Prices

June 24, 2014

May Preliminary Imports Surpass 4 Million Tons

Written by Brett Linton

The latest steel import census data has preliminary imports at 4,016,437 net tons in May, the highest tonnage levels seen since 2006. May represents a 7.4 percent increase over the previous month and an increase of 1,178,145 tons or 41.5 percent compared to May 2013. Foreign steel now represents 28 percent of the steel market.

Semi-finished steel (mostly slabs) was 25 percent of the total tons imported. This is important to note since semi-finished steels are brought in by the domestic steel industry to be rolled and shipped to domestic customers.

Oil country tubular goods (OCTG), as discussed in previous issues of Steel Market Update, exceeded 400,000 tons.

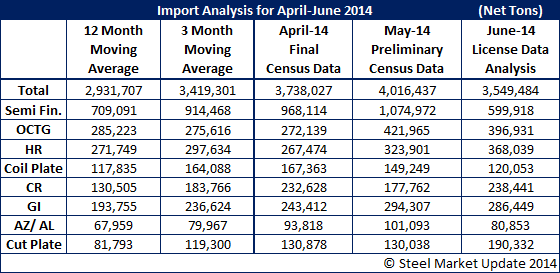

The table below shows a comparison of May imports (total and by product) to those of April and June and moving averages calculated through June.

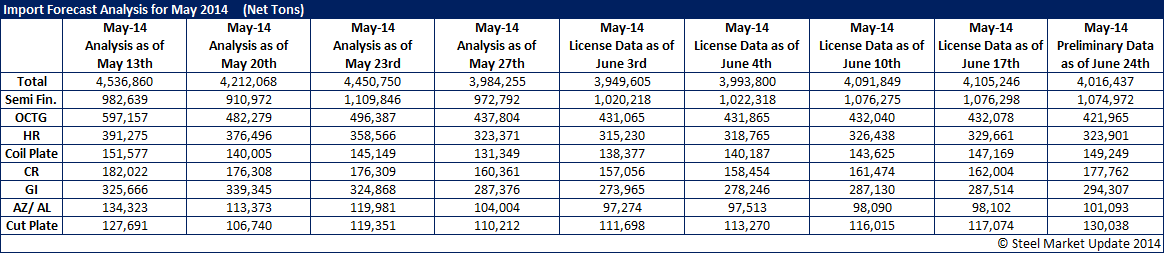

Below is a history showing the progression of import data throughout the month of May (click on the image to see a larger version).