Product

January 21, 2013

SMU Survey – Stable to Slightly Rising Demand – Trend Developing for Lower Pricing

Written by John Packard

On Tuesday, January 15th, Steel Market Update (SMU) began our second steel survey of the New Year. Our surveys are focused on the flat rolled steel market and are conducted by inviting slightly less than 700 companies who are asked to participate by invitation. Of those participating in last week’s survey 48 percent of the respondents were from manufacturing companies, 37 percent from service center/wholesalers, 6 percent from steel mills, 4 percent each from trading companies and toll processors and 1 percent from suppliers to the steel industry (such as paint or chemical companies).

Total Survey Participation – Stable to Slightly Rising Demand – Trend Developing for Belief in Lower Pricing

SMU asks a number of questions which are aimed at the entire group as a single unit (as opposed to breaking them into market segments). We want to know about Sentiment (which we published in Thursday’s edition of our SMU newsletter), general over-all demand and price direction.

General demand trends remained consistent with what we saw at the beginning of January with 62 percent of our respondents reporting stable demand (-1 percent from early January and -7 percent from mid-December), 23 percent reported demand as improving (-2 percent from early January and +9 percent from mid-December) and the remaining 15 percent reported demand as in decline (+3 percent from early January and -5 percent from mid-December). Demand is consistent with early January which we consider as an improvement over what we saw in mid-December.

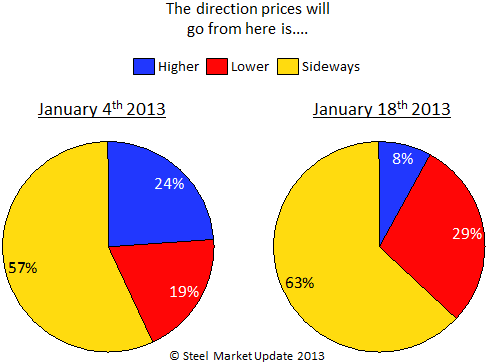

Our survey Respondents are convinced the only direction prices will go from here is sideways – with 63 percent of those taking our survey responding that way last week. a 6 point increase from what we measured during the first week of January. Those who think prices will go lower increased from 19 percent to 29 percent of our respondents while those believing prices will go higher dropped from 24 percent to only 8 percent.

Our survey Respondents are convinced the only direction prices will go from here is sideways – with 63 percent of those taking our survey responding that way last week. a 6 point increase from what we measured during the first week of January. Those who think prices will go lower increased from 19 percent to 29 percent of our respondents while those believing prices will go higher dropped from 24 percent to only 8 percent.

Survey Prompted Debate

When it comes to pricing,– and the direction of prices – there is not a consensus of opinion. Last week’s survey showed an adjustment in opinion and captured comments from our respondents:

Well-I think the question needs to be qualified by the time frame… Today’s “sideways” movements of $20-40/ton are history’s big price swings. And an immediate direction one way can be reversed the next. So depending on if “from here” is reviewed over the next week, next month, or next quarter… There is not a lot of ancillary demand right now, as pricing momentum seems to be pointed softly downward due to excess apparent supply, short lead times, and med-high inventory levels. As stated earlier, our customer demand has increased in the New Year, and I suspect the case may be similar in other places but just not discussed as much as the over-supply and dreariness that seems to be pervasive in conversations these days. Mills contend that prices are below their costs, and if true, they deserve to cover their costs and raise their prices. I suspect this is the near future. Whether that reverses momentum and leads to further increases is a bit suspect. But the market needs an end to the erosion to spark activity. From there, prices may hold at a current or slightly higher level barring other unforeseen factors (increase in demand, supply disruption, raw material cost changes, government intervention, etc.) But there is certainly the slight possibility that none of this holds, and price erosion continues breaking the glass floor and leading to further downward velocity. Midwest based service center.

Slight softening will occur solely because the mills will want to stimulate their order books, however, market fundamentals will not allow pricing to collapse. It would not surprise me to see Cold Rolled CRU roll back to $35.00-$35.25 but rebound right after the Chinese New Year. Midwest service center.

Current market is fairly soft, will be hard for increases to gain traction at this time. Manufacturing company.

Order books are very weak. Midwest service center.

Not sure – scrap price may change – some movement there – that means sideways or higher. Manufacturing company.

With Iron Ore and global steel prices increasing, I think the mills will push for an increase. Whether it holds or not, depends on how hungry our domestic mills are for the business. Manufacturing company.

My eyes are on China. With the meteoric rise in iron ore prices, I am cautiously optimistic that we will begin to see a cost-push opportunity for the domestic mills to raise pricing. Manufacturing company.