Product

March 13, 2013

Last Week’s Estimated Raw Steel Production

Written by John Packard

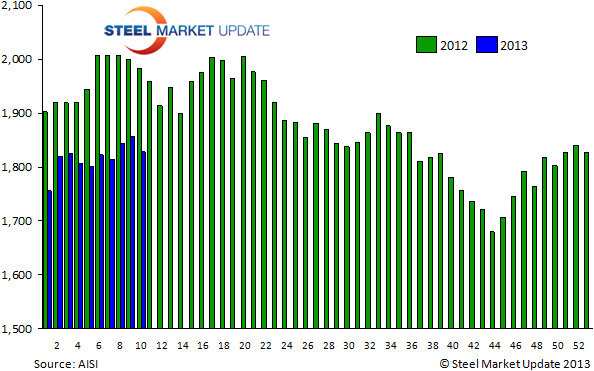

The American Iron & Steel Institute (AISI) reported their estimated raw steel production data for the week ending March 9, 2013. According to AISI estimates the U.S. steel industry produced 1,828,000 net tons of raw steel last week. This represents a decrease of 1.6 percent compared to the week earlier and is 7.8 percent lower than the same week one year ago.

The AISI estimates the capacity utilization rate to be 76.3 percent. SMU reminds our readers the AISI has made an adjustment to the domestic capabilities for 1st Quarter 2013. The new quarterly capability is 30.8 million tons. The 1Q 2012 capability number according to the AISI was 32.3 million tons and that number was adjusted to 32.7 million tons for 4Q 2012 with the addition of the new Severstal Columbus EAF.

The AISI estimates the capacity utilization rate to be 76.3 percent. SMU reminds our readers the AISI has made an adjustment to the domestic capabilities for 1st Quarter 2013. The new quarterly capability is 30.8 million tons. The 1Q 2012 capability number according to the AISI was 32.3 million tons and that number was adjusted to 32.7 million tons for 4Q 2012 with the addition of the new Severstal Columbus EAF.

Year to date the AISI estimates total raw steel produced to be 18,170,000 net tons, down 7.3 percent compared to the 19,604,000 tons produced through the same period last year. The average capacity utilization rate is estimated to be 75.7 percent so far this year, down from 79.1 percent last year – although last year comparison is against different tonnage and you are better served to compare tonnage production which we have done in the graphic provided above.

The North East district produced 195,000 net tons, down 1,000 tons from the previous week.

The Great Lakes district produced 666,000 net tons, down 8,000 tons from the previous week.

The Midwest district produced 259,000 net tons, down 5,000 tons from the previous week.

The Southern district produced 619,000 net tons, down 13,000 tons from the previous week.

The Western district produced 89,000 net tons, down 2,000 tons from the previous week.

Total production was 1,828,000 net tons, down 29,000 tons from the previous week.