Product

February 27, 2013

CRU Indexed “Contract” Spot Purchases – Have the Domestic Mills Hurt the Spot Market?

Written by John Packard

The whole reason behind the various indices is to provide transparency to domestic mill spot transactions. This, in turn, gives buyers and sellers a basis to work from when negotiating both existing (spot) and future (contract) deals.

The issue everyone has – as a buyer your job is to be at the cutting edge – below the spot transaction price level. As a mill supplier your goal is to tie up tonnage in order to keep the various pieces of equipment running at peak performance which (hopefully) will then translate into profits for the mill.

Those two goals have created CRU indexed pricing (usually at some pre-ordained discount) that end up working against the spot transparency and may actually be hampering efforts by the domestic mills to bring spot prices up at times of change. Here, I will let an executive with one of the large service center groups explain:

CRU indexed purchases as a substitute for spot buying – that is CRU index referenced during the month of PO entry, sets the price for delivery at normal lead-times. Volumes in this style of price methodology appear to be growing. I would like some kind of reference to how much of this is really going on, and who is doing it (consumers v distributors). I think you could have strong effects on the market in two main ways; 1) it removes this normally transacted “spot” from the data set that makes up the CRU index (it is called “contract” and not reported). And, 2) a kind of target price is established for non-indexed spot purchased. This target price creates a stronger ceiling for prices to break through, and therefore would mitigate the magnitude of increases, and accelerate the decreases.

If the domestic mills fail to collect these CRU purchases that are on “contracts,” but in reality are nothing more than a substitution for spot purchases, then when markets announcements are made and prices are set to rise the existence of these deals slows down that process. At the same time, what SMU has found with some buyers is if their CRU indexed “contract” deal is not as good as “spot” market prices elsewhere they will order less “contract” tons and go to the spot market thus driving prices lower.

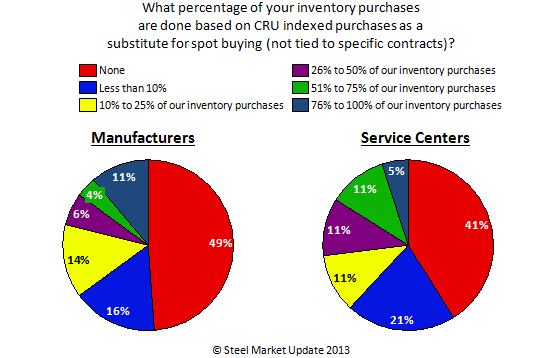

In last week’s SMU steel survey we did ask both manufacturing companies and distributors/service centers what percentage of their purchases were being made on CRU indexed deals but were not tied to specific contracts (steel tied to specific part for end customer). As you can see by the results below – the impact on the spot market can be significant if these buys are not being collected by the various indices.

If the market sample of our survey is representative of the overall market, then we can assume that a fairly high percentage of what might be construed by some as “spot” purchases are actually tied to CRU and are not being reported as part of the pool. We understand that CRU is advising both the mills and end customers that deals where specific monthly tonnages – whether for inventory or otherwise – are tied to CRU indices are not to be reported as spot purchases.

This means if a service center buys 60” galvanized coil inventory for resale into the mechanical contractors a coil at a time, but purchases the tonnage from the mill tied to a monthly CRU index (most likely with some form of discount), then that material is not consider as part of the spot pool of price assessments.

SMU is struggling with this concept.

Steel Market Update does not collect purchase information from the domestic steel mills – all of our data comes directly from the buyers of steel – manufacturing companies and distributors. Although we ask specifically for spot purchases – at the moment we will allow the buyers supplying us the information to determine if the CRU minus monthly deals which are not tied to specific contracts are actually “spot” inventory purchases and therefore they wish to report them as such.

Lately, our numbers have generally been in line with CRU – it will be interesting as the percentage of these monthly CRU indexed non-specific contract deals grows if our numbers will begin to grow apart. Time will tell.

As always your comments are both encouraged and appreciated: John@SteelMarketUpdate.com.