Prices

June 16, 2015

SMU Price Ranges & Indices: Pace is Quickening on Coated

Written by John Packard

Coated steels continued to be the strongest products on the heals of AD/CVD suits having been filed on the products along with the new price increase announcements by the domestic mills. We heard from a number of galvanized buyers that the offers out of the steel mills all begin with a three (as in $30.00/cwt or higher) and lead times on coated products appear to be moving out further and faster than hot rolled and cold rolled. Even so, we saw prices increase across the board on all of the flat rolled products.

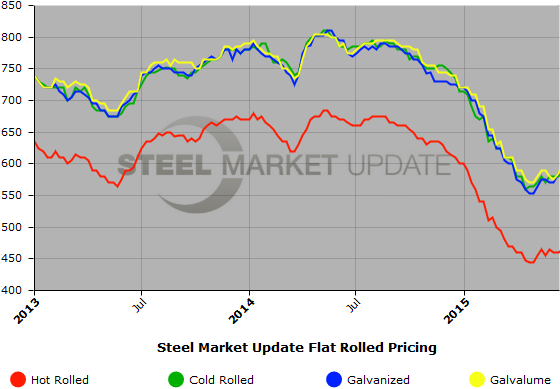

Hot rolled was up $5 per ton, cold rolled by $10 per ton with galvanized up $10 and Galvalume up $15 per ton.

Here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

Hot Rolled Coil: SMU Range is $440-$490 per net ton ($22.00/cwt- $24.50/cwt) with an average of $465 per ton ($23.25/cwt) FOB mill, east of the Rockies. The lower end of our range was unchanged compared to last week while the upper end of our range increased by $10 per ton. Our average is now $5 per ton higher compared to one week ago. Most of our survey respondents were reporting HRC offers as being $460 to $480 per ton and we even captured a few $490 per ton offers. The $440 deals were fewer and tied to a combination of relationships and tonnage. SMU price momentum for hot rolled steel is for prices to move higher over the next 30 to 60 days.

Hot Rolled Lead Times: 3-6 weeks.

Cold Rolled Coil: SMU Range is $570-$610 per net ton ($28.50/cwt- $30.50/cwt) with an average of $590 per ton ($29.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to one week ago, as did the upper end of our range. Our average is now $10 more than last week. We continue to believe that price momentum on cold rolled steel is for prices to move higher over the next 30 to 60 days.

Cold Rolled Lead Times: 4-7 weeks.

Galvanized Coil: SMU Base Price Range is $29.00/cwt-$30.50/cwt ($580-$610 per net ton) with an average of $29.75/cwt ($595 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range increased $10 per ton compared to last week. Our average is now $10 more than one week ago. As mentioned above, most offers are now at $30.00/cwt or higher (base price + extras). In light of the dumping suit which affects galvanized from India, China, South Korea, Brazil and Taiwan as well as the second price increase our opinion is for prices to move higher over the next 30 to 60 days.

Galvanized .060” G90 Benchmark: SMU Range is $649-$679 per net ton with an average of $664 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-8 weeks.

Galvalume Coil: SMU Base Price Range is $29.00/cwt-31.00/cwt ($580-$620 per net ton) with an average of $30.00/cwt ($600 per ton) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to one week ago while the upper end of our range increased $20 per ton. Our average is now $15 more than last week. Galvalume has the same circumstances as galvanized in that it is part of the corrosion resistant anti-dumping suit filed by the domestic steel mills as well as the price announcements. Our belief is momentum on Galvalume will be for higher prices over the next 30 to 60 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $871-$911 per net ton with an average of $891 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 4-6 weeks.

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.