CRU analysts Thais Terzian and Frank Nikolic will be the featured guests on the next SMU Community Chat on Wednesday, July 9, at 11 am ET.

The live webinar is free for anyone to attend. A recording will be available to SMU subscribers. You can register here.

What we’ll talk about

Terzian is a principal analyst at CRU, where she leads crude steel and metallics analysis. She’ll focus on both metallics and semi-finished goods as well as developments across steel markets in Americas. In other words, we’ll discuss not only the North American steel market (as we usually do) but also developments in South America – and how they impact markets here.

Nikolic is vice president of base and battery metals for CRU. We’ll delve into what’s happening in those markets with a particular focus on zinc – a key raw material for anyone in the galvanized steel market.

CRU is SMU’s parent company. And both Terzian and Nikolic bring a wealth of knowledge to the issues that matter to you. They’ll also be speaking at SMU Steel Summit. (The agenda for Summit is here. And you can register here.) So think of this as a preview of what they’ll discuss in Atlanta – and a good way to get the conversation going before Summit kicks off on Monday, Aug. 25.

As always, we’ll keep it to about 45 minutes. You can drop in, learn something – and then get on with your day. We’ll take your questions too. So remember to think of some good ones for the Q&A on Wednesday, July 9, at 11 am ET!

Editor’s note

If you’d like to see past Community Chat webinars, you can find those here. I suggest checking out a good one we did on June 25 with Ken Simonson, chief economist for the Associated General Contractors of America (AGC). We discussed the impact of President Trump’s tariffs, immigration crackdown, and tax cuts on construction.

Form letters sent to Japan and South Korea’s leaders stating that US President Donald Trump plans to apply 25% tariffs on goods from each nation beginning on August 1 are not applicable to steel or aluminum imports.

In his July 7 correspondence with US trade partners, Trump announced that he was changing his July 9 reciprocal tariff implementation.

“Starting on Aug. 1, 2025, we will charge [Korea/Japan] a Tariff of only 25% on any and all [Korean/Japanese] products sent into the United States, separate from all Sectoral Tariffs,” Trump’s letter stated.

During a White House press briefing on Monday, White House Press Secretary Karoline Leavitt told reporters that the president plans to send 12 other countries similar letters.

“The president will sign an executive order today delaying the July 9 deadline to Aug. 1, so the reciprocal tariff rate or these new rates that will be provided in this correspondence to foreign leaders will be going out the door in the next month. Or deals will be made in those countries continue to negotiate with the US,” Leavitt said.

She added: “The president and this trade team want to cut the best deals for the American people and the American worker. That’s what they’re focused on.”

Trump did not make explicit note of sectoral tariffs for imports from Vietnam in his Truth Social post last Wednesday. On July 3, SMU analyzed potential tariff scenarios on Vietnamese exports of steel and aluminum to the US via Final Thoughts.

SMU continues to reach out to steel groups and the administration to understand whether the president was including steel and aluminum in his “any and all goods” statement last week.

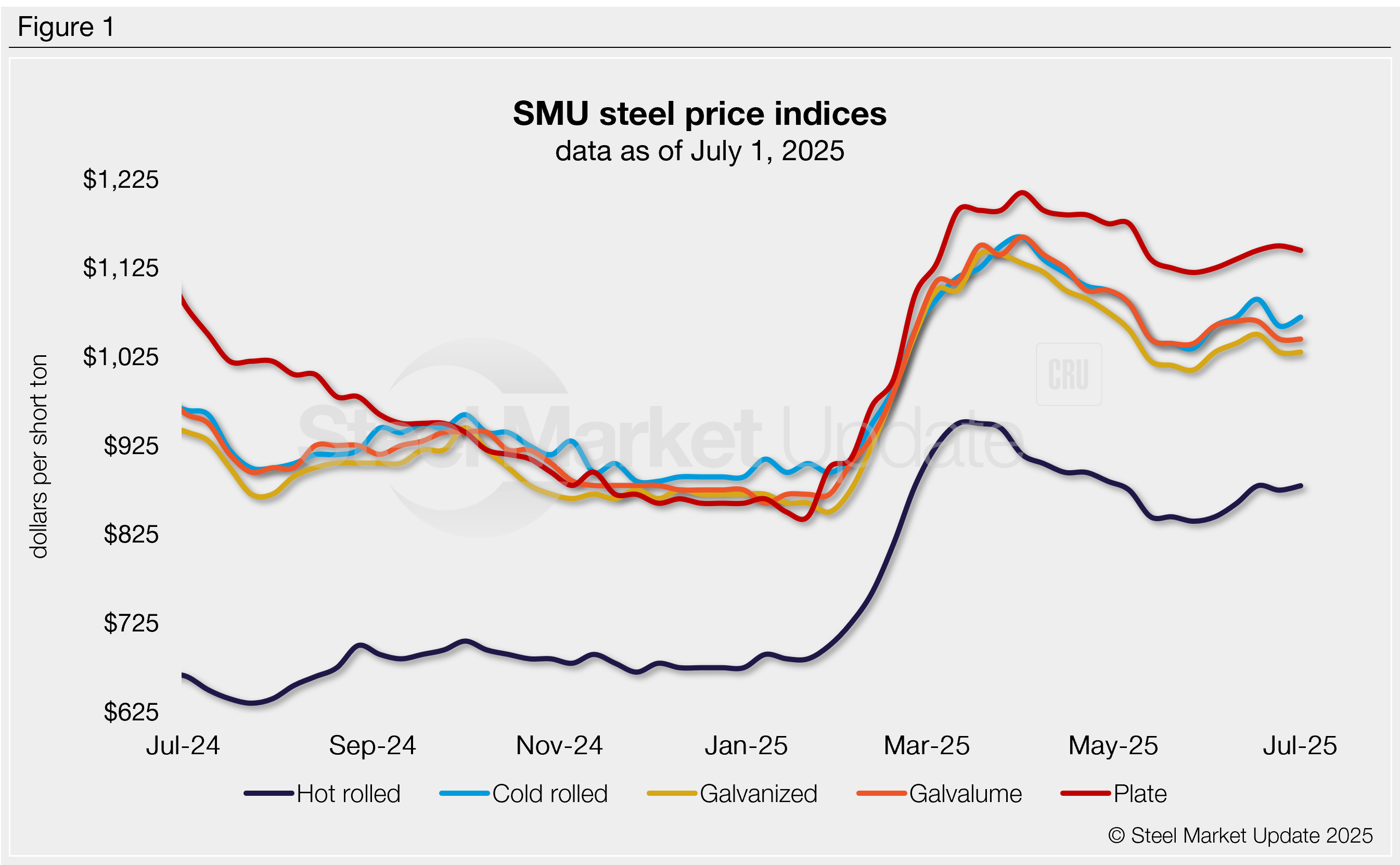

Domestic steel mill output inched higher last week, according to the American Iron and Steel Institute (AISI). Raw production remains historically strong and has been growing steadily since April.

US mills produced an estimated 1,781,000 short tons (st) of raw steel for the week ending July 5 (Figure 1). Output rose by 5,000 short tons (st), or 0.3%, from the previous week and sits just 6,000 st below the three-year high seen in mid-June.

Last week’s production was 4.8% above the year-to-date (YTD) weekly average of 1,700,000 st and 4.9% higher than the same week one year ago.

The mill capability utilization rate was 78.6%, down slightly from the previous week (79.1%) but well above one year ago (76.5%). Note that AISI updated its total capacity estimates last week, raising annual capacity from 116.8 million st to 117.8 million st. As a result, even though production rose, utilization declined.

YTD production now stands at 45,199,000 st with a capability utilization rate of 76.0%. Mills have produced 0.5% more steel this year than in the same period of 2024. Prior to June, 2025 output had been trailing last year’s pace.

Raw production increased week over week (w/w) in four of the five AISI-defined regions:

Northeast – 123,000 st (up 2,000 st w/w)

Great Lakes – 563,000 st (up 3,000 st)

Midwest – 231,000 st (up 5,000 st)

South – 791,000 st (down 7,000 st)

West – 73,000 st (up 2,000 st)

Editor’s note: The raw steel production tonnage provided in this report is estimated and should be used primarily to assess production trends. The graphic included in this report shows unadjusted weekly data. The monthly AISI “AIS 7” report is available by subscription and provides a more detailed summary of domestic steel production.

Nucor is keeping its list price for spot hot-rolled coil unchanged after last week’s shortened holiday week.

The steelmaker said in a letter to customers on Monday that, effective immediately, its consumer spot price (CSP) for HR coil would be $910 per short ton.

The price is flat from last week but up $40/st from the start of June.

Nucor also said pricing at its West Coast joint venture, California Steel Industries (CSI), would remain unchanged from last week at $970/st.

You can track steel mill price announcements using the calendar on our website.

Charlotte, N.C.-based Nucor also said it would continue to offer HR lead times of 3-5 weeks.

On July 1, SMU assessed spot HR coil prices at $840-920/st, averaging $880/st.

A week earlier, on June 26, we pegged HRC lead times between three and six weeks, with an average of 4.4 weeks.

Watch for updated steel prices on Tuesday and the latest mill lead times in Thursday evening’s newsletter.

I’m not sure how many different ways I can write that it’s been a quiet market ahead of Independence Day.

There are variations on that theme. I’ve heard everything from the ominous “eerily quiet” to “getting better” and even the occasional “blissfully unaware” (because I’m enjoying my vacation).

If you want to get a more detailed idea of what buyers are thinking, check out our latest edition of “Market Chatter.” You’ll see the word “uncertainty” a lot, and more than a little concern about demand. More on that in a moment.

I think this much is fair to say. We saw more activity in June after President Trump announced in late May that Section 232 tariffs on imported steel would double to 50%.

The logic was pretty simple: People knew higher tariffs today would lead to higher prices tomorrow – and so they went out and bought. Was there a frenzy of activity like we saw when Trump made a similar announcement about tariffs in February? No. But there was an uptick.

Get ready for a quiet spot market in July

Let’s say you have a monthly contract based on a discount to spot prices for the prior month. And let’s say your contract discount is 6-8%. SMU’s hot-rolled coil price for May averaged $851 per short ton (st) in May. That would put June contract prices at $780-$800/st.

And, sure enough, spot prices did go up in June on higher tariffs. So let’s make the same assumption for July contracts. SMU’s spot HR price averaged $875/st in June. (Editor’s note: You can go to our Interactive pricing tool and select monthly averages to find that price.) That would put contract prices at $805-825/st for July. That’s up, but it’s still well below the spot HR prices published by Nucor ($910/st) and Cleveland-Cliffs ($950/st).

Let’s assume, using some rough numbers, that your company typically buys 50% spot and 50% contract. Let’s also assume that you’re unsure of demand and doubly cautious because you’re unsure about tariffs too. Why wouldn’t you put as many tons as possible under contract and buy only what you absolutely need to on a spot basis?

I guess what I’m saying is that it could be a very quiet July as far as spot activity goes. Which shouldn’t be a surprise. Steel production is up vs. a year ago, according to the American Iron and Steel Institute data (AISI). And consumption is down if for no other reason than OEM summer outages.

Last year, we saw spot HR prices slide from $670/st on average at the start of July to $640/st on average by the end of the month. (And big buyers were at $600/st or lower.) If you’re a mill, the good news is that tariffs and duties (on coated products in particular) have put a much higher floor under prices.

What comes next?

The big question is, when does activity improve? I think we could see the typical seasonal dance. OEMs will start to come out of their summer shutdowns in August, which should help to stabilize prices. And then mills will start taking their fall outages, just as OEMs are fully ramped up again – which should give mills a stronger hand to increase prices in the fall. (Why mills and OEMs don’t align production schedules is a question for another day.)

Based on that alone, I can see the logic from those of you who are bullish about the second half. There are other reasons to be bullish about the back half of the year. I’ve heard from some of you that inventories are moving lower.

We’ll release June service center inventory data to our premium subscribers on July 15. I’m not going to guess what that data will show. (That data is a good reason to upgrade from executive to premium. Contact SMU account executive Luis Corona at luis.corona@crugroup.com to learn more.) But it’s true that inventories have come down sharply since the start of the year. It’s also true that buyers continue to be cautious about building stocks.

I’ve also heard from some mills that you’re discounting less – even if it’s on fewer tons – because you have less competition from imports and because domestic buyers have shifted purchases to US mills.

Import license data was not complete for the June when I wrote this article. That said, through June 23, the US Commerce Department had recorded licenses to import about 518k st (470k metric tons) of steel to the US. That’s about 23k st per day. If that rate continued, imports would be approximately 679k st in June. That would mark the lowest point for flat-rolled steel imports since ~600k st (545k mt) in January 2021 – when the market was still getting on its feet after the worst days of the pandemic.

That trend might help explain not only why producers feel less need to discount but also why high steel production levels during the summer doldrums haven’t led to lower prices.

Truth be told

Speaking of imports, I’ve been asked by some of you what President Trump’s announcement about 20% tariffs on Vietnam means for the steel. As most of you know, Trump himself broke the news on Wednesday in a post on Truth Social.

On the one hand, a 20% tariff represents a doubling of the 10% tariff Vietnam had previously been subject too. On the other hand, steel is subject to a 50% tariff. So did Vietnamese steel – which has been among the lowest-priced import material in the US market – just get a tariff reduction?

When I was writing this column, the question was whether the phrase “any and all goods” in Trump’s “truth” might refer to steel. As best as I can tell, the answer is, no, Vietnam’s steel tariff has not been reduced.

Here is why, according to folks in the industry I’ve talked to. The 20% is in reference to Vietnam’s tariff under the International Emergency Economic Powers Act (IEEPA), which is separate from Section 232 tariffs. And the Section 232 tariff for Vietnamese steel (like that for almost all other countries) remains at 50%.

But I don’t know that anyone is going to outright say that until an executive order or proclamation saying as much has been posted on the White House website. Because with Trump, you never know for sure until you see it in writing – and even then, there might be some lingering questions.

It’s exciting/funny/sad (probably depending on your politics or lack thereof) that we’re approaching ALL CAP Trump “truths” like religious text – seeking the higher meaning. Maybe we’ll get some clarity later today or over the long weekend. For now, I’m planning to enjoy the fireworks on Friday and time with friends and family.

SMU’s offices will be closed on July 4 and over the weekend. We’ll be back at it again on Monday.

SMU Steel Summit

The agenda for this year’s SMU Steel Summit is nearly complete. If we have any last-minute additions, you’ll see them first here. So stay tuned!

Also, we’ll be hosting an SMU Community Chat next week with CRU analysts Thais Terzian and Frank Nikolic. They’ll discuss the outlook for metallics, semi-finished products, and zinc. You can find out more and register here.

Fun fact: Thais and Frank will also be speaking at Steel Summit. So think of the Chat as a good way to start a conversation that we’ll continue in person at the Georgia International Convention Center (GICC) in Atlanta on Mon-Weds, Aug. 25-27.

Nearly 950 people have already registered to attend from dozens of companies. If you’re not already on the list of companies attending, we hope to see you there soon.

In the meantime, happy Independence Day to everyone in the US. And a belated happy Canada Day to our friends in Canada.

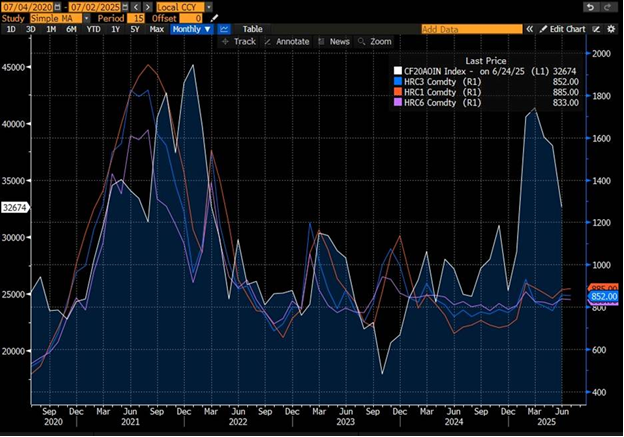

As you head into the long weekend, here is a recap of where things stand in hot-rolled (HR) coil futures along with some key datapoints.

Nucor increased its consumer spot (CSP) for hot-rolled coil (HRC) to $910 per short ton (st), up $10/st from last week. Backwardation persists in the forward HRC, with front months refusing to cross the $900/st level. The anchor CRU index print on Wednesday is a key cause for relative strength in July ‘25. But heading into Aug. ‘25-Oct. ’25, we see an average decline of ~$15/st per month.

The tariff backdrop is lending support to mill pricing power. But the price spikes from tariff headlines over the last several months have been muted compared to past price spikes. (The pandemic in ’20-21 and Russia’s full-scale invasion of Ukraine in ’22, for example.)

One key consideration is net positioning in CME futures. It had been on the ascent in 2025 until a rapid cut of exposure in June ‘25. As of June 24th, Commitment of Traders (COT) data points indicate that physical participants reduced length by 2,260/st while maintaining net long.

Managed money also sits on the long side of the market and added 8,940/st. Swap dealers’ primary positioning is in spreads. However, they added 6,180st to their short positioning. Other reportable positions sit net short and added 10,660st to their shorts. We can interpret that managed money still has expectations of price strength while physical participants are running closer to a balance on a net basis.

CME HRC M1, M3, M6 and CFTC net positioning

On the forward-looking side, mill margins are at healthy levels above $400/st on average. That’s partly because busheling scrap has dropped on a dollar basis from the $500 per gross ton (gt) prices seen earlier this year. Capacity utilization, according to the American Iron and Steel Institute (AISI) is at a healthy 79.1%.

Forecasted consumption upticks from new mill capacity heading into Q3 should be supportive for scrap pricing and, in turn, demand. Turkish import levels have been rangebound for HMS 80:20. I would put chances of an export price push on cut grades at limited.

Disclaimer

The views and opinions expressed in this column are solely those of the author, Joshua T. Toney, Principal of Corsair Elements LLC. This material is provided for informational and educational purposes only and does not constitute investment, trading, legal, or financial advice. Corsair Elements LLC is not registered with the Commodity Futures Trading Commission (CFTC) or the National Futures Association (NFA). Nothing contained herein constitutes a solicitation or recommendation to buy or sell any commodity interest, futures contract, swap, or other financial instrument. Readers should consult their own professional advisors before making any financial decisions.

With so much happening in the news cycle, we want to make it easier for you to keep track of it all. Here are highlights of what’s happened this past week and a few upcoming things to keep an eye on.

It will be a shorter week as the United States celebrates Independence Day on Friday. But we won’t leave you high and dry.

The so-called One Big Beautiful Bill, which President Trump had been championing, passed in the Senate and has been sent back to the US House of Representatives for reconciliation.

Several items in the bill would impact the steel industry. We will be reporting those to you. So far, portions of the 2017 Tax Cuts and Jobs Act, scheduled to expire at the end of 2025, have been extended.

The Steel Manufacturers Association and the American Iron and Steel Institute applauded the tax provisions included in the bill. You can see what they said here, with the caveat that the bill still has not been passed.

Prices

On Monday, Nucor raised its weekly spot list price for hot-rolled (HR) coil by $10 per short ton (st) to $910/st after holding it steady at $900/st the previous week.

At the same time, Nucor is also aiming to keep plate prices flat again with the opening of its August order book.

Sheet and plate prices were little changed this holiday week. SMU’s average HR coil price inched up $5/st to $880/st. Prices for other products were also little changed. You can see how cold-rolled coil and other products reacted – and what market sources are saying – here.

Trade

The US government is moving on trade petitions filed earlier this month by a coalition of domestic steel producers. The Commerce Department officially initiated unfair trade investigations into rebar imports from Algeria, Bulgaria, Egypt, and Vietnam. You can find the latest here.

Canada has implemented tariff-rate quotas on steel imports to help protect and stabilize its domestic market. Notably, the TRQs do not apply to countries that have a free trade agreement with Canada. Find out the details here.

Around the market

GE Appliances will be reshoring the production of some of its appliances to its Louisville, Ky., headquarters with a $490-million reshoring project positioning it to become the “biggest American washer manufacturer.” Recall that appliance maker Whirlpool said the company expects tariffs to boost business as it looks to invest in its US-based operations.

Cleveland-Cliffs’ previously announced idlings at its Riverdale, Ill., Conshohocken, Pa., and Steelton, Pa., mills have gone into effect. That’s according to WARN notices from the affected states and Cliffs’ website.

Economic data to watch out for

Tuesday, July 8: Consumer credit (3 p.m.)

Wednesday, July 9: Minutes of Fed’s May FOMC meeting (2 p.m.)

Thursday, July 10: Initial jobless claims (8:30 a.m.)

US mills shipped slightly less steel in May than in April, according to the latest figures from the American Iron and Steel Institute (AISI).

Domestic mills shipped 7,507,349 short tons (st) of steel in May, down 1% from 7,580,635 st in April, AISI said in data released on Thursday.

But despite recent shipment declines, 2025 volumes are still ahead of 2024 shipment levels.

Case in point: Shipments in May 2025 are 1% higher than shipments of 7,431,201 st in May 2024. And through the first five months of 2025, US mills had shipped 37,285,289 st. That’s up 1.9% from 36,607,546 st in the same period last year, per AISI.

AISI also offered the following product specific tallies for the first five months of 2025 compared to the first five months of 2024: hot-rolled sheet and strip – down 2%, cold-rolled sheet and strip – up 1%, and coated sheet and strip – up 1%.

Steel trade groups praised the passage of the Big Beautiful Bill (BBB) as it passed in the House of Representatives on Thursday.

The bill has been approved by both the House and Senate. It will now be sent to President Trump’s desk where it is expected to be signed within days.

American Iron and Steel Institute responds

AISI President and CEO Kevin Dempsey applauded the passage of the bill, which extends provisions of the 2017 Tax Cuts and Jobs Act (TCJA). Some of these were scheduled to expire at the end of 2025.

Dempsey also noted the bill includes several other improvements to the US tax code.

For the US steel industry, in particular, as well as manufacturing, Dempsey noted the importance of a number of tax provisions.

“Many of the key capital cost recovery provisions from the 2017 tax law have expired or were scheduled to be phased out, including 100% bonus depreciation for business investment, immediate expensing for domestic research and development expenses, and the EBITDA-based standard for business net interest deductions,” Dempsey said in a statement on Thursday.

He commented that these rules have a record of fueling innovation and economic growth.

“Today’s action to restore these measures and make them a permanent part of the tax code will allow many companies to invest in steel-intensive facilities and equipment,” Dempsey added.

Approval of the Steel Manufacturers Association

Likewise, SMA President Philip K. Bell cheered the BBB’s passage.

“Passing the One Big Beautiful Bill Act and sending it to President Trump’s desk for signature means America will continue to be the premier destination for manufacturing,” Bell said in a statement on Thursday.

He noted that since President Trump’s first term, steelmakers have been making major investments.

“The steel tariff and the Tax Cuts and Jobs Act (TCJA) have helped steelmakers invest in their facilities, their workers and their communities,” Bell said. “The One Big Beautiful Bill will work to turbocharge those investments and help drive new ones.”

He cited driving innovation and lowering the cost for manufacturing equipment as positive effects the bill will have on the domestic steel industry.

“This legislation puts our industry in a strong position to continue making momentous investments and supporting America’s coming economic renaissance,” Bell concluded.

The United Steelworkers (USW) union applauded news that private equity firm Atlas Holdings has agreed to acquire Evraz North America.

Evraz NA, a union-represented company, was put up for sale in 2022 when sanctions were imposed on its parent company.

Mike Day, president of USW Local 5890 in Regina, Saskatchewan, said workers there are relieved after years of uncertainty.

“This has been a long and difficult process for our members, who have worked through uncertainty with professionalism and pride in their work,” Day said in a press release.

“We’re hopeful this marks the beginning of a long and positive relationship with Atlas. Our members are ready to continue doing what they do best by producing high-quality Canadian steel that supports our economy and our communities,” he added.

USW sources in the US said their sentiments align with the statements issued by union members in Canada.

The sale is expected to close in the second half of 2025. Atlas Holdings is rumored to have agreed to pay $500 million for Evraz NA.

Evraz NA operates facilities in western Canada that primarily make energy tubulars for the region’s oil-and-gas sector. Its US operations include a plate mill in Portland, Ore., and a mill in Pueblo, Colo., that makes rail, wire rod and coiled rebar, as well as seamless pipe. The company also operates scrap recycling facilities in both countries.

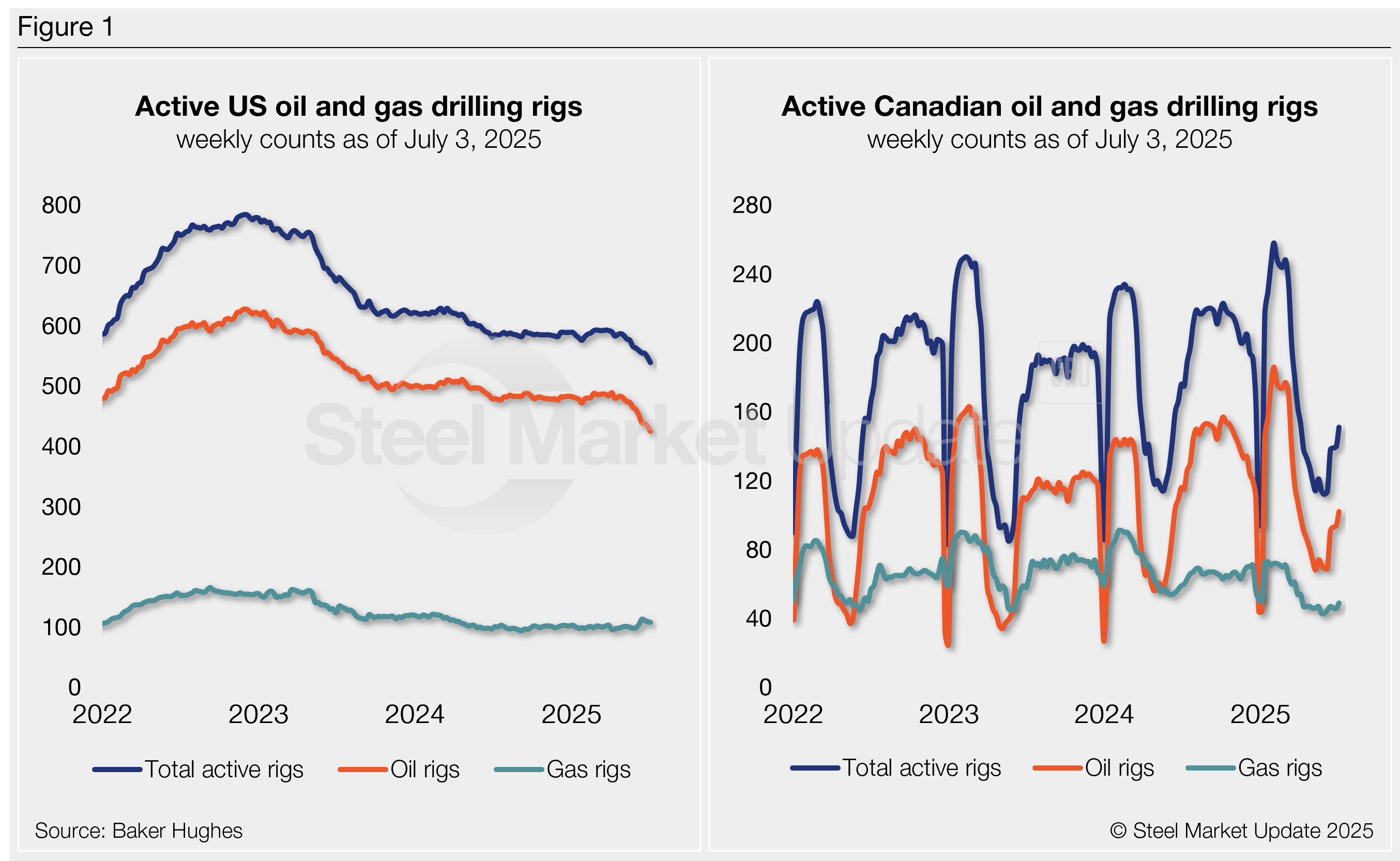

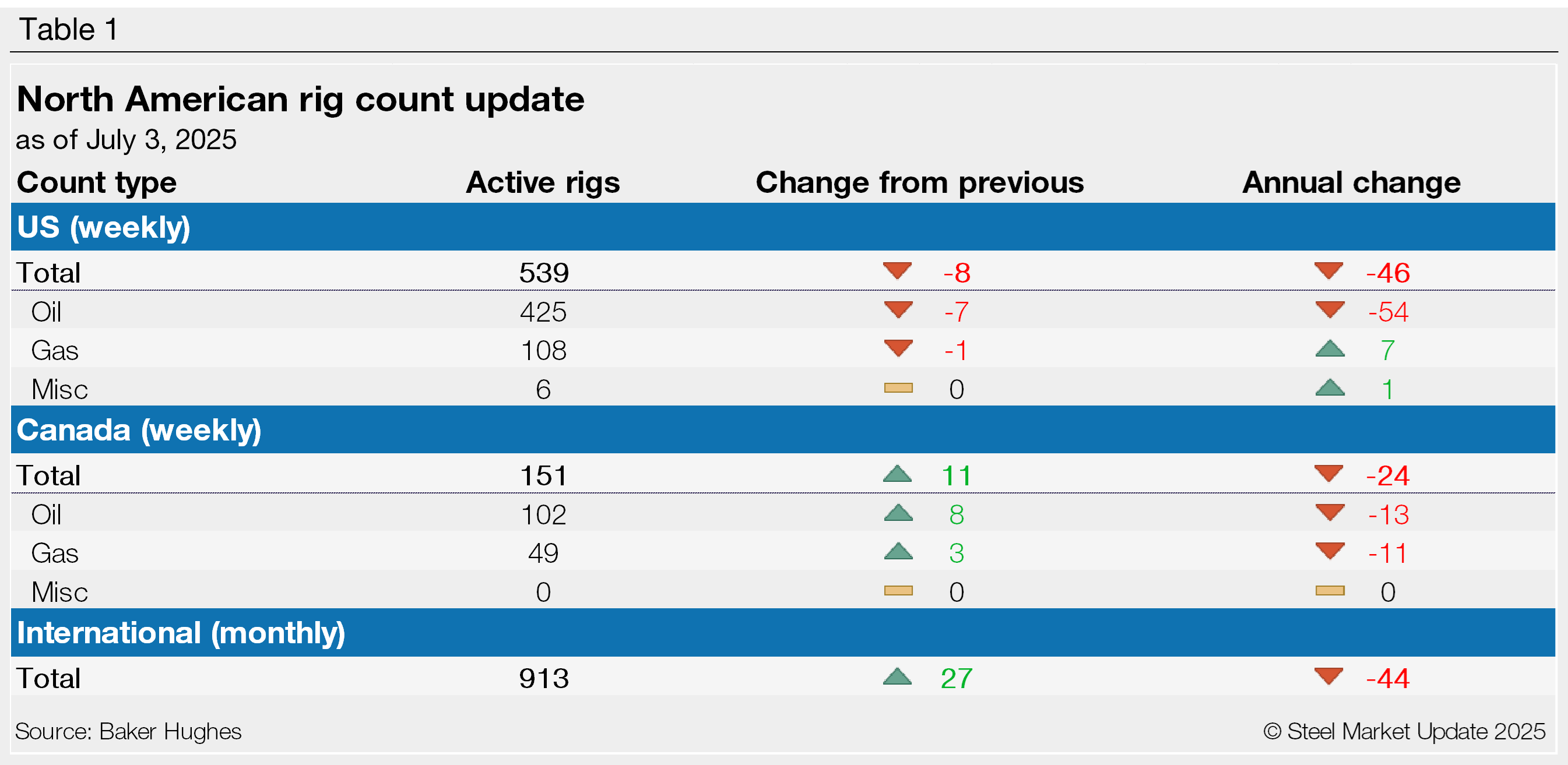

The rig count declined for the 10th consecutive week in the US, while the Canadian count rose for the fifth straight week, according to Baker Hughes.

The US rig count fell by eight this week to 539, the lowest rate since October 2021. Compared to the same week last year, 46 fewer rigs are in operation today.

Canadian activity improved by 11 rigs this week, now up to a 13-week high of 151 rigs. The Canadian count is down by 24 from this time last year. Activity typically slows down each spring as thawing ground conditions limit access to drilling sites, then picks back up in June and July.

The international rig count is reported monthly at the beginning of each month. The June count was 913 rigs, up 27 from May but 44 fewer than one year ago.

The Baker Hughes rig count is significant for the steel industry because it is a leading indicator of oil country tubular good (OCTG) demand, a key end market for steel sheet.

For a history of the US and Canadian rig counts, visit the rig count page on our website.

Triple-S Steel Holdings has closed on its previously announced acquisition of American Stainless Tubing.

The deal was a $16-million all-cash transaction, subject to customary closing conditions.

North Carolina-based American Stainless Tubing was acquired by First Tube LLC, a subsidiary of Triple-S, from Ascent Industries, a specialty chemical company.

Note that Angle Advisors was the exclusive investment banking advisor to Ascent for completing the transaction, according to a statement from Angle Advisors on July 2.

Houston-based Triple-S is a privately owned steel service center with over 60 locations.

On Wednesday, July 2, Cleveland-Cliffs marked a milestone in American stainless steelmaking, holding a ribbon-cutting ceremony for its new $150 million bright anneal line at its Coshocton Works in Ohio.

Photo courtesy of Cleveland-Cliffs.

Chairman, President, and CEO Lourenco Goncalves stood flanked by state leaders and union workers, touting the project as proof that US manufacturing is not only alive, but also advancing.

According to the Cleveland-based steelmaker, the high-tech line uses a 100% hydrogen atmosphere. It replaces acid-based processing with a recovery unit that recycles gas back into the system.

The line is designed to serve high-end auto and appliance markets. At the same time, it is pushing back against imported material, mainly stainless steel produced in Finland but routed through Mexico, Goncalves said.

“We are now producing in Ohio something that used to be produced in Finland… That’s what we are stopping by doing investments,” he added.

Ohio Governor Mike DeWine called it “a great day for Ohio,” praising the project’s economic and security implications. “Making steel in the United States is about jobs. It’s about good-paying jobs. It’s also about national security,” he said. “We learned during the pandemic—we have to make the essential things here.”

Union leaders echoed the enthusiasm. “Had it not been for the 232 tariffs that were put in place, we would not remain competitive,” said Kurt Knicely, president of the United Auto Workers (UAW) Local 3462.

Knicely credited the leadership at Cliffs for putting their faith in the Coshocton workforce and building the line with American steel, much of which was sourced from Ohio.

The line was built “from what was a grassy field four years ago,” Knicely commented, by union contractors and employees who logged thousands of hours. “This directly benefits the community,” he remarked.

Ohio’s Secretary of State Frank LaRose called the event “a great Ohio story,” noting that American workers “can compete with anyone around the world when they’re on a level playing field.”

“This is what the America First agenda is all about,” added Republican Senator Jon Husted.

“This is not an investment I’m promising. It’s an investment we have already concluded,” Goncalves noted.

“There’s no problem to invest in the United States of America when you have the market conditions to survive as a business,” the chief executive added.

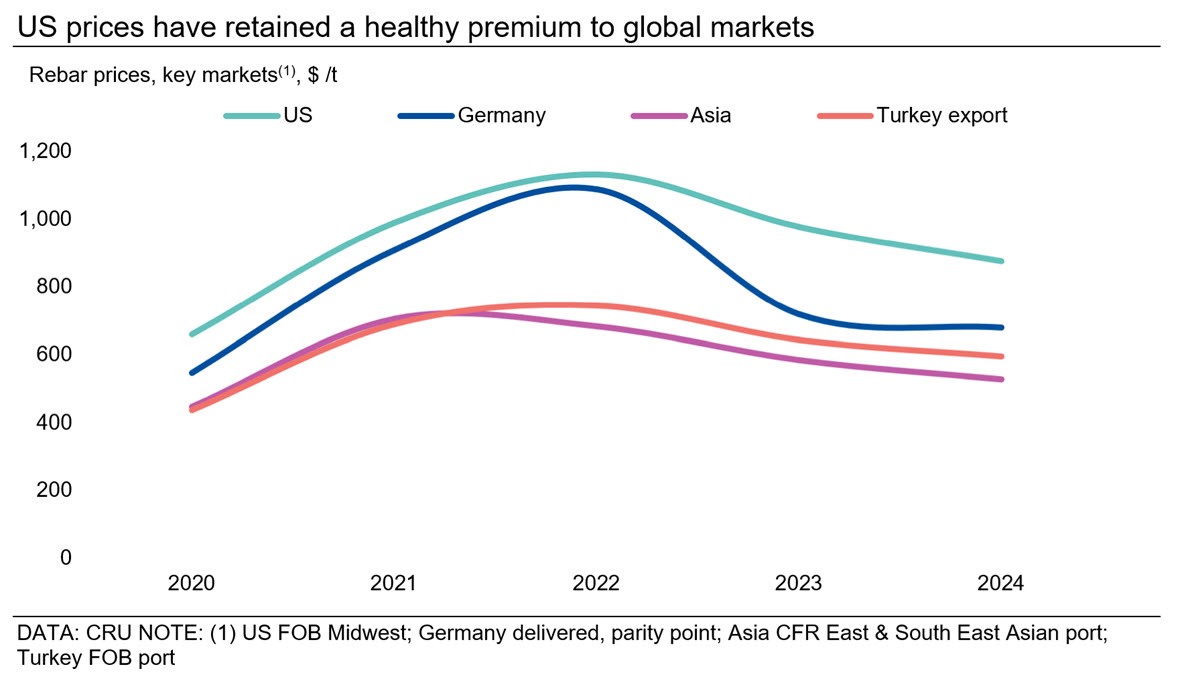

Following the onset of the war in Ukraine in March 2022, concerns about import availability and expectations of rising demand from President Biden’s Infrastructure Bill pushed US rebar prices to record highs. In response, a flurry of new mills and capacity expansions were announced to meet the rise in demand from growth in the construction sector.

Three years later, stronger end-use consumption has been slow to materialize, and President Trump’s rapid changes to tariffs and trade policy have muddied the economic outlook. Revisions to Section 232 have leveled the playing field in terms of imports, and some countries that were only occasionally present in the US market are starting to gain market share.

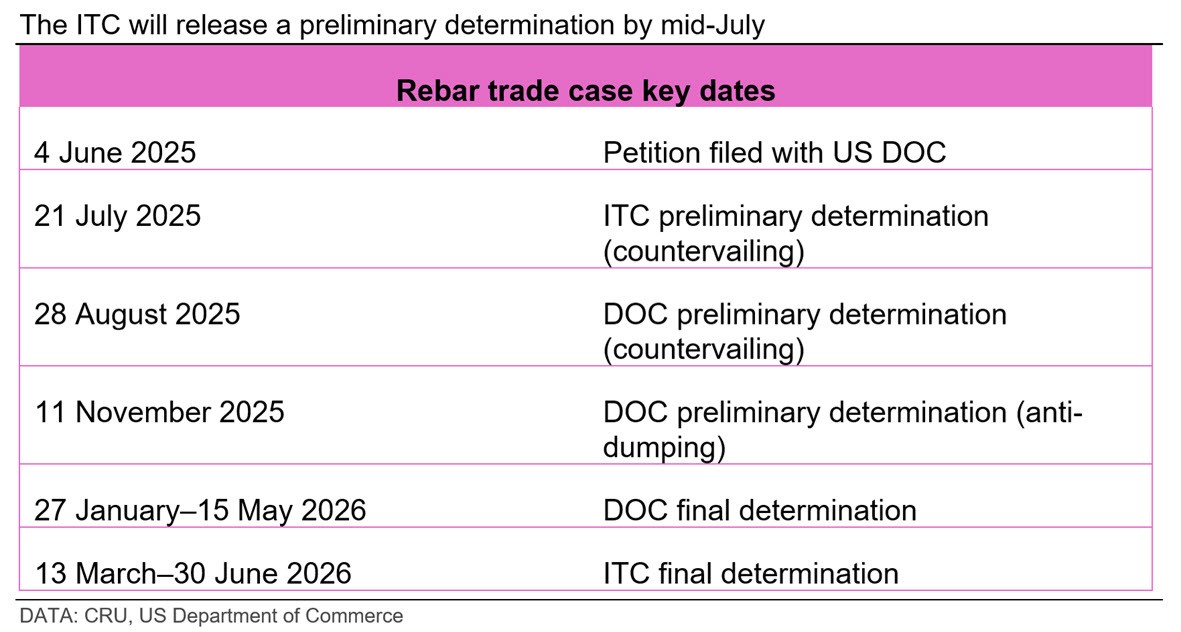

Domestic producers have taken notice. On June 4, the Rebar Trade Action Coalition submitted a petition with the International Trade Commission (ITC) to initiate anti-dumping duties on rebar from Algeria, Bulgaria, Egypt, and Vietnam.

This comes at the same time that several of the previously announced greenfield projects and mill expansions are ramping up. The additional capacity will effectively displace a portion of imports. However, the US is and will remain a net importer of long products. This begs the question: Will this trade case have a meaningful impact?

This insight will explore developments in domestic production, the dynamics of the US rebar market, and changes in trade as a result of tariffs. Considering these factors together should bring clarity on how important this trade case is to the US rebar market.

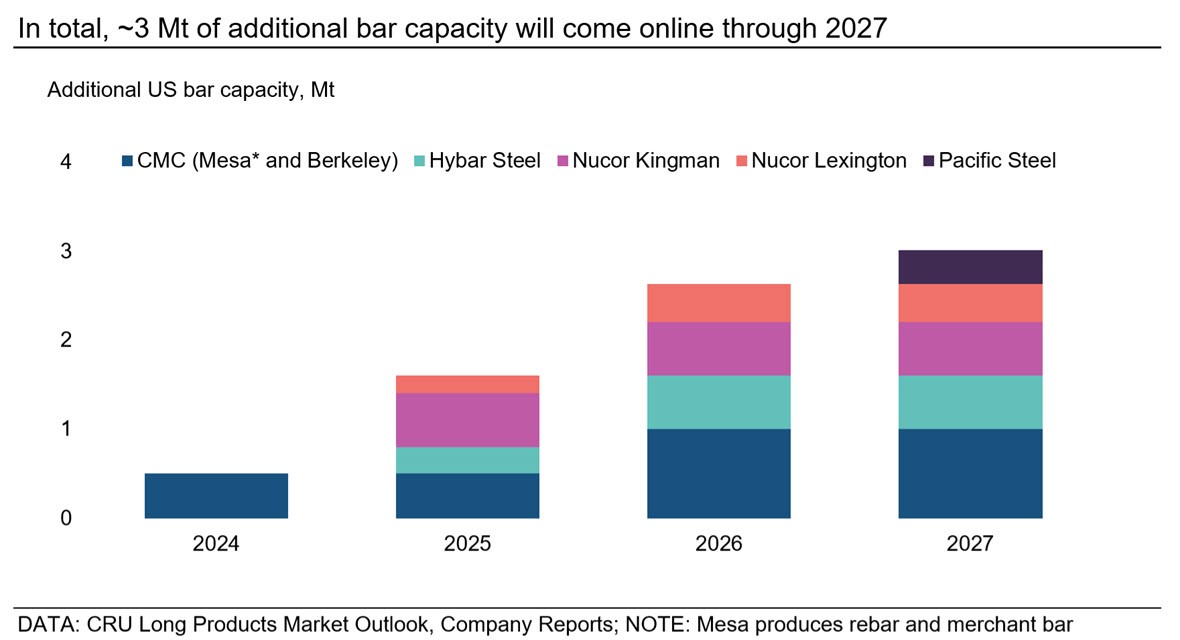

The US will add 2 million mt of rebar production over the next few years

In 2022, expectations of rising demand, along with the prospect of higher sustained prices due to lagging production, prompted numerous announcements of greenfield rebar projects, as well as capacity expansions. In all, nearly 6 million metric tons (mt) of rebar production was proposed to come online through 2027.

The first of these to reach completion was CMC’s Arizona 2 mill in Mesa, Ariz., which started in 2024 and can produce 500,000 mt per year of bar products. In 2025, more than 1.5 million mt of added capacity is set to ramp up from new players and incumbents.

Steel industry veteran David Stickler’s newest investment, Hybar, rolled its first rebar in early June at its plant in Osceola, Ark. In addition to using 100% scrap feedstock, the plant implements a direct connection to a solar installation and battery storage, meaning it can run fully on renewable solar power. These innovations have allowed Hybar to obtain Climate Bond certification, and they strive to eventually secure LEED (Leadership in Energy and Environmental Design) certification, an endeavor that Stickler achieved during his time at Big River Steel.

Nucor is expanding capacity in 2025 as well. It added a melt shop to its Kingman, Ariz., bar mill, which it expects will produce 600,000 mt per year, in addition to a 500,000 mt per year micro mill in Lexington, N.C. Both of these projects are ramping up now and anticipated to be operational sometime in Q3’25.

Looking ahead, CMC is also building a micro mill in Berkeley, W.Va., which is expected to start in H1’26 and produce 500,000 mt per year of rebar. Pacific Steel has a 380,000-mt-per-year micro mill in California slated for 2027. Several other new players in the US market also pledged to add 1.7 million mt per year of production but have not announced target dates.

Rising demand means the US will still require imports

While CRU’s economic outlook for 2025 has cooled, the years ahead will bring some recovery for finished steel consumption. Construction activity will rebound as projects already funded through the IIJA continue to support infrastructure spending. Manufacturing should see a bump from steel mills being built, as well as investments in reshoring across various sectors. The shift toward AI supports continued data center construction, too, further bolstering non-residential construction activity.

As demand grows, even with new domestic capacity, the US will remain a net importer of rebar. Historically, most US rebar imports have come from Mexico, Turkey, and, in part, Algeria. Mexico’s share of imports has been cut in half since 2020, and low-cost producers like Egypt have taken their place.

Global oversupply remains a risk for the US market

Even as demand has continued to rise over the last decade, expansions in domestic production lagged. Consequently, US rebar imports ballooned to 1.6 million mt in 2016, up more than 450% from the 2011–13 average of ~289,000 t. This resulted in ~1 million mt of bar capacity added to the US market through 2020.

Global capacity has also continued to rise. The latest edition of CRU’s Steel Long Products Market Outlook forecasts that world ex. China production will grow ~6% over the next five years.

Cost-competitive producers in Africa and Southeast Asia will add more than 8.5 million mt of capacity during this time, though demand in those regions grows at a slower pace. Even with tariffs and duties, the overall lower costs for these producers make them a viable option for net importing countries like the US.

Section 232 brings support but is not a long-term solution

The revision of Section 232 to include material from Canada and Mexico has stemmed imports from those regions but also allowed opportunities for others to gain market share. While raising the tariff rate from 25% to 50% will support the US market, effects are generally short-lived after the initial shock.

Negotiations on reciprocal tariffs are ongoing and increasing the Section 232 rate should help move along discussions. As deals are reached, it’s likely we see a drop back to 25% on Section 232 or even some exemptions, letting steam out of the upward pressure on prices. Therefore, any longer-lasting solution to curb imports will come in the form of anti-dumping or countervailing duties.

Ultimately, the case could mitigate risk for upcoming capacity

After the US Department of Commerce decides whether or not to initiate the case, the ITC preliminary determination is scheduled for mid-July. If approved, trade flows could shift again to re-include more traditional trade partners, specifically Mexico. Furthermore, it will stem the risk of new mill investments being undercut by oversupply in the global market.

This piece was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

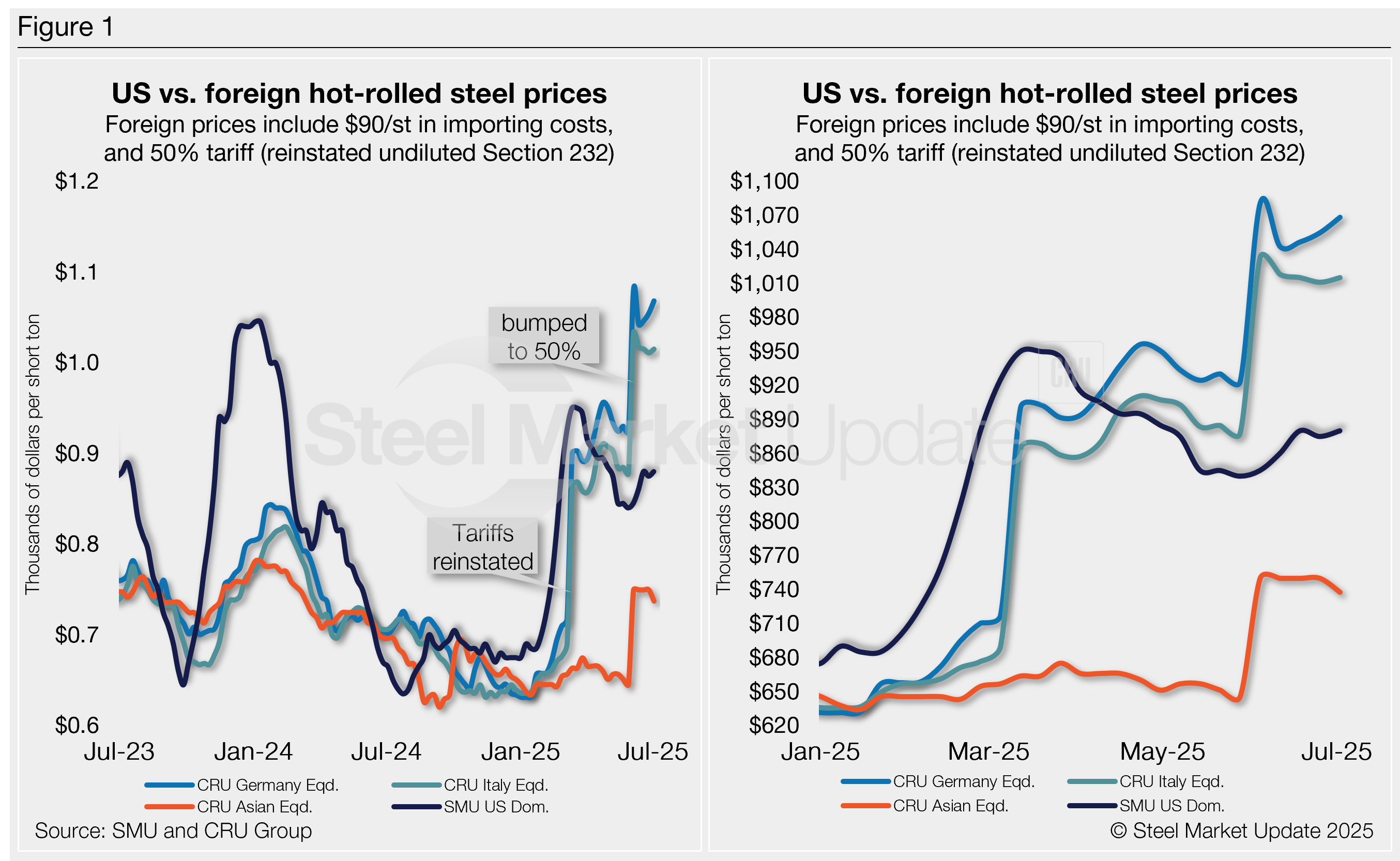

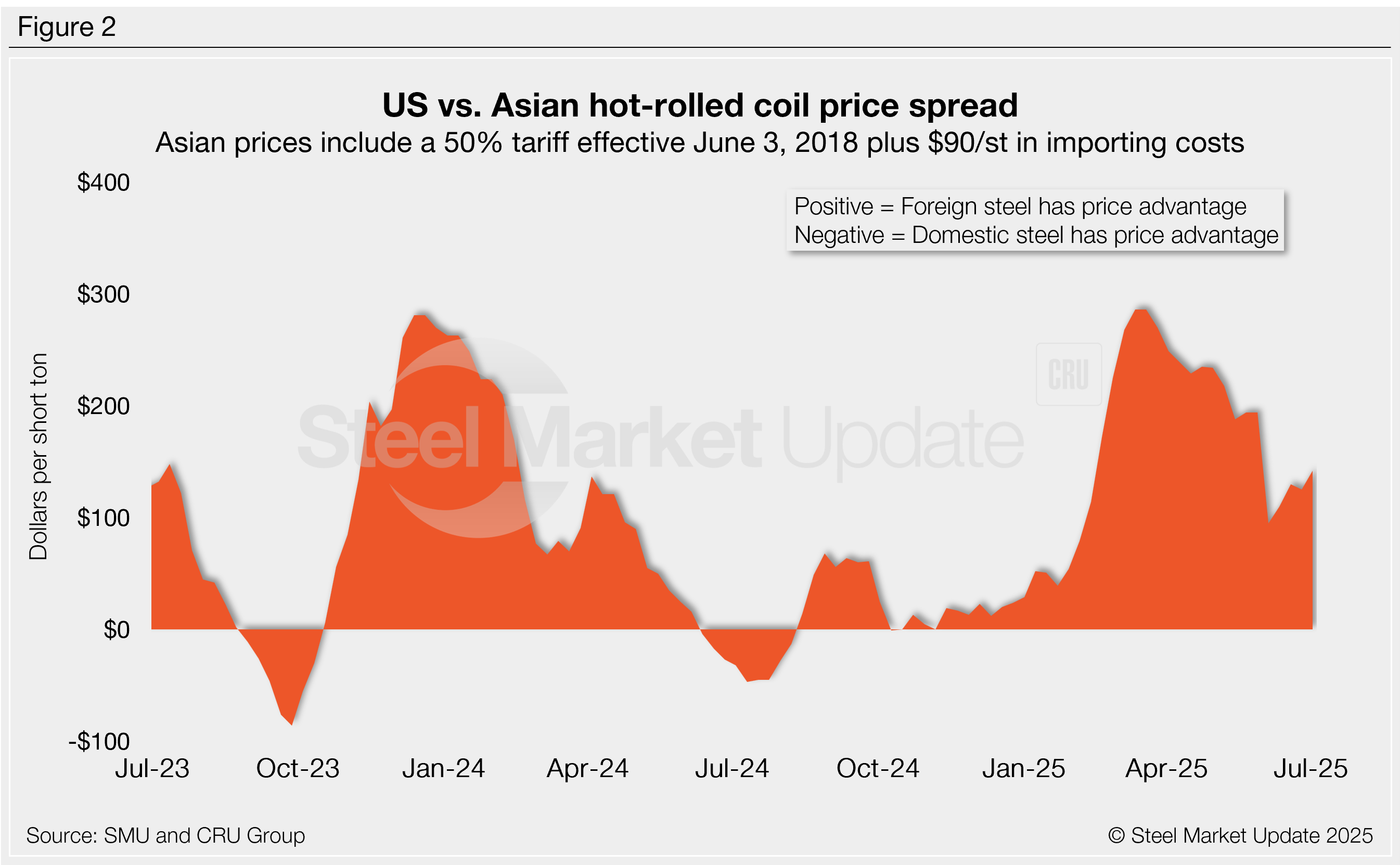

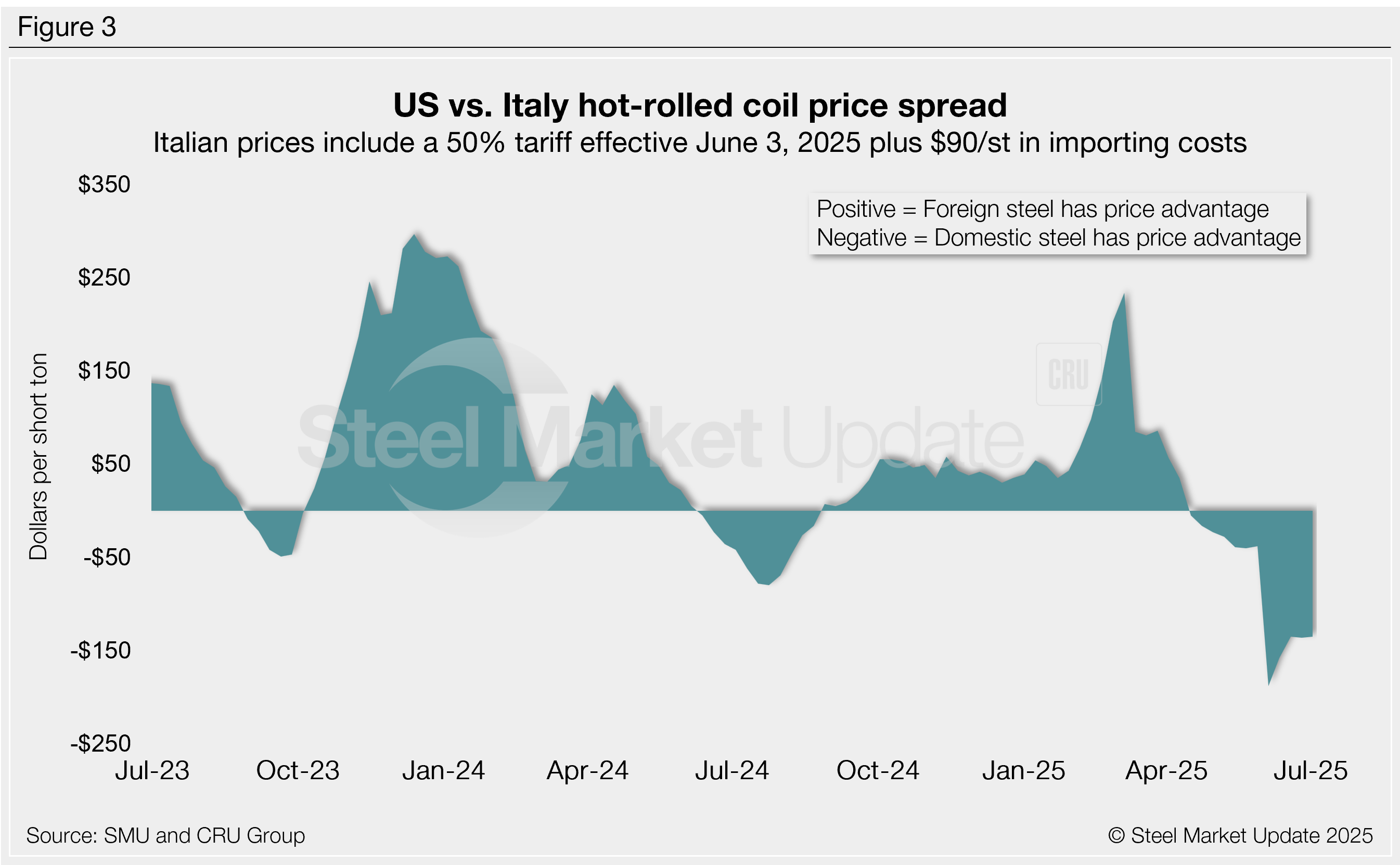

US hot-rolled (HR) coil prices crept up this week but have been largely transacting within a tight band over the past few weeks. Stateside tags continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

Recall the tariff hike to 50% on June 3 reversed earlier gains from March, when reimposed undiluted Section 232 rules had briefly narrowed the price gap with imports on a landed basis.

Prior to March, allies such as Japan and the EU had not been subject to the 25% S232 tariff; instead, they had tariff-rate quotas. The price gap immediately widened again after S232 was stacked (see Figure 1).

By the numbers

SMU’s average domestic HR coil rose $5 this week to $880 per short ton, up $35/st since tariffs were doubled.

Even so, US hot band is now 6.9% cheaper than imports, down from 7.3% last week, but a clear shift from five weeks ago when it was roughly 3% pricier.

If Asian prices weren’t at such a discount to US prices, stateside product would be roughly 18% cheaper than imports. HR from Germany and Italy, on a landed basis, has a massive premium over US hot band.

Today, in dollar-per-ton terms, US product is on average $60 less per short ton than imports. The gap was $64/st less last week and a swing of nearly $90/st before the tariff hike.

The charts below compare HR prices in the US, Germany, Italy, and Asia. The left side highlights prices over the last two years. The right side zooms in to show more recent trends.

Methodology

SMU calculates the theoretical spread between domestic (FOB mill) and foreign (delivered to US ports) HR coil prices. We do this by comparing our weekly US HR assessment to CRU’s weekly HR indices for Germany, Italy, and Southeast Asian ports. This calculation is purely theoretical. Actual import costs can vary significantly and affect the true market spread.

To estimate the CIF price at US ports, we add a $90/st charge to all foreign prices to account for freight, handling, and trader margins, along with the 50% blanket tariff. This $90/st figure serves as a general benchmark — buyers should adjust it based on their specific shipping and handling expenses.

If you import steel and have insights on these costs, we’d love to hear from you. Contact the author at david@steelmarketupdate.com.

Asian HRC (Southeast Asian ports)

As of Wednesday, July 2, the CRU Asian HRC price was $432/st, down $8/st vs. the week prior. Adding a 50% tariff and $90/st in estimated import costs, the delivered price of Asian hot band to the US is ~$738/st. As noted above, the latest SMU US HR price is $880/st on average.

The result: Prices for US-produced HR are theoretically $142/st higher than steel imported from Asia, up $17/st w/w. Despite the added tariff margin, the premium remains well below recent highs seen in 2023 when stateside tags were ~$300 /st more expensive than Asian product.

Italian HRC

Italian HR prices ticked higher by $3/st this week to $617/st, but are about $12/st lower over the past four weeks, according to CRU. After doubling tariffs to 50% and adding $90/st in estimated import costs, the delivered price of Italian HR is, in theory, $1,015/st.

That means domestic HR coil is theoretically $135/st cheaper than imports from Italy. That’s just $1 higher w/w. It still represents a $369/st swing before S232 was reinstated and then doubled. Without the 50% tariff, US prices in theory would be $173/st above Italian imports.

German HRC

CRU’s German HR price was up $9/st to $652/st this week. After adding a 50% tariff and $90/st in import costs, the delivered price of German HR coil is, in theory, $1,068/st.

The result: Domestic HR is theoretically $188/st cheaper than HR imported from Germany, a $8/st cut vs. last week.

US hot band held a $207/st premium over German HR just about three months ago, which had represented the widest margin in 14 months. Without the 50% tariff, US prices would be $138/st above German imports in theory.

Editor’s note

Freight is important when deciding whether to import foreign steel or buy from a domestic mill. Domestic prices are referenced as FOB the producing mill. Foreign prices are CIF, the port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.). Inland freight, from either a domestic mill or from the port, can dramatically impact the competitiveness of both domestic and foreign steel. It’s also important to factor in lead times. In most markets, domestic steel will deliver more quickly than foreign steel. On March 12, 2025, undiluted Section 232 tariffs were reinstated on steel. All steel imports and many derivative products faced a 25% tariff. Effective June 6, 2025, Section 232 tariffs were increased to 50%. Therefore, the German and Italian price comparisons in this analysis now include a 50% tariff. We do not include any antidumping (AD) or countervailing duties (CVD) in this analysis.

SMU regularly polls active players across North America to gauge the pulse of the flat-rolled steel market. We ask about steel prices, end-use demand, inventory levels, policy impacts, business expectations, and current events, among other things.

After a thorough review of SMU’s market survey results this week, what stood out most to me was that most respondents are lamenting weak demand, cautious buying, and so much uncertainty. (Usage of the word was in the double digits!)

I’m no doctor, but I would suggest a dual diagnosis of extreme tariff fatigue and summer doldrums.

You be the judge, though. Below are some of the comments we received this week, straight out of the mouths of North American steel buyers.

How is demand for your products?

“Weak and slowing.”

“Slower than seasonally normal.”

“Doubling of the 25% tariffs is debilitating.”

“No one is out there aggressively spending CapEx dollars, and that is bad for our core business.”

“Very busy after Trump announced the latest round of 232 tariffs, progressively quieter after that announcement.”

“Flattened last week after a month of increases. But we see demand increases being signaled by several customers.”

Are you an active buyer or on the sidelines, and why?

“Active for back-to-back contracts only. No speculation.”

“Active, but only what we need. We have been reducing inventory with sales declining.”

“Active, only to replenish stock sold.”

“Sidelines – Mill and index pricing are not competitive. And we already pre-bought through the third quarter.”

“Sidelines –The exception is tin mill products.”

“Sidelines –We might be in the minority here. But we think prices are about to fall again.”

When do you think sheet prices will peak, and why?

“Already peaked – Demand is very weak. Especially heading into the summer months.”

“Already peaked – Demand is weak, inventories are high, and lead times are short.”

“Already peaked – Uncertainty is keeping predictability and confidence at bay.”

“Already peaked – Hard to believe that pricing will go up in the summertime, which is the slowest time of the year.”

“Already peaked – I think trade deals with Mexico and/or Canada get announced, and this market returns to falling back down. Demand is just too crappy everywhere.”

“July – May have already peaked, but demand is low going into summer doldrums.”

“July – Demand is soft. Price increases are counterintuitive.”

“July – Just does not seem like buyers will let it get much higher.”

“July – Simply based on the cost of imported steel, I expect domestic steel prices to rise a little further.”

“August – Prices will increase if no changes in Section 232 tariffs and if true demand starts to increase.”

“August – Still see prices inching upwards until tariff clarity, or Middle East escalation.”

“September – Demand has been suppressed thus far. The back half of the year should recover.”

“September – They will hit a plateau in late Q3 for a while.”

“October or later – Cycles will remain short. But I believe pricing will peak in late September/early October on the back of a moderate scrap/input cost increases and an auto uptick.”

“October or later – Based on demand and supply, I don’t feel we will have much of a peak with prices staying fairly flat until we have economic/tariff clarity.”

“October or later – The full effect of the tariffs and doubling of the 25% has not yet been reflected in the market.”

“October or later – Trump’s going to get it rolling.”

How will your company perform this month compared to your forecast?

“June was better than expected.”

“We will meet in June, but July-August is definitely worrisome.”

“This is our seasonally slow time of year. But we’ve reduced forecast coming into each month this quarter, and we still missed by 5-10% each month.“

“Tariff merry-go-round has everyone being over-cautious and conservative on buying.”

“Demand is solid. But pricing remains under pressure.”

Are you seeing evidence of manufacturing reshoring to the US because of Trump’s tariffs?

“Pricing in the US is higher. Does not make sense to reshore.”

“I’m hearing more and more about it, but not yet seeing it in my customer base.”

“Limited instances, but reshoring is happening – just not sure it’s enough to move the needle.”

“Yes, but only on a small scale.”

“Yes, autos, appliance, pipe & tube in particular.”

“It takes a lot of time, and Trump’s uncertainty factor and interest rates still need to go down.”

“A little. But many products have no plants to re-open. They have to be built, which takes years, not months.“

Are President Trump’s tariff policies helping your business? Why or why not?

“I’m not sure. At times yes, other times no.”

“I’m not sure. Too much up and down. Nobody knows what is tariffed and what isn’t.”

“No. Causing uncertainty in market, contributing to slow demand.”

“No. Too much chaos.”

“No. Too unstable.”

“No. The continuous changes are causing too much uncertainty and reducing end-product demand.”

“No. Any semblance of consumer confidence is gone.”

“No. Pushing steel pricing up when demand is low, affecting margins.”

“No. There is a level of reliance on import availability.”

“No. They are hurting our business and driving up costs for manufacturers.”

“Yes. Helped in the short term, jury is still out on the long term. But early future indicators appear to be positive.”

“No. Hurting it and the general economy, which will just start to truly be felt in the next 30-45 days as consumers get sticker shock!”

“I’m not sure. Cannot be sure of anything with Trump.”

*

Thank you to all who took part in this week’s survey! If you don’t already participate but find value in our survey results and Market Chatter articles, others will find value in hearing your thoughts as well! Contact david@steelmarketupdate.com for more information about being included in our market questionnaires and sharing your thoughts with the SMU community.

Steel sheet buyers report feeling bogged down by the ongoing stresses of stagnant demand, news fatigue, tariff negotiations or implementation timelines, and persistent macroeconomic uncertainty.

Nucor’s $10 increase on hot-rolled coil brought its spot price to $910/st this week, but did little to bolster buyer hopes. Raising prices amidst an adequately stocked market nagged at buyers.

One Midwestern-based distributor said Nucor’s increase added to the general sense of uncertainty that buyers are exhausted by.

“Shops are dead. Jobs are dead. Demand is dead. There is a lot of pessimism right now in general. Selling prices remain stagnant. Ample supply without demand to back it up is just more noise,” said the distributor.

A second Midwestern distributor underscored the lack of movement in the market.

“There haven’t been any large price changes and most people are out on vacation this week. That pulls the activity down a bit,” he said.

A service center operator on the East Coast surmises that mill prices are aligned with their orders.

“Business remains slow and steady,” he commented. “My prediction stands: nothing will change until Q4. The market remains slow and mill published prices reflect their order books.”

On the other side of the Rocky Mountains, market sentiment was similar.

A West Coast-based distributor does not expect to see the market gain more confidence until the overall macro-conditions firm up.

“[The] market is still slow, especially this short holiday week. I’m of the opinion that we won’t see a change until the tariffs are decided. Deadline is July 9, and we’ll see if Trump kicks them down the road further and whether they are implemented,” said the distributor.

They added, “Negotiations may take longer than he [Trump] originally thought. When tariffs are complete, I think we’ll be in a better position with trading partners.”

SMU assessed the current spot price for domestically produced HR coil at $840-920/st, with an average $880/st, as of Tuesday, July 1.

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through June 30.

Steel prices continued to tick lower throughout June, though the rate of declines slowed halfway through the month. Overall, sheet and plate prices fell $48-$78 per short ton (st) across June.

SMU’s Price Momentum Indicator varied throughout the month. Moving from Lower to Neutral at the start of the month for both sheet and plate products, before shifting to Higher and then back to Neutral to close out June. The shifts came from a mill pricing blitz that saw some early response, before fizzling out due to poor underlying demand.

Steel scrap prices were flat from May to June due to flat-to-soft demand, ample supply, and sluggish exports. Early expectations for July point to a sideways or slightly weaker scrap market, with new import tariffs expected to have an impact.

Our Steel Buyers’ Sentiment Indices varied in early June, with Current Sentiment reaching a near five-year low and Future Sentiment recovering marginally after falling to a multi-year low. Both edged up to close out the month. Both Indices continue to reflect optimism among steel buyers regarding their companies’ chances of current and future success, although not as strongly as they did back in midway through Q1.

Mill lead times continued to shorten throughout June, with some production times falling to lows not seen in years. As of last week, the average lead time for hot-rolled steel was just over four weeks, cold-rolled and coated products around six weeks, and plate at just over five weeks. Most buyers expect lead times to be steady to down going into summer, citing softening demand and rising supply.

The percentage of buyers reporting that mills are willing to negotiate new spot order pricing slipped at the onset of June as mills tried to push prices higher backed by another round of “tariff-roulette,” sliding from almost 95% to about 60%. But nearly 85% of buyers in our late-June survey reported mills were flexible on price. Tariffs continue to have a recurring impact on prices, though mills might not have felt the upper hand in negotiations as they did earlier in Q1.

The Global Steel Climate Council (GSCC) has certified a total of eight hot-rolled (HR) steel products from Steel Dynamics Inc. (SDI) and Arkansas Steel Associates (ASA).

The move shows an expansion from GSCC’s company-wide level certification to targeting product-level certification under its Steel Climate Standard.

Fort Wayne, Ind.-based SDI received certification for HR steel products from each of its seven mills.

ASA got certified on a steel railroad OTM (other track material), one of its core offerings.

“This recognition underscores our unwavering commitment to sustainable steelmaking and our dedication to reducing emissions,” SDI Chairman and CEO Mark D. Millett said in statement on Tuesday.

Likewise, Hiro Kado, ASA president and CEO, applauded the achievement.

“We are proud to lead the industry in producing climate-aligned steel products that meet the rigorous standards set by the GSCC,” Kado said.

Newport, Ark.-based ASA is a joint venture between Yamato Kogyo and Sumitomo Corp. It specializes in making steel railroad tie plates.

The products were evaluated through a third-party verification process.

GSCC’s Steel Climate Standard is described as “a globally applicable, technology-neutral framework based on science-based targets and transparent reporting.”

The group is a non-profit organization dedicated to reducing steel emissions by creating science-based global standards.

For the statement and full list of certified products, click here.

Ferrous scrap export activity has picked up since our last update earlier this month.

Previously, we reported a dearth in US-origin bulk cargoes for shipment to Turkey or other Mediterranean destinations. This has changed.

Over the last week, there have been five cargoes sold to Turkey from the US East Coast/US Gulf Coast. All the exporters basically received the same price of $345 per metric ton (mt) CFR for HMS 80/20. The component of shredded scrap garnered $365.

The Europeans were also active with numerous cargoes sold at prices ranging from $336-42 per mt CFR for HMS 80/20.

It is unclear at this time whether this buying trend will continue. The rebar market in Turkey still has not gained very much traction. Also, billets from China and Southeast Asia are still fairly cheap. So, one would think, this market is rangebound and shows life only when Turkey has to restock.

Some of the increased pricing of US cargoes has been eaten up by increased freight. However, the worst seemed to be over. SMU spoke with an export executive who told us freight dropped significantly last week. He said freights were down $6-7 per mt, “less than $35 for sure. More downside is expected over the next week to 10 days.”

The US domestic market is starting to show some firmness going into July and could improve in August. It would seem that export prices would have to get better to draw more scrap from the US. Either that or freight rates would have to continue to drop. Maybe both.

Before we get ahead of ourselves, the tariff picture still needs fine tuning. The reciprocal tariff suspension will expire on July 8 and it is not at all certain what the effect on the ferrous markets will be, to say the least.

Cascade Die Casting (CDC) plans to expand at the company’s High Point, North Carolina operation.

The company is investing $8 million into its “Atlantic Division”, comprised of a couple of facilities, with additional support from the local City of High Point and Guilford County to boost infrastructure capacity.

CDC Atlantic already houses 13 die-casting machines (ranging from 900 to 1,600 tons), three on-site furnaces, and shot blasting capabilities.

In 2021, it melted more than 10 million pounds of aluminum – over 4,500 metric tons – even during a period marked by supply chain bottlenecks and a subdued automotive market.

That level of output drawn from a likely underutilized year, signals that the nameplate capacity could be even higher.

Adding notches to a manufacturing belt

CDC’s High Point plant is well-placed within a North Carolina industrial pocket.

Daimler North America’s Thomas Built Buses’ manufacturing site is just down the road, and other key Daimler subsidiaries – including a Gastonia Components operation and Freightliner’s largest manufacturing plant – are within reach as well.

Caterpillar has nearby plants in Winston-Salem, Clayton, and Sanford. And GKN’s automotive footprint is within a couple of hours of CDC Atlantic.

In short, Cascade is in the right operating radius, even if the hub’s stated purpose is to serve the southeastern US and Mexico.

Where A380 and A413 fit

CDC Atlantic casts A380 and A413 secondary alloys, both die-cast grades synonymous with the automotive market.

No alloy is more emblematic of the secondary casting market than A380, while A413, by contrast, serves a more niche role, commonly used in cylinder head and piston production as well as other high-pressure hydraulic applications.

US A380 output topped 200,000 metric tons in 2024, according to the US Geological Survey, compared to A413 which fell under a broader category of secondary die-cast alloys representing about 13% of die-cast production over the same period.

CDC’s implied melting capacity would place it close to 1.5%-2.0% of national die-cast production, excluding sand and permanent mold processes, with output trending toward the upper end of that range. While 2% may sound modest, when spread across more than 225 casting sites in the US, it’s a meaningful slice – especially considering the figure is likely a conservative estimate, with actual throughput potentially exceeding those totals.

Cascade’s bet on High Point reinforces the trend that scrap-fed die-castings are still a prevalent part of automotive aluminum, despite recurring bottlenecks and muted production levels. The High Point facility, in particular, is also positioned within a manufacturing corridor dense with OEMs that service the commercial vehicle sector – arguably the segment where light-weighting remains a top design priority.

This piece was first published by SMU’s sister publication, Aluminum Market Update. To learn about AMU, visit their website, or sign up for a free trial.

People who’ve participated in our surveys or who read our newsletters are familiar with a question we ask regularly: What’s going on in the market that nobody is talking about?

For the last 2-3 years, there have been two recurring questions from our readers: What’s the latest on the U.S. Steel sale? And who might buy Evraz North America (NA)?

We all know the answer to the first question now. Nippon Steel closed its “partnership” with U.S. Steel earlier this month.

The Nippon Steel deal first made headlines in December 2023 (after news that U.S. Steel was for sale burst into public in August 2023). Then it was a waiting game. Court cases, multiple government reviews, even a “Golden Share.” The transaction had it all.

We’ve gone through an action-packed roller coaster ride. But even if it’s hard to remember now, there were long stretches when nothing happened. At least not that we saw. So it makes sense that people were curious all along as to how the whole thing would play out.

The sale of Evraz NA has been a much quieter affair. Not much was said, at least not publicly. And not much happened, at least not publicly. Then the story came back onto our radar when private equity firm Atlas Holdings announced late last week that it was buying Evraz NA.

Evraz NA has been on the market since August 2022, in the wake of Russia’s invasion of Ukraine in February of that year. (Michael Cowden’s article on it here has further details.)

But again, since that time, we’ve had little in the way of updates. And then, as tends to happen, Friday afternoon or the weekend rolls around, and all the big news spills over the wires.

At least that is how it’s felt since “Liberation Day” and the ever-changing tariff landscape since then. That said, news breaking on weekends isn’t entirely a Trump 2.0 phenomenon. After all, the news that Cliffs wanted to buy U.S. Steel broke on Aug. 13, 2023 – a Sunday. And news that the Biden administration would reduce tariffs on US allies broke on Oct. 31, 2021 – a Sunday, and Halloween too.

Where do we go from here?

It’s not like we have exactly closed the book on these two deals. (Who knows, there could be more curveballs in store for us.) And I wouldn’t be surprised if we continue to see news break on Fridays, weekends, and holidays. But significant chapters have been turned.

Ultimately, I think what these two deals highlight is a new era of trade. Notice I didn’t add in the word “free” there.

Geopolitical squabbles are complicating the idea of a “global village.” And it looks like governments could have a bigger role to play in business, especially in the steel industry. Steel tariffs don’t just rise from 25% to 50% on their own. You can’t shrug it off as just some wonky stuff that happens in Washington, D.C.

What’s something that could happen on an “average” day in 2025? Well, we’ve seen the aforementioned doubling of tariffs, reciprocal tariffs, pauses on tariffs, pauses on negotiations with a neighbor like Canada, and then things resume again.

Shipping is another issue. Whether it’s potential Mideast conflicts leading to closed shipping lanes or levies on Chinese-flagged vessels, what you pay today to get your steel on a boat could be vastly different tomorrow.

And then we’ve seen two recent examples of reshoring. Appliance makers Whirlpool and GE Appliances have both announced an increased focus on US operations. Is that just noise, or the start of a meaningful trend?

Out of this chaos, perhaps in a year or two, maybe we’ll look back and think how obvious the outlines of the “new normal” were. Heck, we could even have a new USMCA agreement of some kind by then.

That conjecture brings us back to the original question: What’s going on in the market that nobody is talking about? You first.

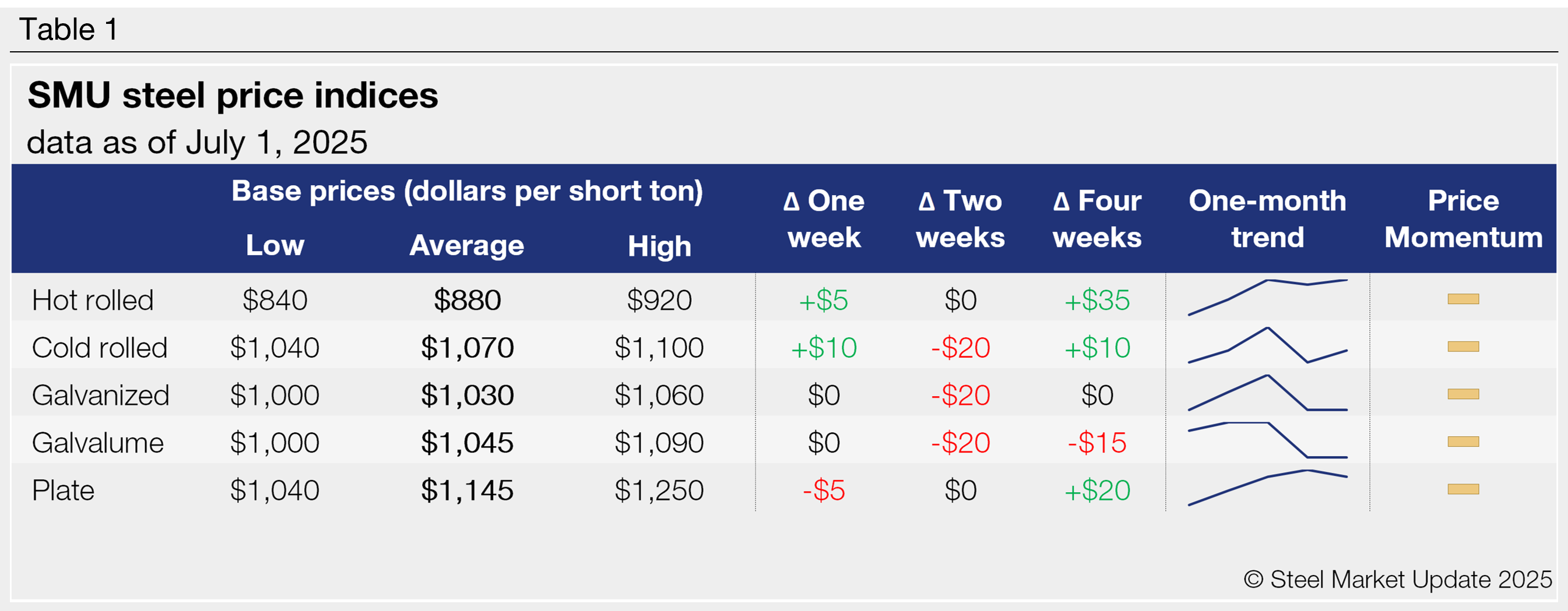

Sheet and plate prices were little changed in the shortened week ahead of Independence Day, according to SMU’s latest check of the market.

SMU’s hot-rolled (HR) coil price inched up $5 per short ton (st) to $880/st on average this week. Prices for other products were also little changed week over week (w/w).

Our cold-rolled (CR) coil price stands at $1,070/st on average, up $10/st vs. last week. Galvanized base prices are unchanged at $1,030/st on average, and Galvalume base prices were flat at $1,045/st. Plate, meanwhile, dipped to $1,145/st on average, off $5/st from last week.

If there was a change, it was that some of our price ranges consolidated in a tighter band compared to prior weeks – with modestly higher lows and somewhat lower highs.

Our price indicators for all sheet and plate products remain at neutral.

What they’re saying

Market participants generally characterized the market as quiet ahead of July 4. And more than a few noted that they were already on vacation.

A producer source said his company has gotten more orders this week without the discounting that pervaded prior weeks. He said it could be a sign that inventories continue to move lower.

A service center source said his company has been buying only as needed as it tries to tune out the noise around emotional issues such as the Big Beautiful Bill, tariffs, and tensions in the Middle East.

Both agreed that volumes were lower than they would be during a non-holiday week.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $840-920/st, averaging $880/st FOB mill, east of the Rockies. The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w. Our price momentum indicator for hot-rolled steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 4.4 weeks as of our June 26 market survey. We will publish updated lead times next Thursday.

Cold-rolled coil

The SMU price range is $1,040–1,100/st, averaging $1,070/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is flat. Our overall average is up $10/st w/w. Our price momentum indicator for cold-rolled has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 4-9 weeks, averaging 6.2 weeks through our latest survey.

Galvanized coil

The SMU price range is $1,000–1,060/st, averaging $1,030/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is down $20/st. Our overall average is flat w/w. Our price momentum indicator for galvanized steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,078–1,138/st, averaging $1,108/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-8 weeks, averaging 6.0 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,000–1,090/st, averaging $1,045/st FOB mill, east of the Rockies. The lower end and the top end of our range flat w/w. Our overall average is unchanged w/w as a result. Our price momentum indicator for Galvalume steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,268–1,358/st, averaging $1,313/st FOB mill, east of the Rockies.

Galvalume lead times range from 4-8 weeks, averaging 6.2 weeks through our latest survey.

Plate

The SMU price range is $1,040–1,250/st, averaging $1,145/st FOB mill. The lower end of our range is flat w/w, while the top end is down $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for plate has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 4-8 weeks, averaging 5.6 weeks through our latest survey.

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

The US Senate on Tuesday passed the tax and budget reconciliation bill extending provisions of the 2017 Tax Cuts and Jobs Act (TCJA) scheduled to expire at the end of 2025.

The Steel Manufacturers Association (SMA) and the American Iron and Steel Institute (AISI) applauded the tax provisions included in the bill.

Steel advocacy support

SMA President Philip Bell said the group is encouraged by the Senate’s progress and noted his apprehension about commenting before the bill is passed by the US House of Representatives.

“We’re very pleased that the Senate has moved forward with the tax bill. And we think the tax bill, when coupled with revitalized 232 tariffs, are probably the two most powerful things the administration can do for the domestic steel industry,” he said.

Bell went on to pinpoint the benefits of the tax policy for steelmakers.

“There are three really important components we like. First, immediate expensing of research and development (R&D) investments. That is absolutely critical. As is, immediate expensing of capital equipment. In an industry with large-scale equipment, it’s very capital-dependent. Finally, what we really like is the facility expensing piece of the bill,” he said.

Bell noted that several projects have been moving forward, but freeing capital through the new tax changes expedites ramp-up time for facilities. And that means employing workers faster.

On the topic of workers, Bell called attention to the overtime exemption in the bill. “The icing on the cake is the overtime exemption. This will help our workers have more money in their pockets to take care of their families and to support the communities where they live,” he said.

The overtime exemption is a temporary measure added to the bill. For workers who earn less than $160,000 per year, overtime wages are exempt from federal taxes. The clause is applicable from 2025 through 2028.

Kevin Dempsey, president and chief executive of AISI, also lauded the restoration of tax provisions.

“We applaud Senate passage of this legislation, which will permanently restore key provisions that have a proven record of fueling innovation and economic growth, including 100 percent bonus depreciation for business investment, immediate expensing for domestic research and development expenses, and the EBITDA-based limitation on business net interest deductions,” Dempsey said.

“Capital investment is crucial for economic growth and job creation in the American steel industry and the manufacturing sector as a whole. Many of the key capital cost recovery provisions of the 2017 tax law have expired or are being phased out. Restoring these provisions is essential to ensuring that many companies will be able to make new investments in steel-intensive facilities and machinery,” he added.

The Congressional Budget Office states that the bill will “increase the deficit by nearly $3.5 trillion over the 2025–2034 period relative to the amount in the January 2025 baseline.”

Mining industry support

The bill includes a subsidy for met coal used in steel production.

A statement from the National Mining Association CEO, Rich Nolan, emphasized the group’s interest in supporting the domestic industry. He sees the bill as freeing the industry from constraints that limit the US’s ability to compete in the global economy.

“Through these measures, the bill will directly support US economic growth and security. Mining feeds and fuels virtually every American supply chain; a strong mining industry creates an equally strong foundation for every industry that depends on the products and energy we provide. More can be done, and the NMA will continue to advocate with Congress and the administration on ways to support additional domestic mining, and mineral production and processing,” Nolan said.

Canada has implemented tariff-rate quotas (TRQs) on steel imports to help protect and stabilize its domestic market.

Notably, they do not apply to countries that have a free trade agreement (FTA) with Canada. Thus, this exempts 52 countries, including the US and Mexico.

Also notable is that any unfilled quota remaining at the end of a quarter will be rolled over into the next, according to the Department of Finance Canada.

The product categories and quarterly quota volumes are shown below.

Product

Quarterly quota (metric tons)

Maximum share of total quota per country

Flats

186,856

36%

Longs

178,512

28%

Pipe and tube

117,406

47%

Semi-finished

152,383

72%

Stainless

5,568

91%

Any imports above the quota levels will be subject to a 50% surtax.

“This measure will help stabilize the Canadian market and prevent harmful diversion of foreign steel from third countries into Canada while minimizing impacts on Canadian importers and downstream users,” according to Finance Canada.

The Canadian government will review the quotas “in 30 days to ensure their appropriateness and effectiveness in light of evolving market circumstances, and periodically thereafter.”

Canadian industry anticipates little help from TRQs

The Canadian steel industry doesn’t see the TRQs as doing much to help what it sees as a dire situation.

Catherine Cobden, president and CEO of the Canadian Steel Producers Association (CSPA), believes a tariff-rate quota will still allow high levels of steel imports to enter the country duty-free.

She put it bluntly: “In its current form, the TRQ will do little to support our industry.”

The United Steelworkers (USW) union in Canada agrees.

“The tariff-rate quota is too narrow. It locks in high levels of dumped steel and doesn’t cover some of the worst offenders,” said USW National Director Marty Warren.

As is, the TRQ system “leaves out two-thirds of imports to Canada, including from countries like South Korea and Vietnam, with whom Canada has a free trade agreement, despite repeated dumping violations,” USW added.

CSPA has warned that there could be a huge fallout from the tariff war, with thousands of job losses across the Canadian steel industry.

The union said it will continue to press the federal government. Warren stated: “Canadian jobs are on the line – and half measures won’t cut it.”

US-Canada trade talks continue

Canada rescinded a planned digital services tax over the weekend in order to resume trade talks with the US.

Recall that on Friday afternoon, another presidential outburst on social media said the US was terminating trade discussions due to the levy.

On Sunday, in response, Canada’s government announced it would rescind the tax “in anticipation of a mutually beneficial comprehensive trade agreement with the United States.”

“Canada’s new government is engaged in complex negotiations on a new economic and security partnership with the United States,” the government said to explain the reversal.

Leaders of the two countries agreed to resume negotiations “with a view towards agreeing on a deal by July 21,” the Canadian government said.

The owner of Liberty Steel Industries and his family were among the six victims of a plane crash in Ohio on Sunday.

Authorities identified the bodies of James ‘Jim’ Weller, 67, president and CEO of Liberty Steel Industries Inc.; his wife, Veronica, 68; their son John, 36; and daughter-in-law Maria, 34, according to The Vindicatorin Youngstown.

The pilot, Joseph Maxin, 63, and co-pilot, Timothy Blake, 55, also died when the twin-engine Cessna 441 Conquest went down about seven minutes after takeoff from Youngstown Regional Airport just before 7 a.m. Sunday.

The National Transportation Safety Board is investigating the incident, The Vindicator reported.

The family was traveling to Bozeman, Mont.

Warren, Ohio-based Liberty Steel processes hot-rolled, cold-rolled, and coated flat-rolled steel in addition to providing stamping and blanking services.

It has facilities in Lordstown and Warren, Ohio, as well as in Saltillo, Mexico. Its customer base spans North America, Mexico, and Brazil, according to its website.

Weller’s father, James Weller Sr., founded the steel service center in 1965.

US manufacturing activity slowed for a fourth straight month in June. That’s a sharp shift after trending up for most of Q1, according to supply executives contributing to the Institute for Supply Management (ISM)’s latest report.

The ISM Manufacturing PMI (Purchasing Managers Index) stood at 49% in June, up just 0.5 percentage points from 48.5% a month earlier.

A reading higher than 50% indicates the manufacturing economy is growing, while a reading below that shows contraction.

Still, the overall economy continued to expand for the 62nd month since last contracting in April 2020, ISM said. (A Manufacturing PMI higher than 42.3%, over a period of time, usually indicates an expansion of the overall economy.)

“In June, US manufacturing activity slowed its rate of contraction,” ISM Chair Timothy R. Fiore said in a statement on Tuesday.

Demand and output indicators were mixed in June, Fiore added, noting that the “mixed indicators in output suggest companies still being cautious in their hiring even with an increase in production.”

The New Orders Index remained in “contraction territory and edging lower,” registering 46.4% in June vs. 47.6% a month earlier, according to ISM. Fiore also noted that New Export Orders slowed their rate of contraction (46.3% vs. 40.1%).

In June, primary metals was among the nine manufacturing industries that reported growth, while fabricated metal products was among the six manufacturing industries reporting contraction.

Executive comments

A fabricated metals executive highlighted the growing concern and impact of tariffs on domestic manufacturing: “Business has notably slowed in last four to six weeks. Customers do not want to make commitments in the wake of massive tariff uncertainty.”

Cleveland-Cliffs’ previously announced idlings at its Riverdale, Ill., Conshohocken, Pa., and Steelton, Pa., mills have gone into effect.

That’s according to WARN Notices from the affected states and Cliffs’ website.

Recall that in early May the Cleveland-based steelmaker announced the idlings would take place on or around June 30. Insufficient demand and pricing were cited as drivers. At the time, the steelmaker said ~950 jobs would be impacted.

Cliffs declined to provide additional comment on this story. A request for comment from the United Steelworkers union, which represents workers at the facilities, was not returned by time of publication.

Steelton

The Steelton mill, which makes steel rails, was listed in “full idle,” per Cliffs’ website.

A Pennsylvania WARN notice from May said 559 workers were affected. Regarding whether it was listed as closure or layoff, the notice listed it was a “layoff.”

Located near Harrisburg, Pa., the facility also sports an EAF with ladle refining and vacuum degassing facilities, a three-strand continuous jumbo bloom caster, and an ingot-teeming facility.

Cliffs in its first quarter earnings report said that Steelton was idled in part because of import competition from Japanese steelmaker Nippon Steel.

Company Chair, President, and CEO Lourenco Goncalves said during a press conference in early June that Steelton would remain idle despite higher Section 232 tariffs.

Riverdale

The Riverdale operation was also listed in “full idle” on Cliffs’ website.

An Illinois WARN notice from May 2 said layoffs there were because of a “plant closure,” with an effective date of June 30.

Riverdale is a compact strip mill that produces hot-rolled sheet. It is located 14 miles away from Cliffs’ Indiana Harbor Facility in East Chicago, Ind. Riverdale had sourced hot metal from East Chicago via specialized “torpedo” rail cars.

Conshohocken

A Pennsylvania WARN notice from May listed 107 employees affected at the Conshohocken plant, with the closure or layoff category listed as “layoff.”

The effective date listed was June 30.

Conshohocken is a plate finishing facility near Philadelphia.

Radius Recycling Inc.

Third quarter ended May 31

2025

2024

% Change

Net sales

$727.0

$673.9

7.9%

Net earnings (loss)

$(16.4)

$(198.5)

91.7%

Per diluted share

$(0.59)

$(6.97)

91.7%

Nine months ended Feb.28

Net sales

$2,026.0

$1,967.9

3.0%

Net earnings (loss)

$(86.3)

$(250.3)

65.5%

Per diluted share

$(3.04)

$(8.82)

65.5%

(in millions of dollars except per share)

Radius Recycling on Tuesday reported a narrower loss in its most recent quarterly earnings report. Stronger steel demand, rising scrap flows, and improved rolling mill utilization drove sequential gains. Additionally, the company said solid construction activity and firm nonferrous pricing helped offset lingering macroeconomic uncertainty.

The Portland, Ore.-based metals recycler and long steel producer reported a net loss of $16 million in its fiscal third quarter ended May 31. Although still in the red, this was a marked improvement from the $33 million loss in the prior quarter and the $199 million loss in the same quarter last year.

Revenues rose to $727 million, up from the previous quarter’s $643 million and Q3 last year’s $674 million.

Recycling results

Driven by seasonal improvements in supply flows, ferrous sales volumes climbed 4% quarter over quarter and 2% year over year to 1.14 million long tons.

While domestic demand and pricing ticked higher in March due to mill restocking, the company noted that “prices decreased significantly in the remainder of the quarter on macroeconomic uncertainty.”