Product

February 8, 2013

CBO Economic Outlook 2013 to 2023 with Peter Wright Commentary

Written by John Packard

Written by: Peter Wright

The Economic Outlook for 2013

CBO expects that economic activity will expand slowly this year, with real GDP growing by just 1.4 percent. That slow growth reflects a combination of ongoing improvement in underlying economic factors and fiscal tightening that has already begun or is scheduled to occur—including the expiration of a 2 percentage point cut in the Social Security payroll tax, an increase in tax rates on income above certain thresholds, and scheduled automatic reductions in federal spending. That subdued economic growth will limit businesses’ need to hire additional workers, thereby causing the unemployment rate to stay near 8 percent this year, CBO projects. The rate of inflation and interest rates are projected to remain low.

The Economic Outlook for 2014 to 2018

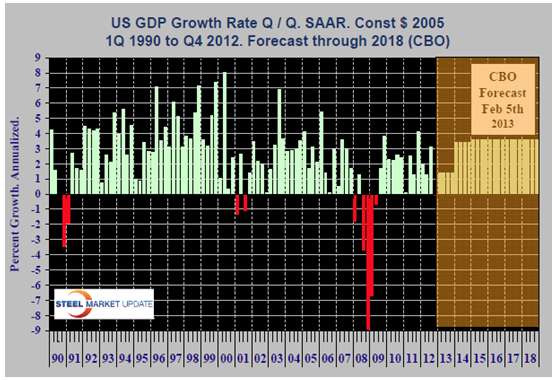

After the economy adjusts this year to the fiscal tightening inherent in current law, underlying economic factors will lead to more rapid growth, CBO projects 3.4 percent in 2014 and an average of 3.6 percent a year from 2015 through 2018, (Figure 1). In particular, CBO expects that the effects of the housing and financial crisis will continue to fade and that an upswing in housing construction (though from a very low level), rising real estate and stock prices, and increasing availability of credit will help to spur a virtuous cycle of faster growth in employment, income, consumer spending, and business investment over the next few years. Nevertheless, under current law, CBO expects the unemployment rate to remain high—above 7½ percent through 2014—before falling to 5½ percent at the end of 2017. The rate of inflation is projected to rise slowly after this year: CBO estimates that the annual increase in the price index for personal consumption expenditures will reach about 2 percent in 2015. The interest rate on 3 month Treasury bills—which has hovered near zero for the past several years—is expected to climb to 4 percent by the end of 2017, and the rate on 10-year Treasury notes are projected to rise from 2.1 percent in 2013 to 5.2 percent in 2017.

The Economic Outlook for 2019 to 2023

For the second half of the coming decade, CBO does not attempt to predict the cyclical ups and downs of the economy; rather, CBO assumes that GDP will stay at its maximum sustainable level. On that basis, CBO projects that both actual and potential real GDP will grow at an average rate of 2¼ percent a year between 2019 and 2023. That pace is much slower than the average growth rate of potential GDP since 1950. The main reason is that the growth of the labor force will slow down because of the retirement of the baby boomers and an end to the long-standing increase in women’s participation in the labor force. CBO also projects that the unemployment rate will fall to 5.2 percent by 2023 and that inflation and interest rates will stay at about their 2018 levels throughout the 2019–2023 period.

(Source: CBO. Update February 5, 2013)

Commentary:

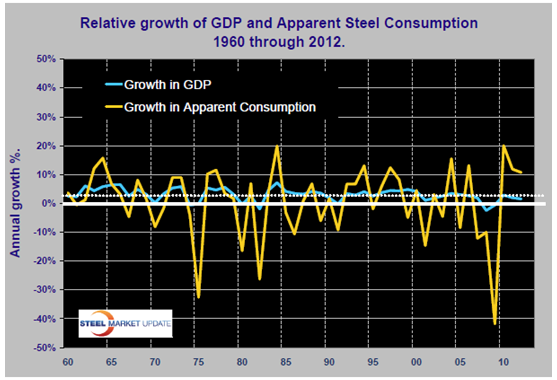

In the last 52 years – since 1960 there has been an over-riding relationship between the growth of apparent steel consumption and the growth of GDP. This indicates that in the very long term it is necessary to achieve about a 2.5 percent growth in GDP to get any growth in steel consumption. However steel is very much more volatile than GDP as shown in Figure 2. The dotted line represents the level of GDP that has to be exceeded to get any growth in steel consumption in the long term. In recent years steel growth has been much higher than the long term relationship would suggest and this will continue for several more years as we recover from the disastrous year of 2009. If the CBO is correct in its February 5th analysis then steel consumption will get an additional boost from GDP over and above the recovery effect through 2018.