Market Data

July 1, 2014

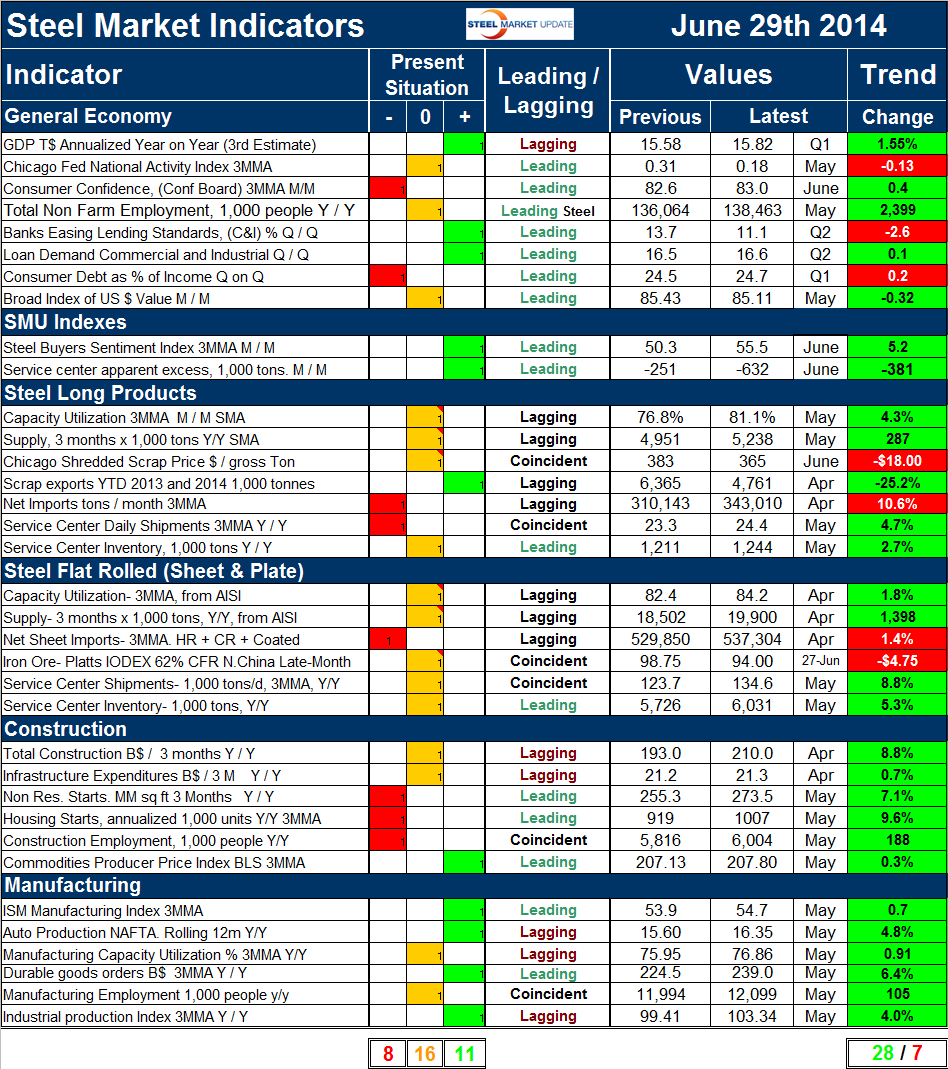

Key Steel Market Indicators on June 30th 2014

Written by Peter Wright

An explanation of the Key Indicators concept is given at the end of this piece for those readers who are unfamiliar with it. We have made two changes this month to try to make this even more representative of the market. Both the long and flat products shipment rows have been changed from “shipments” to “supply” which includes imports because we believe this is a more valuable data point when it comes to evaluating the overall market.

The total number of indicators considered at present is thirty five, the Chicago Fed Mid-West Manufacturing Index is still on hold to enable the staff to complete a major re-vamp of the structure of their report. Please refer to Table 1 for the view of the present situation and the quantitative measure of trends. Eleven of the present situation indicators based on historical standards were positive on June 29th and eight were negative with sixteen considered to be close to the historical norm. Five of the eight negative indicators were in the steel long products and construction sectors. It makes sense that these two groups would be in harmony. This broad look confirms that it is construction that is holding steel demand lower than is normal at this time in a cyclical recovery. The present situation improved significantly from our last publication on May 29th when twelve indicators were negative, thirteen positive and ten neutral. This was a net change of – 4 to the indicators classified as poor by historical standards and a net change of -2 to the indicators considered historically good.

Our view of the present situation of the general economy did not change in the last month and is barely OK with three indicators positive, three neutral and two negative.

Both the SMU buyer’s index and the SMU service center excess are currently positive. Service centers took in 632,000 tons less than they shipped which we interpret as positive for prices going forward as their inventories are lean. The steel buyer’s sentiment index is at an all-time high at 55.5. The buyer’s index is based on a survey of sheet producers and consumers and is not intended to be indicative of long product market conditions.

Present situation indicators for long products have improved in the last month and are now approaching the flat rolled position. Capacity utilization and steel supply have improved from negative to neutral since May 29th. The price of Chicago shredded has declined in recent months and has been re-classified today from positive to neutral. We regard a high price of both scrap and iron ore as positive for the market. Net imports of both long and flat products are currently high by historical standards therefore these rows are color coded red. Scrap exports continue to be historically low and are color coded green. Service center shipments continue to be below the historical norm for long products and inventories are appropriate for the shipment level.

Present situation indicators for plate and sheet products in summary had no positive indicators, one negative and five neutral. This was a net change of minus one positive and plus one neutral and occurred because we re-thought what good capacity utilization is not because there was a deterioration. This is not an exact science and is evolving over time as we try to improve the value of the analysis. There were no other changes in the last month in our view of the flat rolled market. The price of iron ore continues to decline, if the IODEX index falls below $90 / dmt we will re-classify to negative. We consider a declining iron ore price to be a negative trend for the same reason as we described for scrap above. In August last year Goldman Sachs forecast that the price of iron ore would decline to $85 in 2015 and so far that estimate looks on target. Service center shipments improved in the last month year over year and continue to be classified as neutral.

We changed our view of the current state of construction in the last month with both total and infrastructure expenditures being re-classified from negative to neutral based on the May data from the Commerce Department which measures construction put in place. Nonresidential starts, housing starts and construction employment continue to be negative by historical standards. There was no change in our view of the present situation of manufacturing in June. None of the manufacturing indicators on a present situation basis are currently negative, four are positive and two are neutral.

The quantitative analysis of the value of each indicator over time is shown in the “Trend” columns of Table 1. There is nothing subjective about this section of the analysis. Reported numbers are the latest “facts” available. The total number of positive trends in June improved by one from May with a total of 28 out of 35 indicators heading in the right direction. May was the best result in the 15 months that we have performed this analysis and June surpassed May. Changes in the individual sectors are described below. (Please note in most cases this is not June data but data that was released in June for previous months.)

Three out of eight trends in the general economy trended negative in June, this was an increase of one which was the Chicago Fed National Activity Index, (CFNAI). This is a diffusion index based on 84 sub-indexes, a value > 50 indicates expansion and < 50 indicates contraction. The CFNAI is still signaling expansion but more slowly with a May value of + 0.18. Other indicators in this section continued on their previous trajectory, however the year over year growth of GDP fell from 2.61 percent based on the first estimate of Q1 to 1.55 percent based on the third estimate. Note this is year over year, the negative 2.9 percent reported by the Bureau of Economic Analysis last Wednesday compared Q1 2014 with Q4 2013.

The trend of the SMU steel buyer’s sentiment index continued to be positive and reached an all-time high in the second half of June. The trend of service center surplus changed from negative in May to positive in June. This was because the apparent deficit rose from 251,000 tons to 632,000 tons. We regard a deficit as a positive because it points to lean inventories and higher future prices. By this logic more is better and the deficit increased therefore the trend was positive.

In the long product steel sector in June, five of seven indicators were trending in the right direction which was the same as in our May analysis. Note long product capacity utilization and steel supply data is for May and flat rolled is for April, this is because SMA, who only compile data for long products get their numbers out faster than does AISI. We use AISI data for flat rolled. Supply of long products maintained the strong surge reported last month and capacity utilization increased by 4.3 percent in May compared to April. Shipments at the service center level increased by 4.7 percent year over year continuing that positive trend. The price of Chicago shredded which had declined in March recovered by $10 in April and then declined by $15 in May and a further $18 in June. We consider a declining scrap price as negative as it suggests a weakening global and domestic market.

Of the six flat rolled steel indicators, four had a positive trend in June’s data and two negative. This was an improvement of one in positive trends. In May we reported the March shipment trend as negative and this month we are replacing shipments with supply and reporting the April supply trend as positive. This is partly the result of rising imports. In April the price of iron ore increased by $5.50, declined by $17.50 in May breaking through the $100 level and on June 27th was down to $94.00. Capacity utilization increased from 82.4 in March to 84.2 in April. Net imports of sheet products on a 3MMA basis increased for the fourth consecutive month in April, up 1.4 percent from March. Service center shipments and inventories continued to trend in a positive direction through May. Service center tons / day shipments of sheet products have now trended positive for ten straight months.

Construction trends in the May improved in six out of six indicators, as they also did in last month’s report. All indicators are year over year and all except employment are three month moving averages. It now seems to be confirmed that the decline in nonresidential and residential construction starts in March was weather related and are now back on the track of positive growth, albeit with a long way to go.

In the manufacturing sector all indicators trended positive in the June data as was the case in May. All comparisons are year over year.

The key indicators analysis is starting to look better in its view of the present situation and trends are very good which bodes well for the balance of 2014. SMU has several benchmark analyses that show steel demand to be below the historical norm for this stage of a recovery. This is because the recession in non residential and housing construction was so extreme that it will be years before the 2007 levels are regained. In addition government funded infrastructure work is still depressed.

We believe a continued examination of both the present situation and direction will be a valuable tool for corporate business planning.

Explanation: The point of this analysis is to give both a quick visual appreciation of the market situation and a detailed description for those who want to dig deeper. It describes where we are now and the direction in which the market is headed and is designed to give a snapshot of the market on a specific date. The chart is stacked vertically to separate the primary indicators of the general economy, of proprietary Steel Market Update indices, of both flat rolled and long product market indicators and finally of construction and manufacturing indicators. The indicators are classified as leading, coincident or lagging as shown in the third column.

Columns in the chart are designed to differentiate between where the market is today and the direction in which it is headed. It is quite common for the present situation to be predominantly red and trends to be predominantly green and vice versa. The present situation is sub-divided into, below the historical norm (-), (OK), and above the historical norm (+). The “Values” section of the chart is a quantitative definition of the market’s direction. In cases where seasonality is an issue, the evaluation of market direction is made on a three month moving average basis and compared year over year to eliminate this effect. Where seasonality is not an issue concurrent periods are compared. The date of the latest data is identified in the third values column. Values will always be current as of the date of publication. Finally the far right column quantifies the trend as a percentage or numerical change with color code classification to indicate positive or negative direction.