Prices

August 5, 2014

Chinese & Domestic Cold Rolled Analysis

Written by John Packard

We are aware that the domestic (USA) steel mills are unhappy with Chinese exports of cold rolled to the United States. The rumors of potential dumping suits against Chinese cold rolled, and possibly coated steel, have been floating about the industry for months.

Based on latest import license data for the month of July, Chinese cold rolled exports into the United States should be about 56,000 net tons. This would be lower than the 85,000 net tons delivered into the U.S. during the month of June. We will have to wait one or two months to see if this is the beginning of a trend (lower Chinese CR exports to the USA) or just a blip in the total picture.

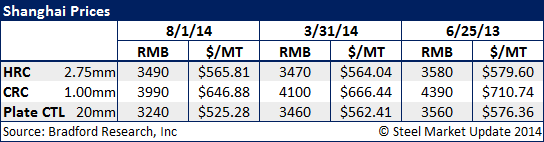

SMU was looking at domestic Chinese (Shanghai) cold rolled numbers that were part of a report produced by Charles Bradford or Bradford Research. The report cited Shanghai prices for .0397” (1.00 mm) cold rolled coils at $646.88 per metric ton. This equates to $586.84 per net ton FOB Shanghai, China. According to Mr. Bradford these prices include the 17 percent value added tax (VAT) which is collected in China.

Mr. Bradford reminder SMU that Chinese numbers can vary quite dramatically from city to city with many cities having prices lower than Shanghai. But we feel, with Shanghai being a port city, that their numbers would be good for our quick analysis today.

One of the “no-no’s” is for a country to export steel products at prices less than the same product costs in the host country. Going back to the Shanghai price listed above, and assuming that it is correct, we wanted to calculate the cost of that material to the Port of Houston. We asked one of our trading sources in Asia what the freight would be from Shanghai to Houston and we were told to add freight of $50 per ton and another $5 per ton in handling costs in Houston. That would bring the traders costs to approximately $641.84 per net ton or $32.09/cwt (there are other fees such as insurance, etc. but we want to provide ballpark figures just for comparison sake).

Value added tax is not collected on exports. So, conceivably we can use the VAT as the profit market for the trading company on a back to back deal and come up with numbers in the low $32.00/cwt range. If we to add an additional $20 per ton margin for the trading company the end result is a number around $663.84-$673.84 per ton USA port ($33.19/cwt-$33.69/cwt).

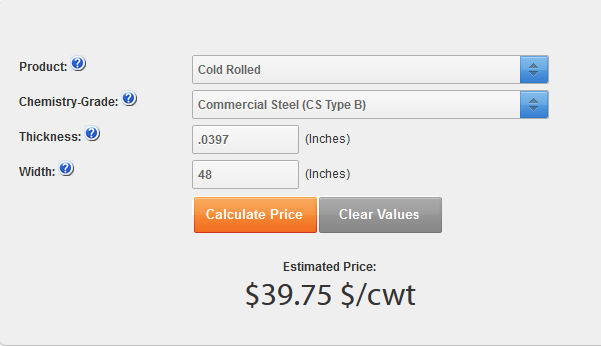

Using the SMU Price Estimator (which is a free tool on our website – see below) we calculated domestic cold rolled using the same parameters as our Chinese example and we came up with $39.75/cwt FOB Steel Mill East of the Rockies (prior to today’s changes in our cold rolled index).

Before taking freight into consideration (which is a large variable in any foreign comparison against domestic pricing) the spread between our Chinese Houston Price and Domestic Mill Price is approximately $6.00/cwt to $7.75/cwt ($120 to $155 per ton).

However, freight from the domestic mills like Nucor Arkansas and Severstal Columbus are approximately $60 per ton. This exacerbates an already competitive situation for the domestic mills as they attempt to compete in the Houston markets. However, the reverse is also true as those who try to move steel by truck into Arkansas or Mississippi have similar freight rates that they must contend with.

We checked with a couple of cold rolled buyers and learned that Chinese cold rolled was offered within the past couple of weeks around $620-$640 Houston which is at the lower end of our hypothetical range we were working with above. This morning (Wednesday, August 6th) we learned from a Houston based service center that many of the Chinese offers have been withdrawn. The last offer was at $33.00/cwt ($660 per ton) which would put the price at the high end of the range we have suggested in our analysis above.