Market Data

March 19, 2024

Manufacturing indicators hold stable since start of year

Written by Brett Linton

Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact Luis Corona at luis.corona@crugroup.com.

Data on US industrial production, capacity utilization, new orders, and inventories remained overall steady and strong through January and February figures, indicating a healthy manufacturing sector. The strength of the manufacturing economy has a direct bearing on the health of the steel industry.

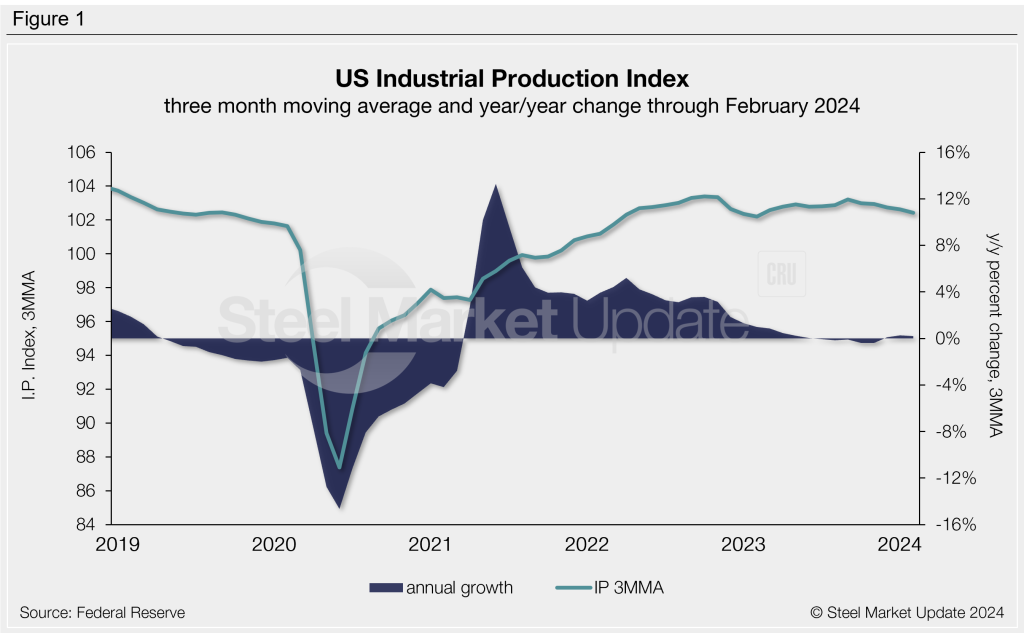

The Industrial Production (IP) Index

The IP Index is a gauge of output from factories, mines, and utilities. Figure 1 shows the IP Index over the last five years, graphed as a three-month moving average (3MMA) to smooth out some of the monthly variability. As a 3MMA, the IP Index has mostly remained strong over the past two years, hovering in the 102-103 range. The latest reading is 102.4 through February, one of the lower levels seen over the past year, but up 0.2% from this time last year.

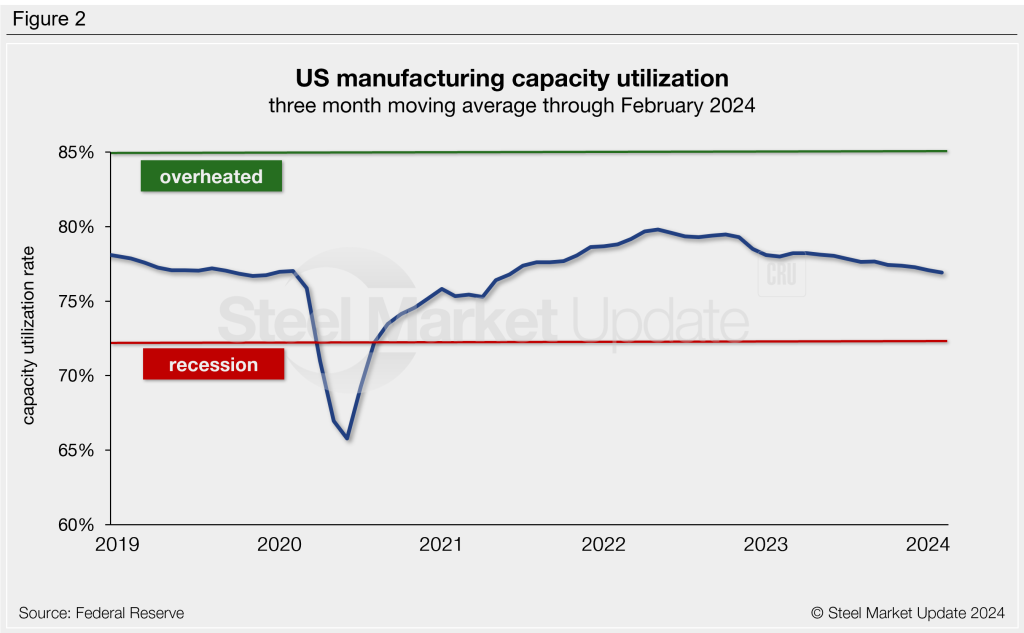

Manufacturing capacity utilization

Manufacturing capacity utilization through February was measured at 77.0% as a 3MMA, now down to a 32-month low. In 2023 we saw an average rate of 77.8%, down from 79.2% in 2022, but up from 77.1% in 2021. Capacity utilization continues to remain above recessionary territory, as it has done since late-2020. For reference, capacity utilization had hovered around 74–78% for most of the 2010s, stalling in April 2020 to reach a low of 66% in June 2020 (Figure 2).

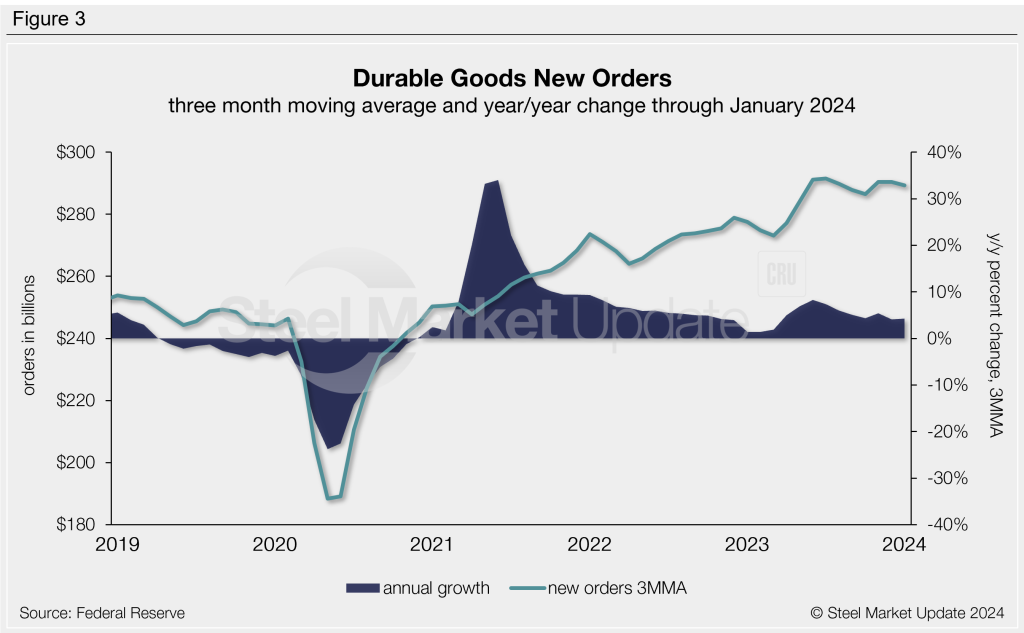

New orders for durable goods

New orders for durable goods are an early indicator of consumer and business demand for US manufactured goods. Levels continue to recover from the 2020 shock, with positive annual growth occurring each month since. As a 3MMA new orders rose to a record-high of $291 billion last June (Figure 3). New orders are at $289.2 billion as a 3MMA through January, up 4.2% annually. Recall the 3MMA had reached a 10-year low of $188.4 billion in May 2020 but returned to normal levels by the end of the year.

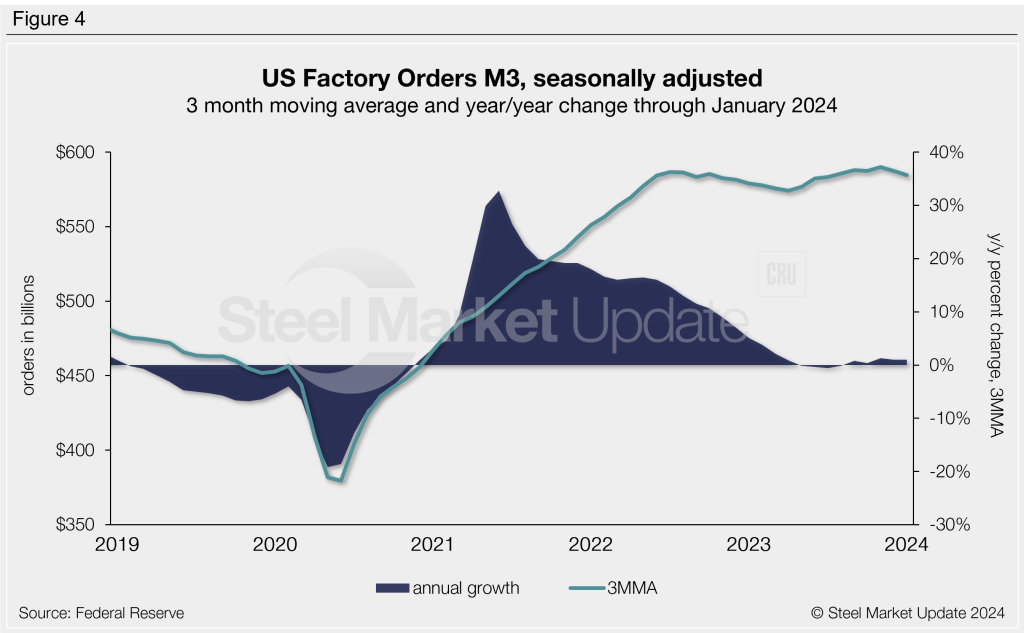

New orders for manufactured products

As reported by the Census Bureau, the growth rate of new orders for manufactured products was historically strong in 2021 and 2022, but stabilized as we entered 2023. Factory orders remain historically high, having reached a 3MMA of $589.9 billion in November, the highest level in our 30-year data history (Figure 4). The 3MMA through January is down slightly to $584.7 billion, up 1.0% compared to levels one year earlier.

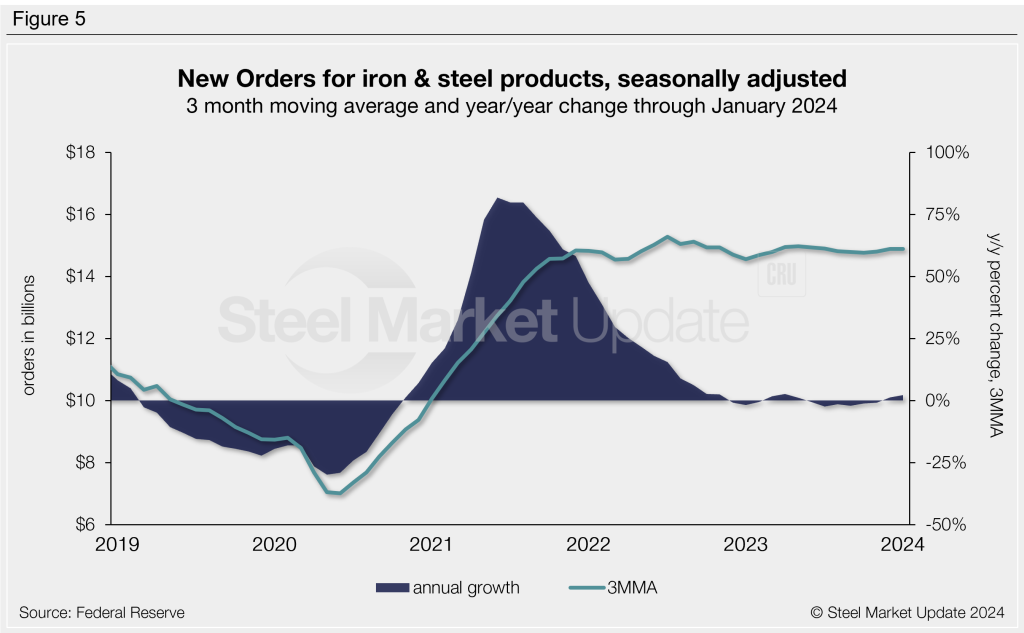

New orders for products manufactured from iron and steel

Within the Census Bureau M3 manufacturing survey is a subsection for iron and steel products. Figure 5 shows the history of new orders for iron and steel products as a 3MMA. The 3MMA new order level remains strong at $14.9 billion through January, a level it has remained in since late-2021. New orders had reached a 30+ year high 3MMA of $15.3 billion in July 2022. The 3MMA year-over-year growth rate through January is 2.2%. This rate has remained near zero since late-2022, having steadily declined from the 11-year high of 81.8% in June 2021.

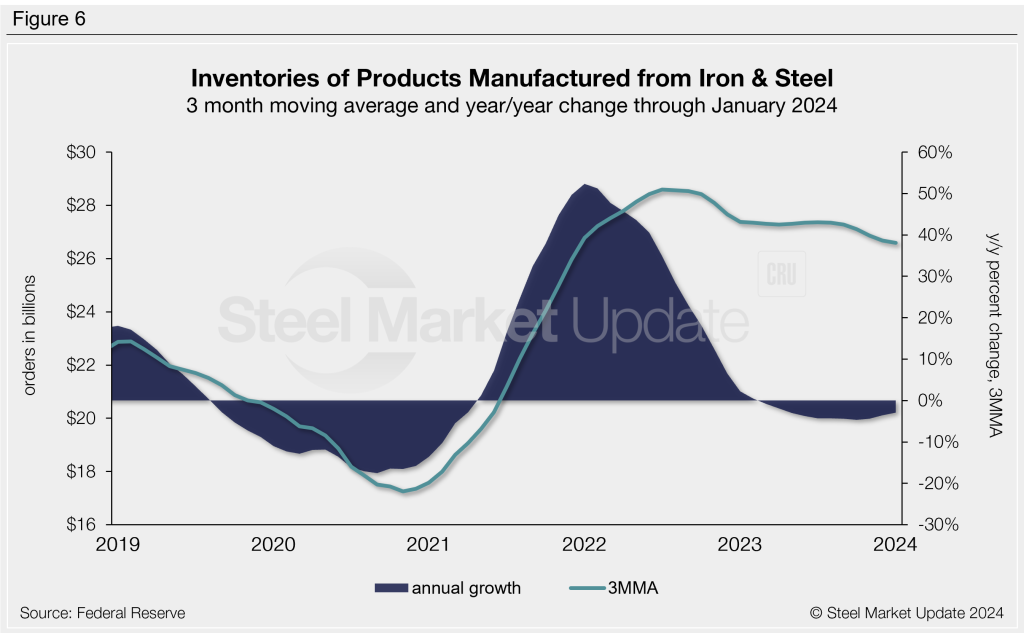

Inventories of products manufactured from iron and steel

Inventories of iron and steel products broke their multi-month increase streak in mid-2022, gradually easing since and now down to a two-year low. The latest iron and steel inventory levels totaled $26.6 billion on a 3MMA basis through January, down 2.9% compared to the same period the year prior (Figure 6).