Miller on scrap: Market deals with ferrous scrap dive

As the month of March goes into the second half, the scrap community is trying to cope with the large drop in ferrous scrap earlier this month.

As the month of March goes into the second half, the scrap community is trying to cope with the large drop in ferrous scrap earlier this month.

With Earth Day almost a month away, the world’s attention often turns to the manufacturing sector with calls for greener production processes.

I’ve had questions from some of you lately about how we should think of the spread between hot-rolled (HR) coil prices and those for cold-rolled (CR) and coated product. Let’s assume that mills are intent on holding the line at least at $800 per short ton (st) for HR. The norm for HR-CR/coated spreads had been about $200 per short ton (st). That would suggest CR and coated base prices should be ~$1,000/st. Good luck finding anyone offering that.

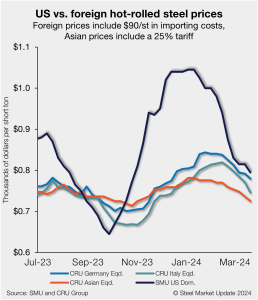

US hot-rolled coil (HRC) remains more expensive than offshore hot band but continues to move closer to parity as prices decline further. The premium domestic product had over imports for roughly five months now remains near parity as tags abroad and stateside inch down.

SMU caught up with Barry Zekelman, executive chairman and CEO of Zekelman Industries, on Wednesday’s Community Chat. As one of the largest independent steel pipe and tube manufacturers in North America, his company is also one of the largest steel buyers in the region. This year alone, the Chicago-based company will buy roughly 2.8 million tons of steel. As such, Zekelman provides a great perspective on the steel industry and the markets it serves.

North American auto assemblies edged down in February vs. the prior month, according to LMC Automotive data. While assemblies did fall month on month (m/m), they are up nearly 3% year on year (y/y).

Varsteel, a Canadian steel and pipe service center, has announced the acquisition of Pacific Steel in Laval, Quebec.

Earlier this week SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market chatter.

US light-vehicle (LV) sales rose to an unadjusted 1.25 million units in February, up 9.6% vs. year-ago levels, the US Bureau of Economic Analysis (BEA) reported. The year-on-year (y/y) growth in domestic LV sales was boosted by a 6% month on month (m/m) gain.

SMU’s price for hot-rolled (HR) inched lower this week. I wouldn’t be surprised, however, if we start to see prices and lead times move higher in the weeks ahead. The modest declines in HR this week are probably the result of lingering deals cut at “old” prices, as sometimes happens after mill price increases. But those deals will probably be out of the market soon if they aren’t already. So why do I float the idea of higher prices? Some big buys have been placed. It reminds me a little of what we saw last fall, when people restocked in anticipation of higher prices once the UAW strike was resolved.

Sheet and plate prices mostly moved lower this week after little change was noted the week prior. Despite edging down, sentiment is mixed, and many suggest a bottom may be near.

As uncertainty swirls around Nippon Steel Corp.’s (NSC) proposed buy of U.S. Steel, the Japanese steelmaker continues to make assurances that it has the best interests in mind for running the iconic Pittsburgh-based steelmaker.

Data on US industrial production, capacity utilization, new orders, and inventories remained overall steady and strong through January and February figures, indicating a healthy manufacturing sector. The strength of the manufacturing economy has a direct bearing on the health of the steel industry.

Domestic production of raw steel moved lower last week, slipping back down after recovering the week prior, according to the most recent data from the American Iron and Steel Institute (AISI).

Eastern Metal Building Products LLC has announced the acquisition of construction products manufacturer Super Stud Building Products.

Volkswagen employees at its assembly plant in Chattanooga, Tenn., have filed a petition with the National Labor Relations Board to become part of the United Auto Workers (UAW) union.

Are we still looking for a bottom on sheet prices? In what direction are steel and scrap prices headed? How’s demand holding up at the moment?

Happy St. Patrick’s Day. “To govern is to choose.” Those words, reportedly first uttered by the late French Premier Pierre Mendes-France in the 1950s, resonate vividly in our time. It means that choices have consequences and that priorities must be set based on goals. Interested parties, in and out of government, raise their voices in […]

The spot rate trend in the flatbeds has seen a positive upturn. There are potential rate accelerators and decelerators, however, likely to influence spot and contract flatbed rates. The flatbed market for spot rates is showing signs of improvement as we move through the new year. February increased slightly from January, marking the third consecutive […]

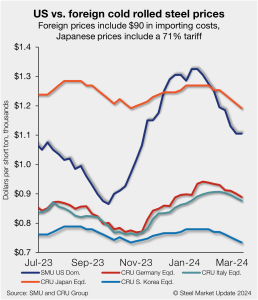

Foreign cold-rolled coil (CR) remains significantly less expensive than domestic product even as US tags continue to decline in a hurry, according to SMU’s latest check of the market.

Rig counts in the US and Canada were mixed this week, according to the latest data from Baker Hughes.

The CRUspi fell by 8.3% month over month (m/m) in March to 206.6 as weaker-than-expected demand weighed on markets around the world. Price falls were notable across all regions, with elevated inventory levels pushing prices in the US and Europe, and disappointing stimulus measures from the Chinese government weighing on those in Asia.

In this Premium analysis we cover North American oil and natural gas prices, drilling rig activity, and crude oil stock levels.

Flat Rolled = 56.6 Shipping Days of Supply Plate = 58.8 Shipping Days of Supply Flat Rolled After weaker-than-expected shipments in January, US service center shipments of flat-rolled steel picked up in February, which caused supply to decrease. At the end of February, service centers carried 56.6 shipping days of flat-rolled steel supply on an […]

SMU’s Current Steel Buyers’ Sentiment Index edged down while the Future Sentiment Index ticked up, according to our most recent survey data

Strength in its flat-rolled steel operations is pushing Steel Dynamics Inc. (SDI) to guide to higher sequential earnings in the current quarter.

According to the latest “Index of Net New Orders of Aluminum Mill Products” released by the US Aluminum Association (AA), total orders in February 2024 were up 9.3% compared to February 2023. This is a noticeable improvement from the growth of 2.1% year over year (y/y) seen in January.

Nippon Steel has reaffirmed the value of its deal for U.S. Steel a day after President Biden issued a statement opposing the sale.

Prices of most steelmaking raw materials have moved lower over the last 30 days, according to Steel Market Update’s latest analysis.

Steel mill lead times were flat to slightly up, according to our market survey this week.