Steel market chatter this week

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

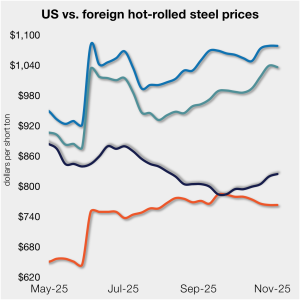

The gap between US hot band prices and imports narrowed slightly. But with the 50% Section 232 tariffs, most imports remain more expensive than domestic material.

U.S. Steel has unveiled more details of a multi-year growth plan in partnership with Nippon Steel.

Shipments from US steel mills were strong in September, according to the latest figures provided by the American Iron and Steel Institute (AISI).

Most sheet prices inched up again this week following mill efforts to set a floor under tags and to increase them from there.

The United Steelworkers (USW) union has voted down a tentative agreement with Metallus. The parties will continue the existing labor contract for 90 days, until Jan. 29, 2026, as they continue negotiating.

SunCoke Energy’s earnings declined in the third quarter as weaker domestic coke sales and contract economics weighed on results.

The volume of raw steel produced by US mills eased last week, according to AISI's latest figures. Prior to this month, output had remained historically strong since June.

Nucor increases HR spot price by $5/ton

With infrastructure demand shifting toward digital capacity, Nucor Corp. is positioning itself as the go-to steel supplier for the data center boom.

The latest Baker Hughes rig count report showed oil and gas drilling slowing in both the US and Canada last week.

SMU’s Steel Buyers’ Sentiment Indices both rose this week, with Current Sentiment rebounding 14 points.

Most steel buyers responding to our market survey this week reported that domestic mills are considerably less willing to talk price on sheet and plate products than they were in recent weeks.

Ternium closed the third quarter with steady shipments and improving margins. But trade policy uncertainty and subdued demand in Mexico weighed on the Latin American steelmaker’s results.

Steel mill lead times marginally extended for both sheet and plate products this week, according to responses from SMU’s latest market survey.

Executives framed the all-stock deal as a path to scale, efficiency, and long-term growth despite ongoing weakness in the metals market.

Sheet steel indices increased across the board this week, while plate prices held steady. All five of SMU’s price indices are higher than they were two weeks ago, and all but one are above levels recorded four weeks ago.

Nucor entered the fourth quarter with clear forward momentum: stronger-than-expected results, solid sheet and plate demand, and construction progress on a major new mill that should add capacity next year.

Nucor has pulled the plug on a planned rebar micro mill in the Pacific Northwest.

Domestic mill production inched higher last week, according to the latest figures released by the American Iron and Steel Institute (AISI). Prior to the start of this month, raw output had remained historically strong since June.

As another month goes by and another futures columnist starts by saying “not much to see here,” I understand that a reader might flip their brain to skim mode.

Demand for plate on the spot market remains soft by comparison to years past. However, this week regional demand variations grew more pronounced.

Our average HR coil price increased $5/short ton from last week, marking a second consecutive week of modest gains. Market participants generally attributed the increase to...

Medium- and heavy-duty trucks (MHDV) and buses imported to the US will start being charged Section 232 tariffs beginning Nov. 1.

SMU’s Steel Buyers’ Sentiment Indices both fell this week, with Current Steel Buyers’ Sentiment notching the lowest reading since May 2020.

Economic growth in some US regions in September was offset by challenges in others, causing the market to appear largely unchanged overall, according to the Federal Reserve’s latest Beige Book report.

Steel mill lead times ticked lower across most sheet and plate products this week, according to responses from SMU’s latest market check.

Mills are more willing to negotiate spot prices for both sheet and plate products, according to our latest market survey results.

SMU’s HR price stands at $800/st on average, up $5/st from last week. The modest gain came as the low end of our range firmed, and despite the high end of our range declining slightly.

The US hot-rolled coil (HRC) market feels steadier as the 4th quarter begins - not strong, but no longer slipping either.