Prices

June 9, 2015

SMU Price Ranges & Indices: Out of the "Dumps?"

Written by John Packard

Last week anti-dumping suits were filed against corrosion resistant products (mostly galvanized and Galvalume) and we did see some tightening as the domestic mills try to move prices anywhere from $10 to $20 per ton on new spot offers. We are still early in the process with many buyers either not needing to buy or waiting to see what happens next.

Hot rolled continues to be the weakest flat rolled product and our range shows no movement compared to one week ago. However, we warn our readers that we have been collecting numbers from both very large buyers as well as small and medium sized buyers. The $440 numbers are not available for small or medium sized buyers. We are seeing HRC numbers in the $460 to $480 range with more and more mills asking $480 on new offers.

The trend is for higher prices on all products with buyers paying special attention to domestic mill lead times. Any quick move on lead times could create a run up in prices. We continue to advise buyers (and sellers) of flat rolled steel to be aware of lead times and any changes in production at your supplier(s).

Here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

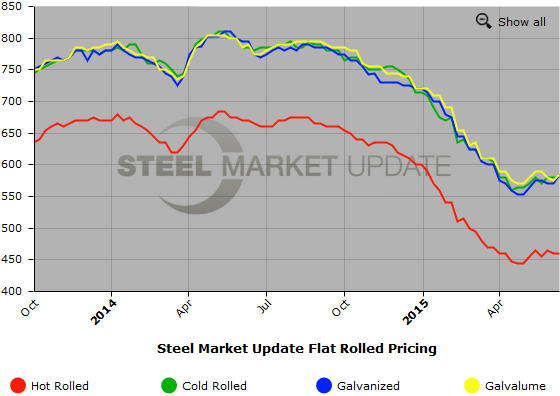

Hot Rolled Coil: SMU Range is $440-$480 per net ton ($22.00/cwt- $24.00/cwt) with an average of $460 per ton ($23.00/cwt) FOB mill, east of the Rockies. Both the upper and lower end of our range remained the same compared to last week. Our average is unchanged compared to one week ago. SMU price momentum for hot rolled steel is for prices to move higher over the next 30 to 60 days.

Hot Rolled Lead Times: 3-6 weeks.

Cold Rolled Coil: SMU Range is $560-$600 per net ton ($28.00/cwt- $30.00/cwt) with an average of $580 per ton ($29.00/cwt) FOB mill, east of the Rockies. Both the upper and lower end of our range remained the same compared to one week ago. Our average is unchanged compared to last week. We continue to believe that price momentum on cold rolled steel is for prices to move higher over the next 30 to 60 days.

Cold Rolled Lead Times: 4-7 weeks.

Galvanized Coil: SMU Base Price Range is $28.50/cwt-$30.00/cwt ($570-$600 per net ton) with an average of $29.25/cwt ($585 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to last week while the upper end of our range increased by $10 per ton. Our average is now $15 per ton higher compared to one week ago. In light of the dumping suit which affects galvanized from India, China, South Korea, Brazil and Taiwan is for prices to move higher over the next 30 to 60 days.

Galvanized .060” G90 Benchmark: SMU Range is $639-$669 per net ton with an average of $654 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-8 weeks.

Galvalume Coil: SMU Base Price Range is $28.50/cwt-30.00/cwt ($570-$600 per net ton) with an average of $29.25/cwt ($585 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago while the upper end of our range was unchanged. Our average is now $10 more than last week. Galvalume has the same circumstances as galvanized in that it is part of the corrosion resistant anti-dumping suit filed by the domestic steel mills. Our belief is momentum on Galvalume will be for higher prices over the next 30 to 60 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $861-$891 per net ton with an average of $876 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 4-6 weeks.

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.