Prices

July 7, 2014

OCTG Imports & New Capacity: Something has to Give

Written by John Packard

Something has to give. US Steel announced during the month of June the closure of two of their OCTG production facilities. The McKeesport facility has a capacity of 315,000 tons of OCTG per year while the Bellville operation capacity is 100,000 tons of OCTG on an annual basis. Total US Steel production capacity of oil country tubular goods is 2.8 million net tons.

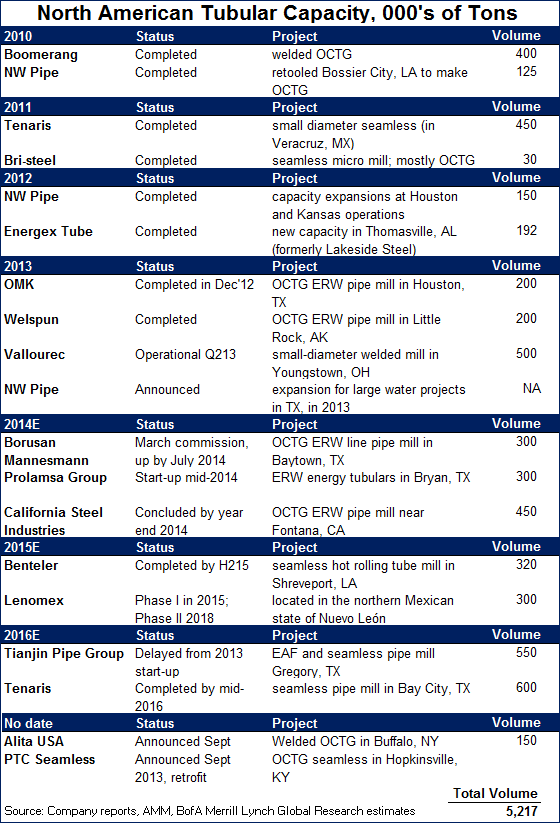

While US Steel is shutting down plants, other OCTG producing companies are either in the process of expanding capacity or have already completed capacity expansion projects. When all of the projects listed in the table below are completed, U.S. companies will have added an additional 5.2 million tons of mostly OCTG pipe production. If you add just the US Steel capacity to the new projects, the total, 7 million net tons, is approximately the size of the entire oil country tubular goods market in the United States.

The total oil country tubular goods market (OCTG) in the United States is approximately 7,000,000 net tons. This includes both seamless and welded pipe with each averaging about 50 percent of the total. The 7.0 million tons includes foreign imports of OCTG which have been averaging 297,300 net tons per month so far this year (through April 2014). If you extrapolate that out over the entire year, foreign imports are projected to account for slightly more than 50 percent of the entire OCTG market.

The biggest year for foreign imports of OCTG in the recent past was 2008 when 3.9 million net tons were exported to the United States. The biggest contributing country in 2008 was China at 2.2 million net tons or, approximately 30.4 percent of all OCTG used in the U.S. By the middle of 2008 dumping suits had been filed against the Chinese OCTG producing mills which resulted in final determinations being announced in 2010 in favor of the U.S. affected industries. China went from exporting an average of 186,617 net tons per month in 2008 to 3,511 net tons in 2010.

South Korea, on the other hand, came in and filled a portion of the void being left by the Chinese, growing their average monthly exports of OCTG from 11,260 net tons in 2009 to 45,758 (2010), 56,546 (2011), 72,553 (2012), 82,265 (2013) and, so far this year, the South Koreans are exporting an average of 118,965 net tons per month.

To put that into perspective, if maintained over the course of a full calendar year South Korea would have exported 1.428 million net tons of OCTG or 20.4 percent of the total OCTG used in the U.S.

However, the real issue is the new domestic capacity which has come online or is coming online over the next couple of years. The OCTG producers were for many years unable to keep up with demand as the oil and gas drilling segments of the market can be quite volatile suffering through boom and bust cycles. Now the industry is very close to self-sufficiency and the need for foreign imports is much less – the question becomes can the domestic producers be competitive against foreign and can the major U.S. buyers of OCTG wean themselves away from foreign OCTG or does the government have to step in and impose duties on South Korea in order to make this happen?

US Steel and the other domestic mills hope the next rulings in the OCTG trade cases go their way and the South Korean producers are forced to reduce or eliminate their exports to the USA, much the same way the Chinese were handled back in 2010.

It is not a small issue for the steel mills. If 50 percent of the OCTG imports are made up of welded pipe (balance being seamless) then the domestic mills have 1.0 to 1.5 million net tons of hot rolled production which would potentially move to the U.S. steel producers.