on Wednesday, June 14.

The increase applies not only to material from U.S. Steel but also to product from its USS-UPI subsidiary in California and its Big River Steel subsidiary in Arkansas.

U.S. Steel’s sheet price hike is the first since Cleveland-Cliffs announced one of $100 per ton – and a target price of $1,300 per ton for hot-rolled coil – on April 3.

U.S. Steel did not list a target price for coil in this increase.

SMU’s hot-rolled coil price stands at $930 per ton, down nearly 20% from a 2023 peak of $1,160 per ton mid-April and marking the lowest point for HRC prices since late February.

Initial reaction to the increase was mixed.

Some market participants questioned whether the move would reverse a trend of falling prices and shorter lead times that has been in place for most of the second quarter. They noted that U.S. Steel was primarily focused on contract-driven automotive business and might have comparatively little exposure or influence over the spot market. Another theory was that the increase might be timed to entice buyers who have been on the sidelines to jump back into the market to restock.

It was not immediately clear whether other mills would follow U.S. Steel’s attempted leading move.

SMU has updated its price-increase calendar to reflect U.S. Steel’s announcement. Please find it here.

By Michael Cowden, michael@steelmarketupdate.com

Nucor said Wednesday the location of its second utility structures production facility will be in Crawfordsville, Ind.

The Charlotte, N.C.-based steelmaker said the new operation it’s building will be located next to the Nucor Steel Crawfordsville steel mill, and is expected to create 200 full-time jobs.

“With this second utility structure production facility, we are expanding our Towers and Structures business and positioning the company to meet the growing demand for utility infrastructure from renewable energy projects, EV (electric vehicle) charging network expansion, and grid hardening,” Leon Topalian, chair, president, and CEO of Nucor, said in a press release.

In 2022, Nucor formed its Nucor Towers & Structures business unit when it bought Summit Utility Structures LLC, a producer of metal poles and other steel structures for utility infrastructure.

Earlier this year, Nucor announced its plans to build the first facility in Decatur, Ala. The company previously said two new utility facilities would have a combined investment of $270 million.

The steelmaker noted that both the Indiana and Alabama facilities “will be highly automated, utilizing efficient straight-line production, and will also include advanced hot-dip galvanizing operations.”

Ethan Bernard, ethan@steelmarketupdate.com

Ohio-based Miami Valley Steel Service Inc. (MVSS) has named Nick Straka as its new president and CEO, effective July 1.

The steel service center said Straka joined MVSS in 2005 in sales, and currently serves as the COO. He will be replacing Lou Moran, who will be stepping down as president and CEO after 14 years. MVSS added that Moran, who has dedicated 33 years to the company, will become executive chairman of the MVSS board.

“At the core of our business lies a culture of excellence that extends to our employees and business partners. Throughout MVSS’s history, we have been fortunate to have exceptional leaders like Lou who have solidified this culture,” Straka said in a press release on Wednesday. “I am both humbled and excited to have the privilege of upholding these high standards for our teammates, customers, vendors, and community.”

By Becca Moczygemba, becca@steelmarketupdate.com

Sometimes it seems the whole world is downstream of the steel industry. Now, that may be a side effect of spending my days immersed in lead times, steel buyers sentiment, and hot-rolled coil futures. That would be a fair assessment. However, looking into the testimonies from the Congressional Steel Caucus’ recent hearing on June 7 displays some of the complicated realities of 2023.

What struck me about the hearing was how the steel industry is handling the post-pandemic phase of globalization.

For example, Roy Houseman, legislative director of the United Steelworkers (USW) union, spoke about the Caucus’ recent letter on “the surge of steel imports from Mexico.”

“As you outlined in a recent letter, it looks like the Mexican steel industry is using its duty-free status under the United States-Mexico-Canada Agreement (USMCA) to permit melted and poured steel products from countries like Brazil, South Korea, and Russia to enter the US through Mexico,” Houseman claimed.

Beyond the issue itself, what’s interesting to me is the interplay between union, industry, the branches of the federal government, trade agreements, and foreign governments. What seems at first glance a regional issue is essentially global in character. Globalization seems now less a good in itself as it was touted to be in the 1990s, but a complex web of negotiations, a necessity that needs to be sorted out.

Nowhere does this seem to be more evident than in decarbonization. Almost everyone is in agreement that it’s a good thing. How to get there is another story, and there’s not only one route.

For example, Cleveland-Cliffs’ chairman, president, and CEO Lourenco Goncalves touted a recent test of hydrogen in the company’s Middletown Works blast furnace in Ohio, while Nucor’s chair, president, and CEO Leon Topalian spoke of the benefits of electric-arc furnace (EAF) steelmaking.

In his testimony, Richard Fruehauf, SVP and chief strategy and sustainability officer at US Steel spoke of the Caucus’ recent focus as the US and European Union discuss a potential global arrangement on steel overcapacity and decarbonization. An agreement is hoped for by October. The US is at odds with the EU’s proposed carbon border adjustment mechanism (CBAM) that could see a carbon tariff placed on US exports to the union.

Here again is a meeting point for globalization that also takes in the threads of China and the developing world. Hammering out an agreement suitable to global players is not an abstract good, but a vital reality that needs the participation of everyone from the workers in a factory to the heads of state.

All of the witnesses’ testimonies can be found here.

SMU Steel Summit

The premier US steel conference is less than three months away. The agenda is packed full of industry experts and key players, and registrations are climbing fast. We had over 1,300 in attendance last year, and we’re on pace to easily exceed that total. So, you may want to consider booking your hotel soon for the Steel Summit, if you haven’t already. Discounted room blocks are going fast, and non-discounted prices are a lot higher than they’ve been in past years.

You can learn more about the agenda and networking opportunities, and to register, click here.

You can register here for the free live webinar.

By Ethan Bernard, ethan@steelmarketupdate.com

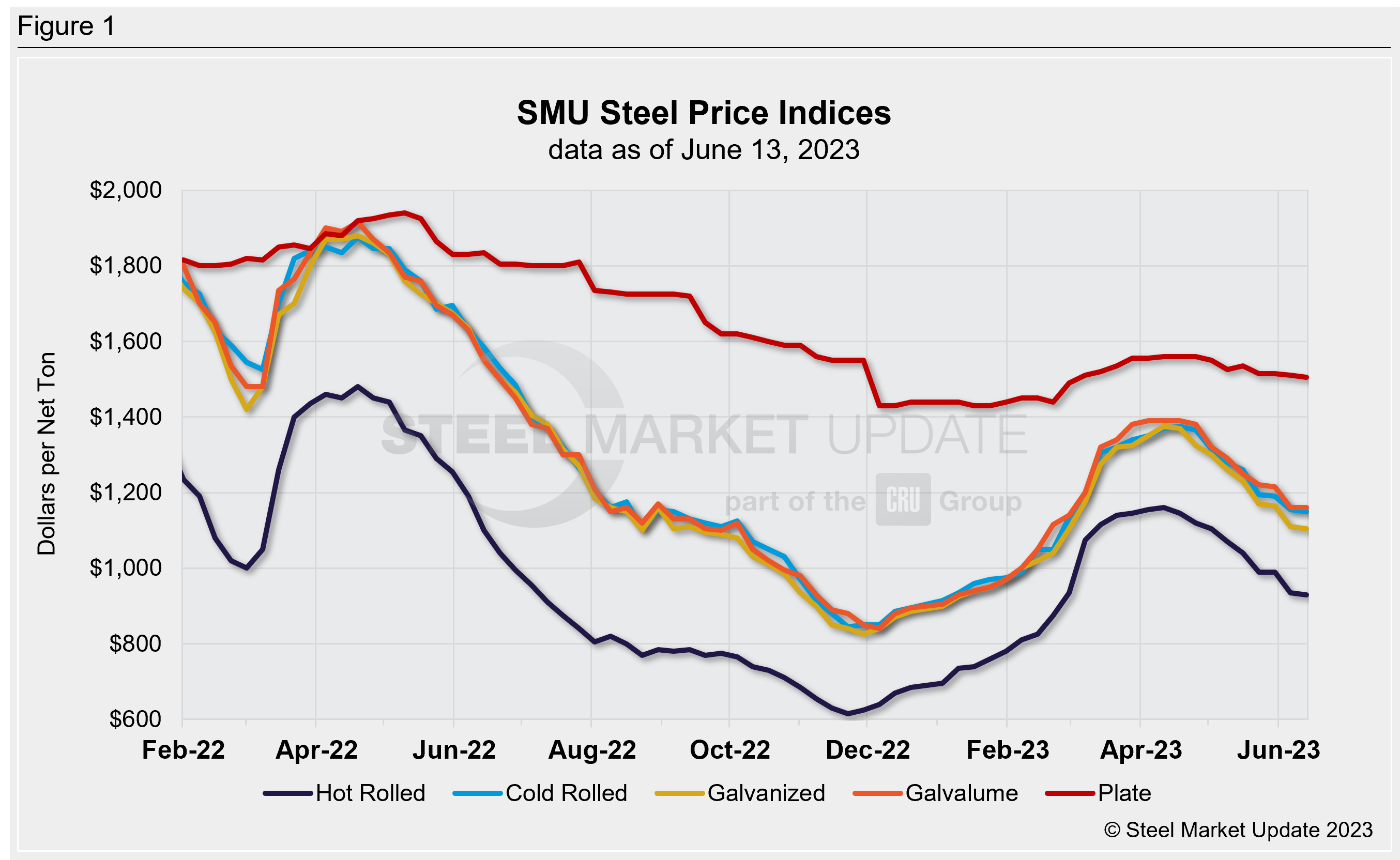

Sheet prices fell at a more modest pace this week after a sharp decline last week, as business seemed somewhat curbed.

After Memorial Day prices fell, leading to the sharpest price drop since June 21, 2022. Now, the slide seems to have temporarily cooled, though sources indicated it was almost exclusively due to a lack of activity.

SMU’s hot-rolled coil price now stands at $930 per ton ($46.50 per cwt), down $5 per ton from a week ago. While chatter existed of even lower prices, there was little in the way of confirmation, as unsolicited offers seemed to gain traction.

Value-added products also posted widespread declines, though again at much smaller rates than the double-digit cuts the week prior. Cold-rolled was down $5 per ton, as was galvanized and Galvalume. We’ve seen two mills lower coating extras as zinc prices erode, and sources anticipate other mills will follow.

Though sheet prices didn’t follow last week’s sharp fall, sources agree that further tag erosion is likely as domestic product remains at a premium to offshore sheet. Also, discounting should intensify as new capacity continues to ramp up.

Plate prices were only down marginally, at $1,505 per ton, but talk surrounding aggressive discounting from published prices continued.

Our sheet price momentum indicator remains at lower. Our plate price momentum indicator continues to point sideways.

Hot-Rolled Coil: The SMU price range is $890–970 per net ton ($44.50–48.50 per cwt), with an average of $930 per ton ($46.50 per cwt) FOB mill, east of the Rockies. The bottom end of our range was unchanged vs. one week ago, while the top end was down $10 per ton week on week (WoW). Our overall average down $5 per ton WoW. Our price momentum indicator for hot-rolled coil points downward, meaning we expect the market will be down over the next 30 days.

Hot-Rolled Lead Times: 3–7 weeks

Cold-Rolled Coil: The SMU price range is $1,100–1,200 per net ton ($55.00–60.00 per cwt), with an average of $1,150 per ton ($57.50per cwt) FOB mill, east of the Rockies. The lower end of our range was sideways WoW, while the top end was down $10 per ton compared to a week ago. Our overall average is down $5 per ton WoW. Our price momentum indicator on cold-rolled coil points downward, meaning we expect the market will be down over the next 30 days.

Cold-Rolled Lead Times: 5–9 weeks

Galvanized Coil: The SMU price range is $1,040–1,170 per net ton ($52.00–58.50 per cwt), with an average of $1,105 per ton ($55.25 per cwt) FOB mill, east of the Rockies. The lower end of our range was unchanged vs. last week, while the top end of our range was down $10 per ton vs. one week ago. Our overall average is down $5 per ton vs. the prior week. Our price momentum indicator on galvanized steel points downward, meaning we expect the market will be down over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $1,137–1,267 per ton with an average of $1,202 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 3–10 weeks

Galvalume Coil: The SMU price range is $1,136–1,185 per net ton ($56.75-59.25 per cwt), with an average of $1,160 per ton ($58.00 per cwt) FOB mill, east of the Rockies. Both the lower end of the range and the top end of the range were unchanged vs. last week. Our overall average sideways as a result when compared to one week ago. Our price momentum indicator on Galvalume steel now points downward, meaning we expect the market will be down over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,429–1,479 per ton with an average of $1,454 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6–8 weeks

Plate: The SMU price range is $1,450–1,560 per net ton ($72.50–78.00 per cwt), with an average of $1,505 per ton ($75.25 per cwt) FOB mill. The lower end of our range was unchanged compared to the prior week, while the top end of our range was down $10 per ton WoW. Our overall average was down $5 per ton vs. the prior week. Our price momentum indicator on steel plate moved to neutral, meaning we are unsure of what direction prices will go over the next 30 days.

Plate Lead Times: 4–9 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

By David Schollaert, david@steelmarketupdate.com

U.S. Steel published its 2022 Environmental, Social and Governance (ESG) Report in which the Pittsburgh-based steel maker said it has dedicated itself to creating sustainable steel and contributing to a greener economy. The report, titled “Essential for Our Future,” reaffirms how essential steel is to creating green technology such as wind turbines solar fields, and electric vehicles. It highlights steel’s ability to be infinitely recycled without loss of quality, providing a significant contribution to lowering greenhouse gas emissions. “Every single employee is playing a role in creating a more sustainable future,” commented David B. Burritt, U.S. Steel’s president and CEO. “Steel’s importance to our society is undeniable, both in the past and into the future as we collectively tackle climate change. It’s of particular significance that we were the first American steel company to set a goal of achieving net-zero greenhouse gas emissions by 2050.” USS said in a press release that it has surpassed its $300 million spending goal on supply chain sustainability programs by nearly 130%. The company is investing in a non-grain oriented (NGO) electrical steel line to meet the increasing demand for EVs and continues to diversify its supplier base. You can find the full report here.

A poll commissioned by the Alliance for American Manufacturing (AAM) shows the vast majority of American voters support strong trade remedies and bringing manufacturing back to the US.

The poll found nearly nine-in-10 voters (87%) agree the federal government should crack down on unfair trade, and four-in-five voters (82%) think the federal government should offer manufacturers incentives to relocate their factories to the US, AAM said in a press release on Tuesday.

The poll found nearly nine-in-10 voters (87%) agree the federal government should crack down on unfair trade, and four-in-five voters (82%) think the federal government should offer manufacturers incentives to relocate their factories to the US, AAM said in a press release on Tuesday.

The group added that the poll, conducted by Morning Consult, found 78% of voters say the federal government should be required to buy American with its own purchases.

However, AAM noted that of those polled only approximately one-third of voters have seen, read or heard about new factories coming to their community (30%) and to the US (36%).

AAM president Scott Paul commented that US voters have made it clear the federal government must do more to bring valuable domestic manufacturing jobs.

“Over the past two years, the US has taken serious steps towards bolstering American competitiveness through investment in domestic manufacturing, but the impacts haven’t yet hit home with communities nationwide,” he said in the release.

Washington D.C.-based AAM is a non-profit, non-partisan partnership formed in 2007 by some of America’s leading manufacturers and the United Steelworkers with a mission to strengthen American manufacturing and create new private-sector jobs through smart public policies.

By Ethan Bernard, ethan@steelmarketupdate.com

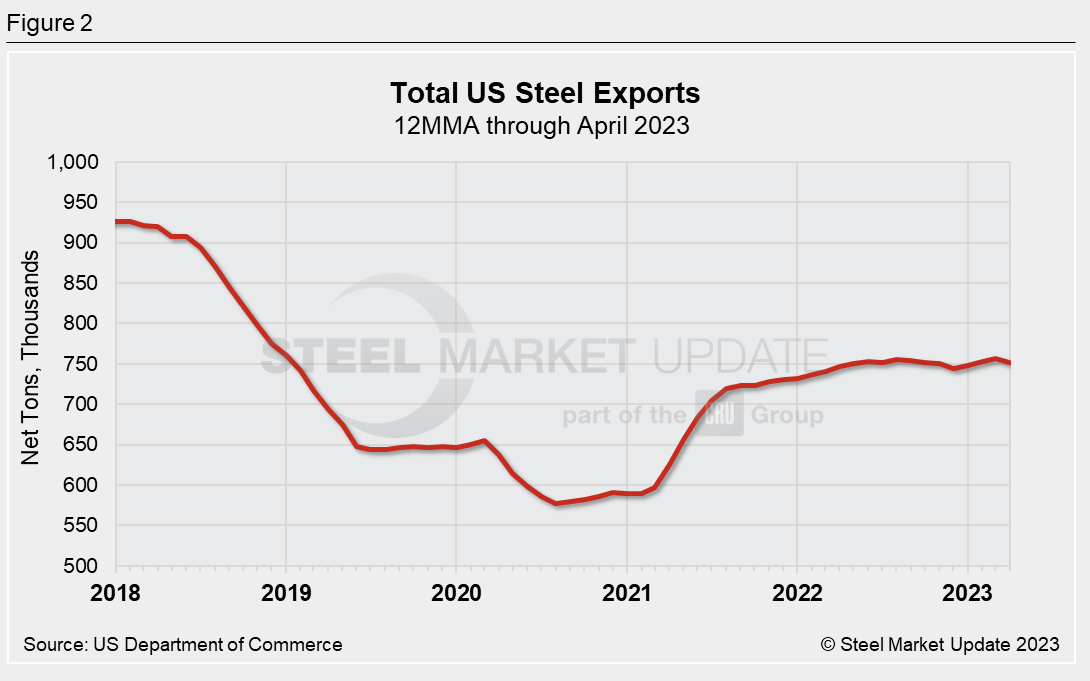

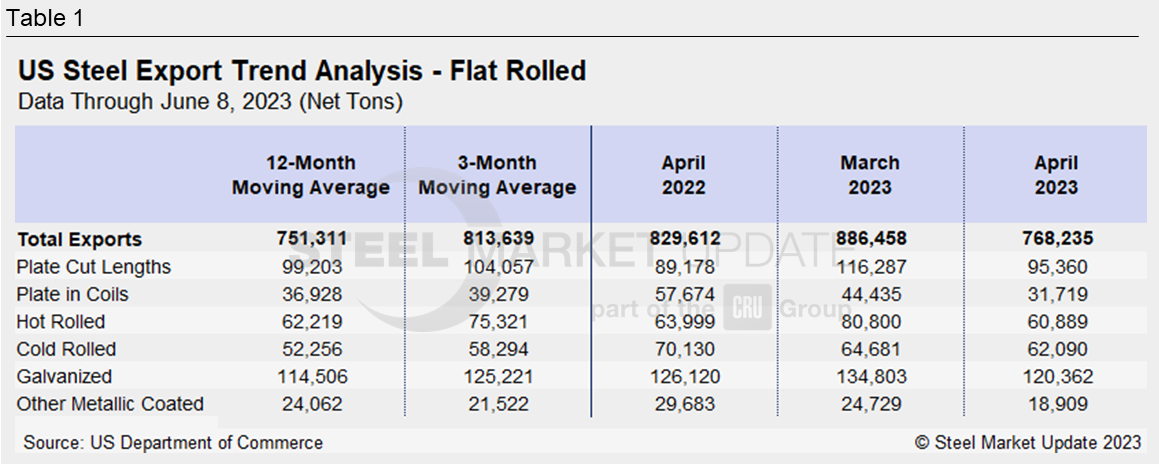

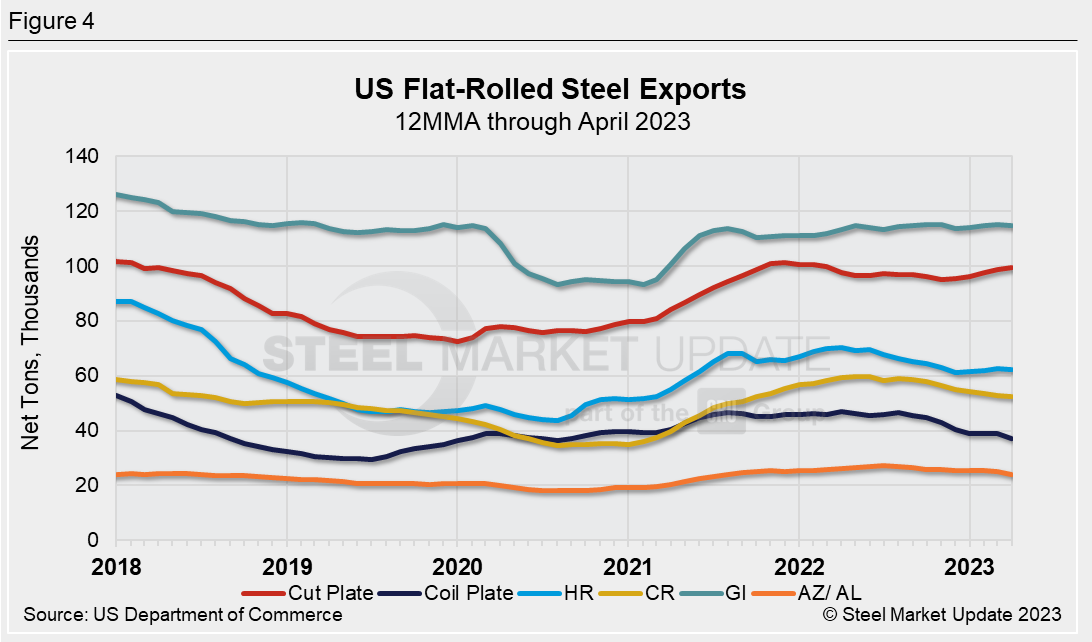

After hitting an almost five-year high in March, US steel exports fell back during the month of April.

Exports totaled 768,235 net tons in April, according to the latest figures available from the US Department of Commerce. This was a 13% month-on-month (MoM) and a 7% year-on-year (YoY) decline. Note that March exports of 886,458 tons were at their highest monthly level since June 2018 (Figure 1).

Shipments to Canada and Mexico typically account for over 90% of monthly exports. April shipments to the USMCA trading partners were at a three-month low.

Looking at exports on a 12-month moving average (12MMA) basis reveals that exports have been fairly steady since mid-2021, inching up from 704,196 tons in July 2021 to 751,311 tons in April (Figure 2)

Exports of major flat-rolled steel products (Table 1) all showed MoM and YoY declines, save for cut-to-length plate, which was down MoM but showed YoY growth of 7%.

Galvanized sheet and strip is the most-exported flat-rolled product. At 120,362 tons in April, exports were down 11% from the three-month moving average (3MMA) but up 5% from the 12MMA.

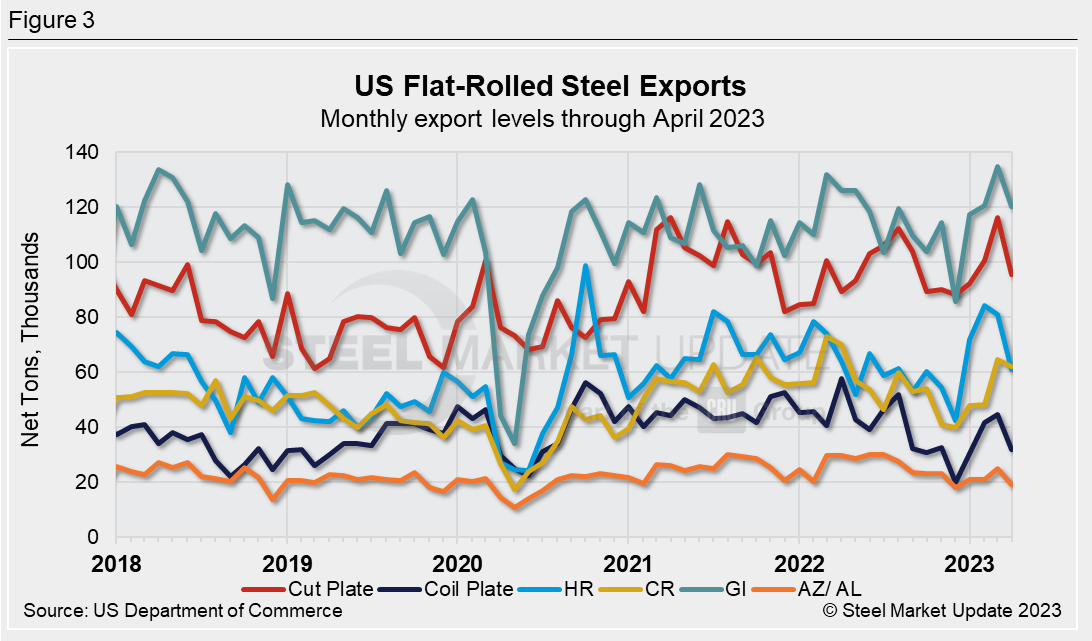

While flat-rolled exports can be erratic month-to-month (Figure 3), looking at their 12MMAs shows most sheet products creeping higher from their recent lows in mid-2020 (Figure 4).

The recent lows for the 12MMA of plate exports were in mid-2019. While cut plate exports have been recovering nicely, exports of coiled plate have been inching downward.

Readers can further investigate historical export data in total and by product using the interactive graphic tool available on our website.

By Laura Miller, laura@steelmarketupdate.com

Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact Lindsey Fox at lindsey@steelmarketupdate.com.

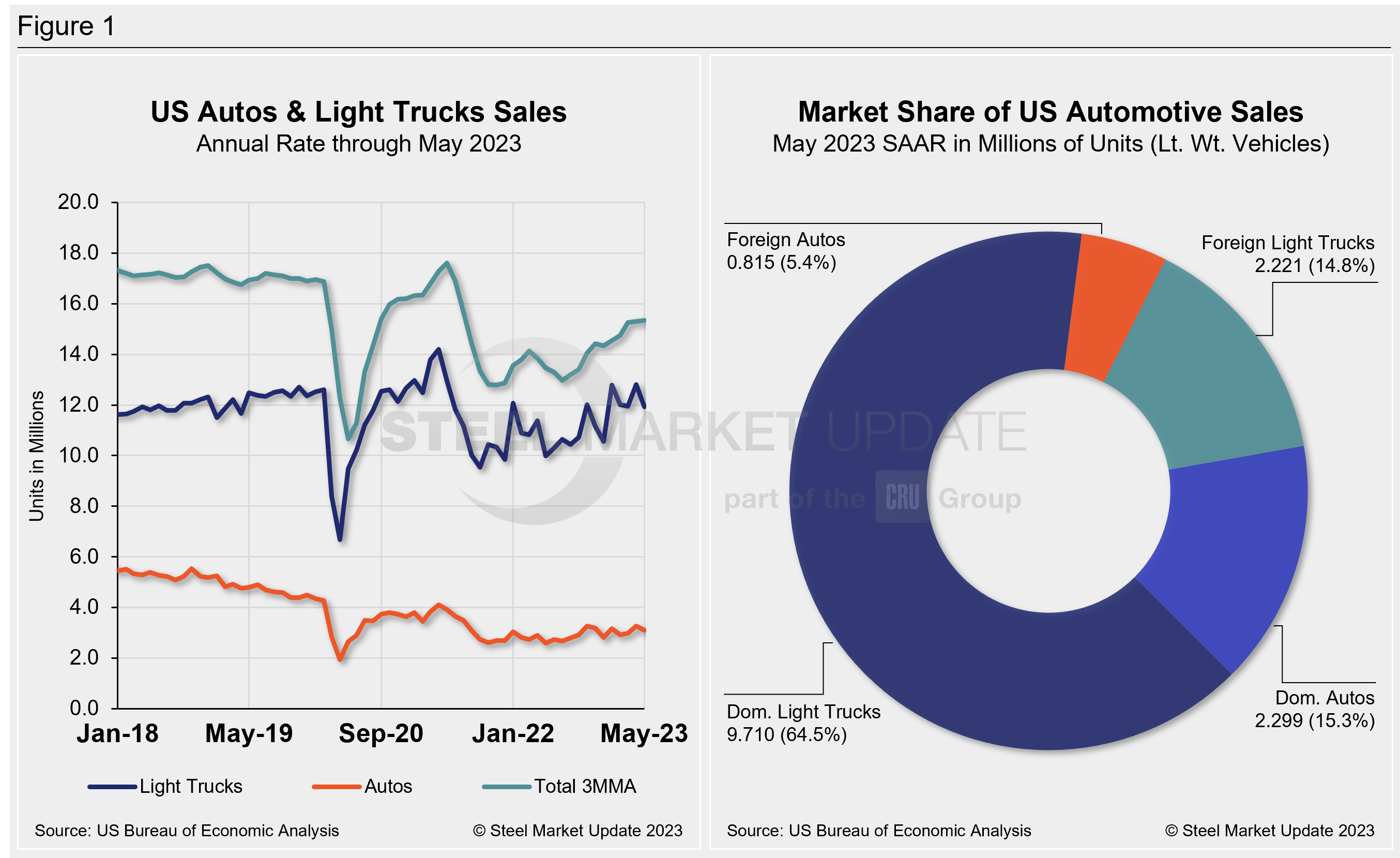

US light-vehicle (LV) sales rose to an unadjusted 1.36 million units in May, up 22.9% vs. year-ago levels, the US Bureau of Economic Analysis (BEA) reported. Despite the year-on-year (YoY) boost, domestic LV sales fell 6.5% month-on-month (MoM).

On an annualized basis, LV sales were 15.1 million units in May, down from 15.9 million units the month prior, and below the consensus forecast which called for a more modest decline to 15.3 million units.

Auto sales continue to be impacted by high-priced inventory. Although the supply of affordable vehicles is growing gradually, the market is still heavily skewed toward higher-end models. This continues to pose a major headwind for most consumers, especially given the current swelled interest rate environment. And retail incentives, though being pressured higher, up 64% YoY in May, are still just about half of what they were in May 2019 – before the global pandemic and semiconductor shortage cut auto assemblies.

Despite that, the average daily selling rate was 54,481 – calculated over 25 days – up from May 2022’s 46,169 daily rate. And passenger vehicle sales increased YoY while sales of light-trucks ticked up by 23.1% over the same period. Light-trucks accounted for 79% of last month’s sales, roughly one percentage point below its share of sales in May 2022.

Below in Figure 1 is the long-term picture of sales of autos and lightweight trucks in the US from 2013 through May 2023. Additionally, it includes the market share sales breakdown of last month’s 15.1 million vehicles at a seasonally adjusted annual rate.

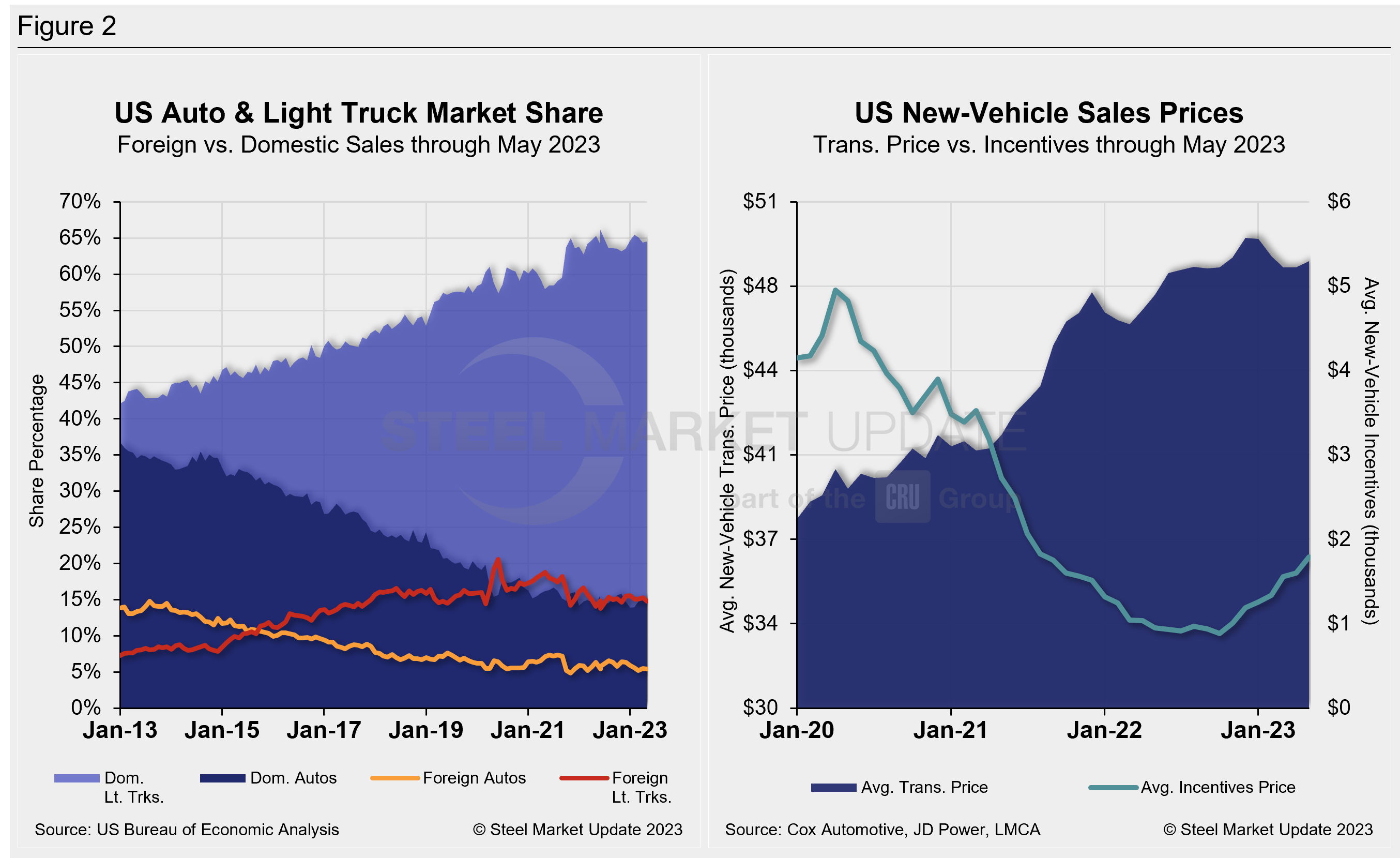

The new-vehicle average transaction price (ATP) was $48,528 in May, up 0.5% from April and up for the first time in five months. Last month’s ATP was also 2.9% (+$1,380) above the year-ago period, according to Cox Automotive data.

Incentives increased again for the seventh straight month. Last month’s incentives were $1,788, up from $1,599 in April, and the highest total since August 2021. With the MoM increase, incentives remained above the $1,000 mark for the seventh time in 10 months and roughly 4% of the average transaction price. Incentives are up 88.2%, or $838 YoY.

In May, the annualized selling rate of light trucks was 11.931 million units, down 6.9% vs. the prior month but still nearly 20% better YoY. Auto annualized selling rates saw similar dynamics, down 5% but up 19.9%, respectively, in the same comparisons.

Figure 2 details the US auto and light-truck market share since 2013 and the divergence between average transaction prices and incentives in the US market since 2020.

Editor’s Note: This report is based on data from the US Bureau of Economic Analysis (BEA), LMC Automotive, JD Power, and Cox Automotive for automotive sales in the US, Canada, and Mexico. Specifically, the report describes light vehicle sales in the US.

By David Schollaert, david@steelmarketupdate.com

Geoff Gilmore, future president and CEO of Worthington Steel, will be the featured speaker on the next SMU Community Chat on Wednesday, June 14, at 11 a.m. ET.

The live webinar is free to attend. A recording will be available to SMU members. You can register here.

We’ll talk about current steel market dynamics, the outlook for the second half, and what might be in store for 2024. We’ll also discuss the biggest challenges and opportunities ahead for Worthington Steel.

And we’ll take your questions too! As always, we’ll keep it to about 45 minutes. You can drop in, learn something – and then get on with your day.

Recall that Gilmore was named executive vice president and chief operating officer of Worthington Industries in August 2018. Worthington in September 2022 announced plans to separate its steel processing business to create a new, standalone public company by early 2024. Gilmore will lead that new company, which will be known as “Worthington Steel.” The consumer products, building products, and sustainable energy solutions segments will be rolled into “New Worthington.”

PS – Check out our Community Chat page, if you’d like to see recordings of past webinars, including our May chat with Flack Global Metals and Flack Metal Bank founder and CEO Jeremy Flack.

By David Schollaert, david@steelmarketupdate.com

General Motors said Monday it plans to invest $632 million in its Fort Wayne, Ind., assembly operation for future truck production.

The Detroit-based automaker said the investment will prepare the plant for production of “the next-generation internal combustion engine (ICE) full-size light-duty trucks,” adding that product details and timing related to future trucks are not being released at this time.

“This investment reflects our commitment to our loyal truck customers and the hard work of the dedicated Fort Wayne team,” Gerald Johnson, EVP of global manufacturing and sustainability, said in a statement.

“It also highlights the company’s commitment to continue providing customers a strong portfolio of ICE vehicles for years to come,” he said.

Johnson noted that GM’s manufacturing operations include more than 50 assembly, stamping, propulsion and component plants and parts distribution centers nationwide.

The Fort Wayne operation builds the Chevrolet Silverado 1500 and GMC Sierra 1500. GM said the investment will support new conveyors, tooling, and equipment in the plant’s body and general assembly areas.

Hourly employees are represented by United Auto Workers (UAW) union Local 2209, according to GM.

“When business is booming as it has been for the past decade — due to the hard work of UAW members — the company should continue to invest in its workforce,” said Mike Booth, UAW VP, GM department. “It is good to see that GM recognizes the hard work you, the UAW membership, contribute to the success of this company.”

This investment comes on the heels of other investments the automakers announced earlier this month.

By Ethan Bernard, ethan@steelmarketupdate.com

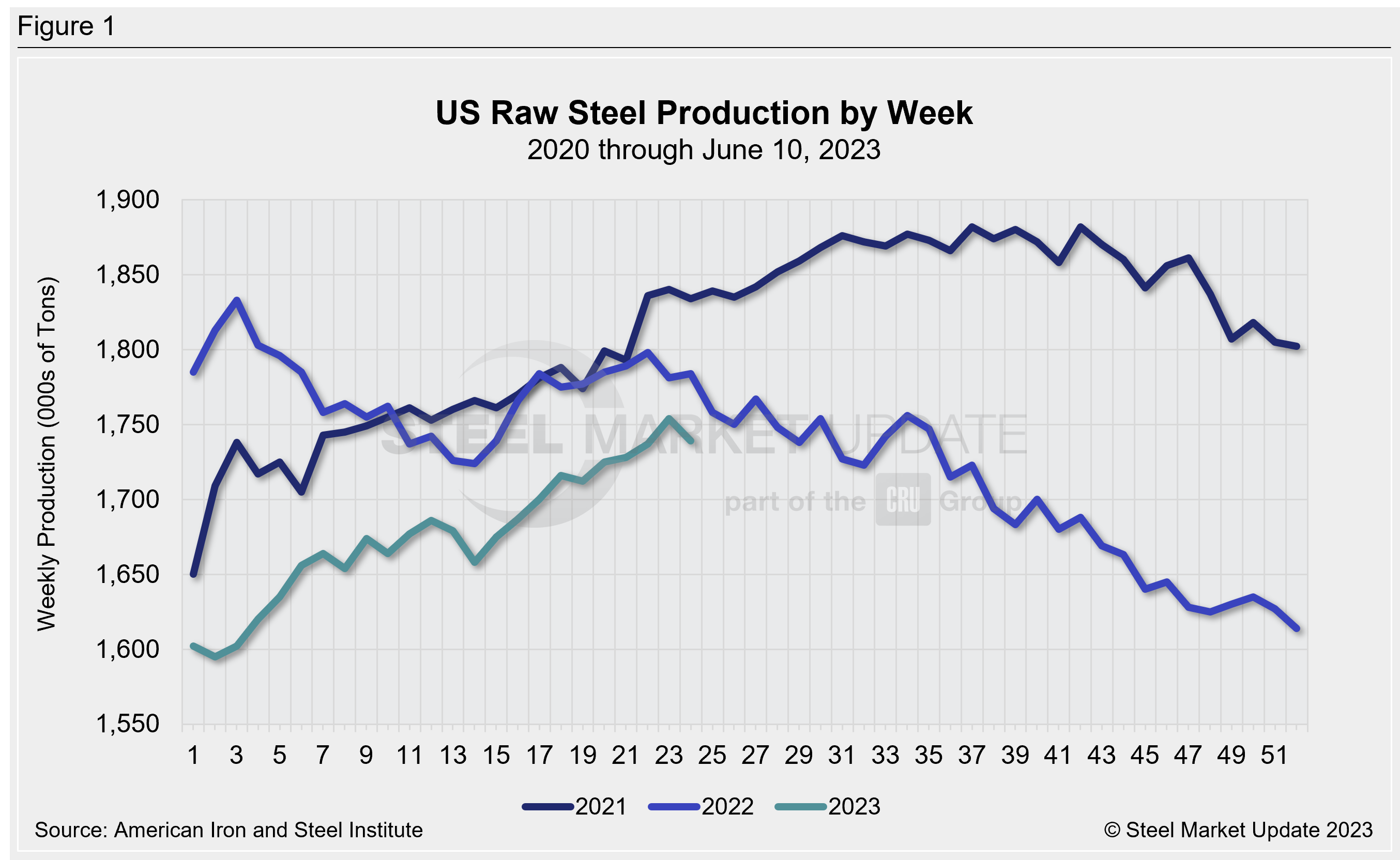

Raw steel production by US mills slipped last week, declining for the first time in five weeks, according to data released by the American Iron and Steel Institute (AISI) on Monday, June 12.

Domestic production stood at 1,739,000 net tons in the week ended June 10, down 0.9% vs. 1,754,000 tons the previous week. Despite the marginal decrease, output was still up by 0.1% from 1,738,000 tons in the same week last year.

The mill capability utilization rate was 77.3% last week, down from 78% a week earlier. Utilization was still off from 78% in the same week last year.

AISI said that adjusted year-to-date production through June 10 was 38,985,000 tons at a capability utilization rate of 75.6%. This is down 3.2% from the year-ago period when 40,268,000 tons were produced with an overall capability utilization rate of 80.3%.

Production by region for the week ending June 10 is below. (Note: week-over-week change is in parentheses.)

- Northeast – 137,000 tons (down 3,000 tons)

- Great Lakes – 560,000 tons (down 11,000 tons)

- Midwest – 211,000 tons (down 2,000 tons)

- South – 766,000 tons (down 2,000 tons)

- West – 65,000 tons (up 3,000 tons)

Note: The raw steel production tonnage provided in this report is estimated. The figures are compiled from weekly production tonnages provided by approximately 50% of the domestic production capacity combined with the most recent monthly production data for the remainder. Therefore, this report should be used primarily to assess production trends. The AISI production report “AIS 7,” published monthly and available by subscription, provides a more detailed summary of steel production based on data supplied by companies representing 75% of US production capacity.

By David Schollaert, david@steelmarketupdate.com

TT Iron Steel Co. Ltd. (TTIS) has signed an agreement to acquire the ArcelorMittal Point Lisas iron and steel plant in Trinidad and Tobago.

Completion of the transaction is subject to approval by Trinidad and Tobago’s government, TTIS said in a release on June 7. The company said initial refurbishment and restart of the plant is expected to cost $150-200 million over the next two years, with further investment required thereafter.

Further details of the transaction were not provided.

The plant is one of the largest steel mills in the Americas that utilizes natural-gas-based, direct-reduced Iron (DRI) technology with electric-arc furnaces for steelmaking, according to TTIS.

ArcelorMittal shuttered the plant in 2016.

“We believe there is great potential for the plant to return to the forefront of global steelmaking technology and performance,” TTIS founder, president, and CEO Gus Hiller said in the release

The plant has historically used natural gas, but TTIS intends to transition to green hydrogen in the next few years as it becomes commercially available. This will reduce the plant’s carbon intensity to 0.4 metric tons of CO2 per metric ton of steel made.

After the restart, the facility “will be the largest recycling operation in the Caribbean consuming scrap and waste tires generated in Trinidad and Tobago to make steel products,” TTIS said on its website.

TTIS commented that more than 1,000 jobs will be created during the refurbishment and start-up phase and, when fully operational, it will create long term employment for 500 skilled workers.

By Ethan Bernard, ethan@steelmarketupdate.com

Rio Tinto said it has signed a memorandum of understanding (MoU) with Chinese steelmaker Baowu to explore projects in China and Australia to help decarbonize the steel value chain.

The global metals and mining company commented that the move follows the recently announced $2-billion Western Range joint venture in the Pilbara region of western Australia involving both Rio Tinto and Baowu.

“Rio Tinto and China Baowu are united in a commitment to accelerating the delivery of low-carbon solutions for the entire steel value chain,” Rio Tinto chief commercial officer Alf Barrios said in a statement.

He noted that the MoU aims to address the challenge of “developing a low-carbon pathway for low-to-medium grade iron ores, which account for the vast majority of global iron ore supply.”

By Ethan Bernard, ethan@steelmarketupdate.com

This weekend I was at my daughters’ swim meet. It’s a recreational summer league, so not all the kids are very competitive, but they all seem to have a great time cheering each other on.

The sportsmanship was unrivaled. All the kids shook each other’s hands after each heat, and nobody exited the water until the last swimmer touched the wall, even if the last swimmer was 30 seconds behind.

Being present at such a thrilling sporting event got me thinking about community. As I looked around, I noticed many of the parents were wearing their child’s team’s shirt. Most people had some type of identifier that told you who they were rooting for. But how do we in the steel industry do the same?

Every single person I have interviewed for our SMU Spotlight series has said the thing they love the most about the steel industry are the people. Our community. Just about every week we reach out to many of you to catch up on pricing, lead times, or whatever else is going on in the market. But there’s more to it than the market talk. I’ve had the opportunity to hear about baseball tournaments, high school graduations, and moving into universities. We’ve met up with our readers who live close to us, or people who contact us when they’re in town, and we get together.

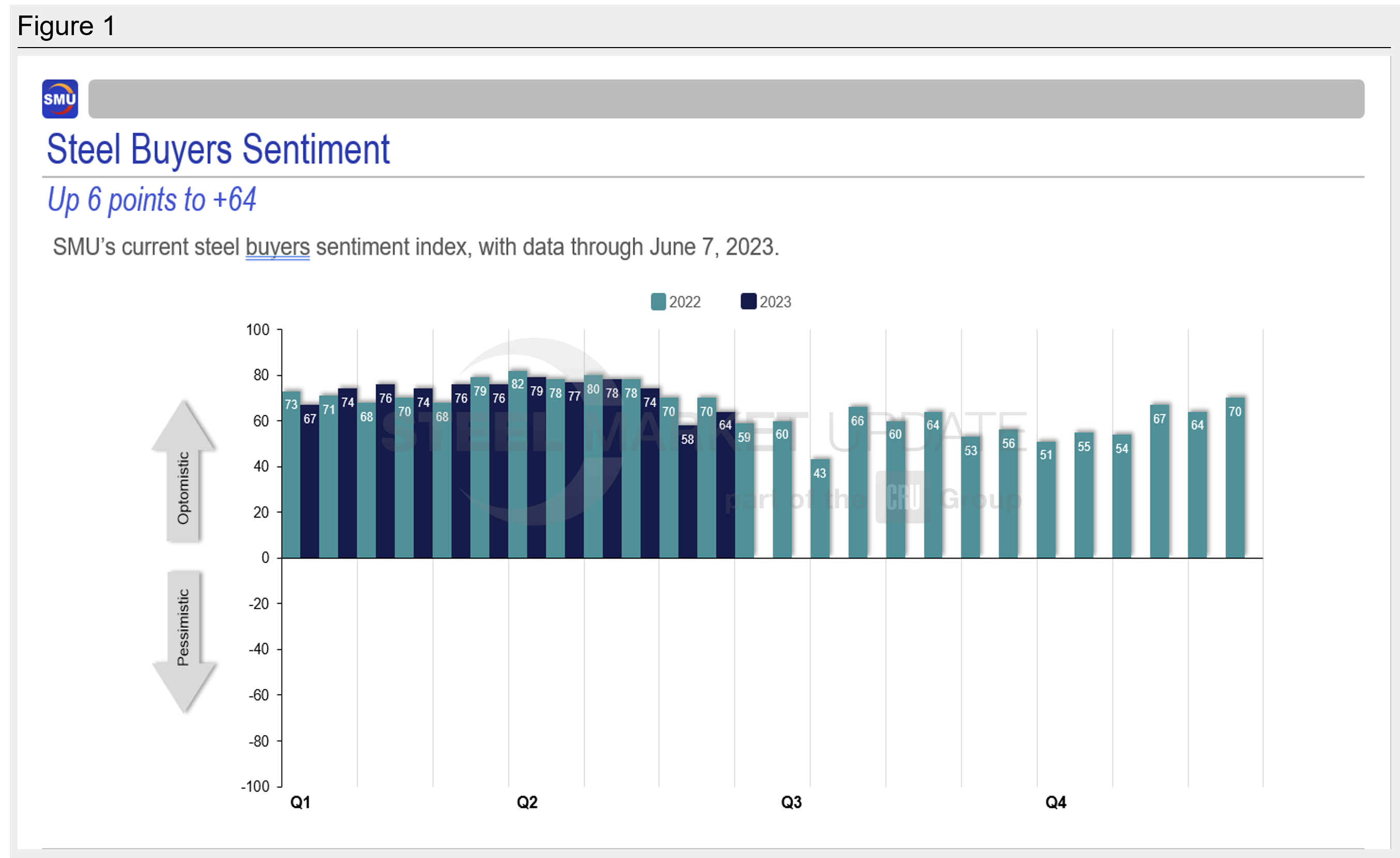

I wish I had a crystal ball, because inevitably I get asked what the market is going to do. It’s been a roller coaster to say the least, but this week our Current Steel Buyers Sentiment Index is up vs. the previous market check. Though it’s not as high as it was at this time last year, buyers seem cautiously optimistic.

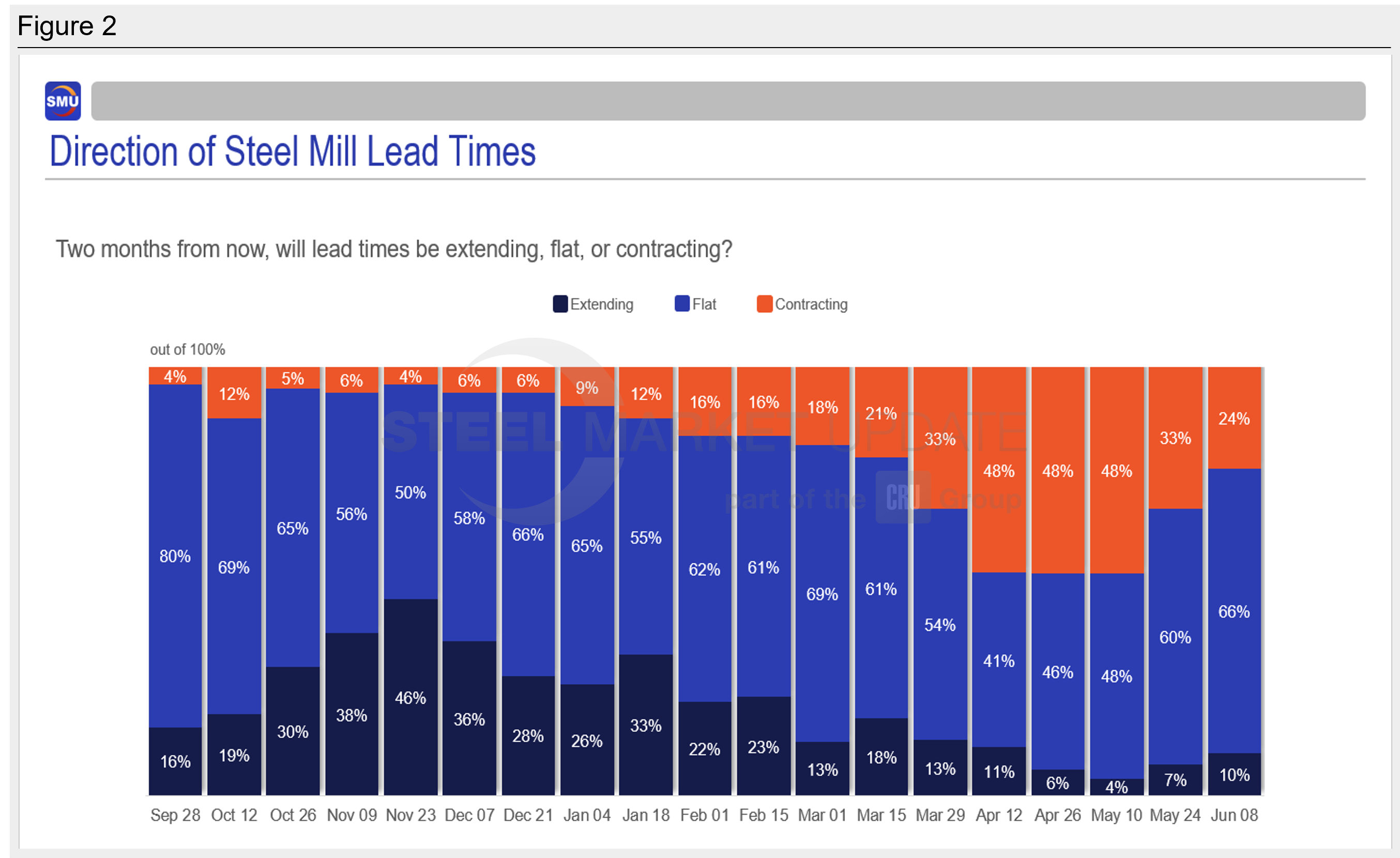

Most people who responded to our survey this week believe that lead times will be flat two months from now. I guess that’s something we can discuss at Steel Summit, which is also about two months from now.

So yes, we bring you pricing, lead times, market sentiment, and the like, but we’re more than that. Last year was my first year at Steel Summit and I finally understood what everyone had been saying. I like to think of it as a block party for the community that just so happens to have some really great speakers. And while nothing brings people closer together than wearing a swimsuit and screaming at your friends in the water (only kidding), we are all part of the same community, and we’re all swimming in the same direction.

By Becca Moczygemba, becca@steelmarketupdate.com

The Congressional Steel Caucus held a hearing on The State of the Steel Industry in Washington on Wednesday, June 7, where prominent steel executives and the United Steelworkers (USW) union gave testimony on issues such as international trade and sustainability.

In his opening remarks, US Rep. Frank Mrvan (D.-Ind.), vice-chairman of the Caucus, stressed his gratitude for these witnesses’ commitment “to support our workers, our national economy, and our national security.”

“We know that American workers can compete with anyone in the world when given a level playing field, and I look forward to continuing to collaborate with my colleagues to enhance our trade remedy abilities,” Mrvan said.

Below, please find selected remarks from statements of the witnesses’ testimony in the order that they were listed. Their full remarks can be found here.

Roy Houseman, Legislative Director of USW:

“Regarding the global arrangement and the steel 232, USW remains committed to maintaining the 232 tariff relief and urges Congress to support a successful negotiation of a global arrangement on steel excess capacity and carbon intensity with the European Union (EU),” Houseman said.

Lourenco Goncalves, chairman, president and CEO of Cleveland-Cliffs:

Goncalves said that on May 8 Cliffs completed a successful hydrogen trial at their Middletown Works blast furnace in Ohio, injecting hydrogen into all 20 tuyeres of the furnace.

“This was the first trial of its kind in the Western Hemisphere,” he said. “This groundbreaking use of hydrogen as an iron reductant is a massive step toward the continued decarbonization of the superior steels produced by the blast furnace-BOF route, and utilized by the automotive industry.”

He also said Cliffs is working to bring about a clean hydrogen economy through their participation in two Midwestern hydrogen hubs.

Further in his testimony he said that hydrogen-powered vehicles are a very real alternative to battery electric vehicles.

As Cliffs is an electrical steel producer, Goncalves took issue with a letter sent to President Biden by trade groups led by the National Electrical Manufacturers Association, about the limited availability of electrical steels.

He said Cliffs is “currently producing more GOES (grain-oriented electrical steel) than our customers are able to receive and process.”

Richard Fruehauf, SVP and chief strategy and sustainability officer at US Steel:

“Strong trade enforcement and continuation of the Section 232 national security action on steel imports is critical,” Fruehauf said. “We thank the Caucus for their support of the industry’s AD/CVD cases and confronting unfair trade.”

He highlighted the Caucus’ focus as the US and EU discuss a potential global arrangement on steel overcapacity and decarbonization.

“A successful outcome and agreement would be one that ensures America makes the green steel our nation needs for electric vehicles, our power grid and the clean economy,” he said.

Citing many of US Steel’s projects aimed at sustainability, he touted US Steel’s recently announced new electrical steel product, known as InduXTM, which will begin production at its Big River Steel operation in Arkansas this summer with the commissioning of its new nongrain oriented electrical steel line.

“By producing InduXTM in the United States, US Steel is making a significant investment-$450 million-in American jobs and bolstering the resilience of our country’s domestic supply chain,” Fruehauf said.

Leon Topalian, chair, president, and CEO of Nucor:

“Vigorous enforcement of our nation’s trade laws coupled with pro-growth tax policies have limited the impact of unfairly traded imports and have unleashed a wave of investment by the domestic industry,” Topalian said.

He noted that since the beginning of 2020, Nucor is now more than two-thirds of the way through a $14-billion cap-ex plan that will double the company’s earnings potential from their pre-pandemic levels.

Topalian added that more than 70% of all steel produced in the US is now made by electric-arc furnaces and that will continue to grow in coming years.

“This massive growth in sustainable steel did not happen as the result of any government regulations or subsidies, but by simply letting the market work,” he said.

However, he said that international competitors continue to produce “unrelenting amounts of the dirtiest steel on the planet, often subsidized by their governments.”

He commented, for example, that China has produced more than 1 billion tons of high-emissions steel from integrated mills in each of the last four years.

“We will win if our nation is truly seeking to use the cleanest steel to build out our economy,” Topalian said.

Barbara Smith, chairman and CEO of Commercial Metals Co. (CMC):

“At CMC our products are substantially lower in embodied carbon than both integrated producers and most EAF steel producers globally due to our continuous investment in innovative new technologies,” Smith said.

She commented that over the past five years at CMC, they have commissioned a new micro-mill in Oklahoma.

“In addition, we are in the process of commissioning a first-of-its-kind merchant and rebar combination micro-mill in Arizona and have recently announced the construction of a new micro-mill in West Virginia totaling approximately 1.5 million tons of new steel production capacity and $1.5 billion in capital investment,” she said.

Andy Annakin, chief commercial officer and EVP of Bull Moose Industries:

Annakin said that at the recent Committee on Pipe and Tube Imports (CPTI) annual meeting, members discussed the new EU policy regarding a carbon border adjustment mechanism (CBAM). He added that “we all agreed that Congress should explore legislation that would level the playing field on entries of high-carbon imports by enacting legislation that imposes a cost to imports of high-carbon-emitting steel products.

“This is necessary to prevent carbon leakage in the form of an import surge into the U.S. when the EU, UK and Canada impose carbon tariffs,” Annakin said.

By Ethan Bernard, ethan@steelmarketupdate.com

The US and European Union are working on an agreement dealing with carbon emissions in the steel industry. The impact on bilateral trade could be high. In 2021, the US and EU agreed that the US would suspend the 25% Section 232 tariffs on steel and aluminum, and the EU would drop its World Trade Organization (WTO) litigation against the tariffs, in which it was claimed that the tariffs violated WTO agreements. The two parties agreed that this “ceasefire” would last two years until October 2023. The plan was to reach agreement by then to coordinate efforts dealing with carbon emissions and to address global “overcapacity” in steel and a mechanism to reduce carbon emissions in steel production. (I always put “overcapacity” in quotes because overproduction, not overcapacity, is the true problem.)

Things aren’t going well yet on the carbon front. The EU has developed a program to put a market price on carbon emissions, through a mechanism called the “Emissions Trading System” or ETS. It sets limits, for electricity and industrial processes, based on emissions. Industries, including steel, will have to reduce emissions by 2026. Any company that emits more carbon per ton than the average for that industry must purchase the “right” to pollute from a company that has lower-than-average emissions.

The United States has paid lip service to putting a price on carbon emissions, but the administration does not like a domestic “carbon tax” on US companies. Domestic producers would be happy to impose costs on foreign producers without paying domestic taxes. Bills have been introduced in Congress to impose tariffs on foreign steel based on their carbon emissions, but none has passed yet. A tariff without a domestic tax on carbon would have problems in the WTO.

A CRU study commissioned by the Climate Leadership Council (composed of major corporations and some environmental groups) notes that the US steel industry is much cleaner than most foreign industries, and that about 75% of current US imports of steel are “dirty.” Much of the US cleanliness stems from the fact that over 70% of US production is from electric-arc (EAF) furnace plants, which are much less carbon-intensive on average than blast furnace (BF) plants. Most of the rest of the world is far more dependent on BF plants (and coal-fired electricity).

A carbon tariff would monetize the carbon advantage of US companies, without punishing BF plants in the US or rewarding EAF plants. Again, BF plants tend to produce more carbon emissions than electric furnace mini mills. In the US, plants would be encouraged to improve their carbon emissions by subsidizing new technologies, such as carbon capture and sequestration (CCS). The Inflation Reduction Act has provided a subsidy for installing CCS systems of up to $85 per metric ton of steel. The expense of capturing carbon and putting it in underground storage would be developed largely at government expense, and domestic steel producers would not be required to develop expensive new production technologies, at least not in the near term. Steel companies in the US would largely be able to continue producing steel pretty much as they do now.

This leaves a gulf between the US and EU positions. The EU, which has set a price on carbon through the ETS, combines that domestic policy with a tariff to equalize the costs of carbon reduction between domestic producers and imports. An important feature of this policy, the EU insists, is that competing foreign producers must face similar cost increases for carbon reduction. Otherwise, the European industry will face eternal unfair competition. Countries that impose a price on carbon emissions on their industries will be exempt from the tariffs, but those that don’t will have to pay it. The US seems to be on the wrong side of that line.

The US, however, insists that the carbon emissions advantage the US already possesses, plus the advent of new technologies such as CCS, should exempt US exports to Europe from the carbon border adjustment mechanism (CBAM). The US, it asserts, is part of the solution, not part of the problem.

A recent request from US Trade Representative Katherine Tai to the US International Trade Commission has been viewed as an attempt to build a record of the US advantage in carbon emissions. Ambassador Tai requested the ITC to analyze the actual carbon emissions of US and international steel and aluminum production industries. The ITC study will not be finished in time to meet the October 2023 target for an agreement with the EU. Perhaps the US will offer to maintain the status quo until the report comes out in January 2025. To bolster this point, Senators Chris Koons (D-Del.) and Kevin Cramer (R-N.D.) have introduced a bill to require the Energy Department to conduct a similar study of energy-intensive industries (steel, aluminum, oil, gas and certain critical minerals) in the US and major foreign producers. Seven other US senators are cosponsors of the “PROVE IT” Act.

If the two sides cannot bridge what is a yawning chasm between their positions, the continued suspension of Section 232 tariffs could be in question as early as October of this year. Direct threats have not surfaced yet, and there may be a chance to kick the can down the road until after the 2024 elections in the US. But the danger is not zero.

Both the US and the EU are still learning how to deal with a relatively new international trade problem. Global trading rules have historically not bothered much with how a product is made. Slave labor and child labor have been the major exceptions until recently. Measuring tariffs by how “dirty” a production process might be are thought by many countries in the developing world as a hit against them as they become more competitive in manufacturing.

Climate issues present a host of new challenges. Energy-dependent industries like steel and aluminum are responsible for carbon emissions from electric utilities. European and American manufacturers would be incentivized to insist on greater renewable energy production so that their products would be cleaner. But utilities must invest to clean up energy production. There are interim measures, such as replacing coal-fired generation with natural gas, that will help.

Most experts consider that both subsidies and taxes (carrots and sticks) could help change the way the world’s industries produce things. Considering that the problem is global, good ideas should ideally be shared—another new concept in intellectual property.

The US-EU impasse should not be that hard to resolve through compromise. Consider, however, that carbon emissions are increasingly produced by manufacturers in emerging economies. A tax on carbon emissions will likely generate tensions between the developed and developing worlds. That will be much harder to deal with than the spat between the EU and the US.

Lewis Leibowitz

The Law Office of Lewis E. Leibowitz

5335 Wisconsin Avenue, N.W., Suite 440

Washington, D.C. 20015

Phone: (202) 617-2675

Mobile: (202) 250-1551

E-mail: lewis.leibowitz@lellawoffice.com

The latest SMU Market Survey results are now available on our website to all Premium members. After logging in at steelmarketupdate.com, visit the Analysis tab and look under the “Survey Results” section for “Latest Survey Results.”

Historical survey results are also available in the Survey Results section under “Survey Results History.”

If you need help accessing the survey results, or if your company would like to have your voice heard in our future surveys, contact david@steelmarketupdate.com.

By David Schollaert, david@steelmarketupdate.com

The LME aluminum three-month price is moving higher again as the week ending June 9 closes trading at $2,230/t. Failing to dip below the critical transition price of $2,000/t, The LME steadied itself despite very lackluster demand anywhere in the world.

Trading in China also kept the regional exchange there neutral, if not a bit higher as SHFE aluminium prices also made some moderate gains the same week. The cash price settled at RMB18,480/t and last traded at RMB18,540/t.

US Midwest Weakens Week Over Week at $0.241- $0.246¢/lb

The US Midwest premium spot is more stable in recent times compared to the extreme fluctuations earlier in the year. It looks quite docile entering June compared to this time last year as the premium was above $0.30/lb. However, it has dropped a fraction the week ending June 9 due to current market sentiment. Shipments as reported by the Aluminum Association are down double digits year to date (YTD) vs. 2022 for extruded products, and nearing this same level for rolled products. Imports are also down heavily across the board. Right now, the only bright spots in the industry are the automotive end-use demand and hard alloy defense and aerospace applications.

Looking at the commitment of trader report from the CME, open interest has been level, but speculators have been building a long position in the market with almost zero short interest. This could suggest that despite the weakening in the short term and a backwardation on the futures curve, a demand push could bring the premium back higher. The potential for lower interest rates in 2023 H2 may provide the catalyst for a rally.

US Manufacturing Base Shrinking

It was clear back in March 2022, when the Federal Reserve began its current rate hike cycle, that rising interest rates and quantitative tightening were going to slow the US economy. The housing market, and the construction sector by extension, were quick to fall victims to higher borrowing costs, and manufacturing industries were not long behind.

Manufacturing output started flattening out since mid-2022, and while there were occasional small monthly increases, such as a 1% rise in April 2023, manufacturing output remains slightly below the pre-pandemic level, in contrast to GDP, which is 6% above the pre-pandemic level.

The ISM Purchasing Manager Index for the manufacturing sector also saw a small increase from 46.3 to 47.1 in April 2023, but in May the downward trend resumed with a reading of 46.9. In fact, the Manufacturing PMI signaled that the sector began contracting back in November 2022, and since then the index has not left recessionary territory.

May 2023 marks the seventh straight month of contraction in the Manufacturing PMI. When we break-down all five categories that make up the Manufacturing PMI, four of them came below 50-mark in May, the exception being the employment index.

The new orders index has remained in recessionary territory since September 2022, signaling weakening new demand. The new export orders index continued declining, reflecting weak global demand and a strong dollar – since despite the troubles in the banking sector and last-minute debt ceiling negotiations, the US dollar remains resilient. While a strong currency helps limit inflation for consumers, it also reduces competitiveness of US exports.

The inventories index fell below 50 in March 2023 as supply-chain bottlenecks have eased and liquidity improved. The supplier deliveries index has been below the 50 breakeven point since October 2022, signaling faster deliveries of suppliers to manufacturers. However, the fact that in May 2023 the supplier deliveries index reached the lowest level since March 2009 also clearly demonstrates slowing activity.

The prices index has been volatile, reflecting that some manufacturing industries have been doing better than others. However, the prices index came at 44.3 in May 2023, which is the lowest level since December 2022, consistent with the big fall in US PPI inflation, which is now negative year over year (y/y). The employment index has shown resilience, as hiring in the sector continues at a solid pace.

Soft FRP and Extrusion Demand With Lower Logistics Costs Invite Imports

The threat of increased imports and price erosion remains for domestic aluminum producers and consumers. While it is reasonable to conclude that the supply chain lessons learned during the pandemic rush will be long lasting, some opportunistic buying will take place to test the friend-shoring trend. Service centers, buying for nearby demand, will test this market if only to average down inventory values and stay aligned with competitors on this slippery slope.

There is good news coming out of the prolonged negotiations between the International Longshore, and Warehouse Union (ILWU) and the Pacific Maritime Association (PMA). Both parties have recently signaled that a new collective bargaining agreement is at hand. The deal covers 22,000 workers and 70 companies, respectively, serving 29 West Coast ports. Slack demand in 2022 H2 and in 2023 Q1 has certainly taken the pressure off the ports. Still, word of an agreement will be welcome news that will support aluminum trade flows, in and out of North America.

The over-the-road loads to equipment ratios are steady through 2023 Q2. Van loads and equipment availability continued to be 2:1, and flatbed accessibility stabilized near 12:1, load to equipment ratio. This time last year, the van and flatbed load ratios were two and six times higher, respectively. Fuel prices moved lower, too, down -20% since the beginning of the year. Logistics metrics remain effective demand indicators. Any uptick in demand will find adequate transport service levels to deliver timely as lead times for rolled products and extrusions remain short. Only heat-treatable alloy plate remains on allocation as demand for aerospace, semiconductor tooling and defence applications remain immune from the economic malaise.

Learn more about CRU’s services at www.crugroup.com

By Stephen Williamson, CRU Research Manager, stephen.williamson@crugroup.com

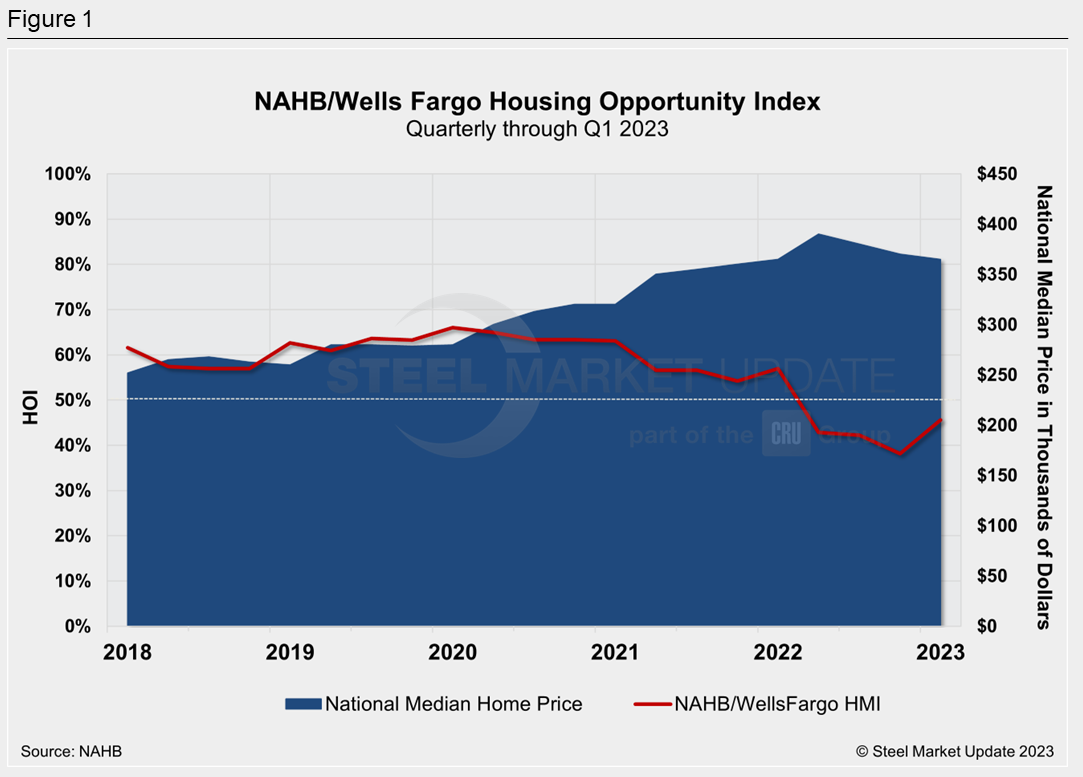

Housing affordability is on the rise in the US, but builders are facing challenges in providing affordable housing, the National Association of Home Builders (NAHB) reports.

In the first quarter of the year, 45.6% of new and existing home sales were affordable to American families earning the country’s median income of $96,300, according to the NAHB/Wells Fargo Housing Opportunity Index (HOI). This was an increase from the lowest level seen since NAHB began tracking affordability – the 38.1% posted in Q4 last year.

Affordability is down, however, from Q1 last year when the HOI hit 56.9%. And it remains below the breakeven point of 50, NAHB noted.

“An uptick in housing affordability in the first quarter of 2023 corresponds to a rise in builder sentiment over the same period as well as an increase in single-family permits,” commented NAHB chairman Alicia Huey.

“And while buyer conditions improved at the beginning of the year, builders continue to wrestle with a host of affordability challenges. These include a shortage of distribution transformers and concrete that are delaying housing projects and raising construction costs, a lack of skilled workers, and tightening credit conditions,” she added.

The national median home price in Q1 declined by $5,000 from the prior quarter to $365,000, NAHB said. At the same time, average mortgage rates fell slightly from 6.8% to 6.46%, and the US median family income increased by 7%, or $6,300, to $96,300.

NAHB said the top five affordable major housing markets in Q1 were: Lansing-East Lansing, Mich.; Scranton-Wilkes-Barre, Pa.; Rochester, N.Y.; Toledo, Ohio; and Pittsburgh, Pa. The top five least affordable major housing markets were all located in California.

By Laura Miller, laura@steelmarketupdate.com