Prices

August 7, 2015

Scrap Exports Down 9.1% for First 6 Months 2015

Written by Peter Wright

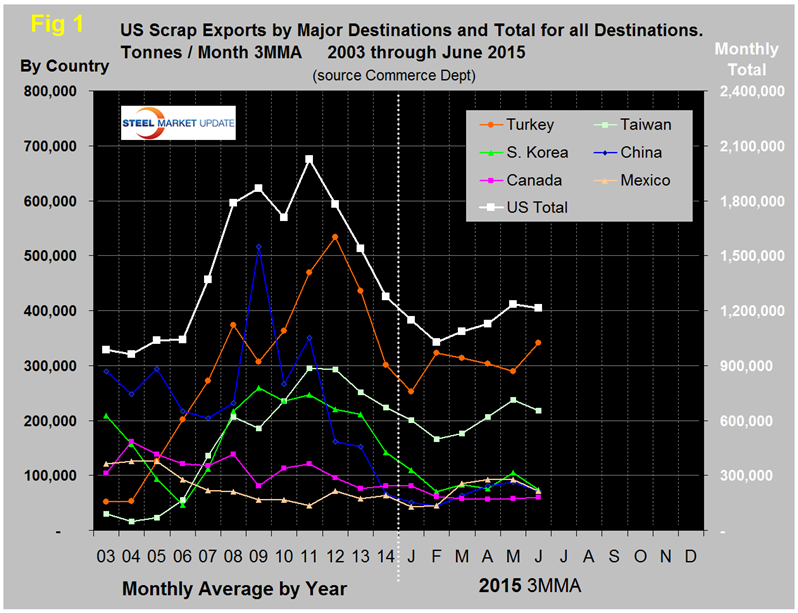

In the first six months of this year bulk scrap exports were 6,893,000 metric tonnes for an annual rate of 13,786,000 tonnes, down by 9.1 percent from the first six months of last year. The tonnages shown in Figure 1 are based on three month moving averages for 2015 and on the twelve month monthly average for previous years. The graph shows that exports declined for three consecutive years, 2012 through 2014 and continued through January and February this year. March saw a trend reversal that continued through May with a small decline in June. In the twelve months of 2014, scrap exports totaled 15,308,000 tonnes, down by 17.1 percent from the same period in 2013.

In the single month of June, Turkey was the major destination with 369,000 tonnes, followed by Taiwan with 170,000 tonnes and Thailand with 117,000. Turkey’s buy is still low by historical standards. CRU had this to say last month about the scrap situation in Turkey. “Turkish scrap consumption is largely covered by imports from the USA, Europe and the CIS. In the past month, imports of Chinese billet have risen rapidly, and displaced scrap imports, causing scrap prices to fall sharply. The volume of billet reportedly being imported from China means that scrap import demand in Turkey could be reduced by over 300,000 t a month, a reduction of 25 percent from current levels. Therefore, downward pressure on scrap prices will remain in the near term.

Over 60 percent of scrap consumption in Turkey is serviced by imports, because there is inadequate supply and infrastructure in the country to support domestic needs, and this has resulted in Turkey being the largest single country importer of scrap worldwide. However, in recent years, the high price of scrap has made it difficult for EAF scrap-based steel producers to compete with BOF iron ore-based operations, most notably from China.

Mills have naturally sought out alternatives, though until now these have been few and far between, and generally not particularly attractive. Billet imports from China have offered a lifeline to struggling Turkish producers, despite it being at the expense of production from their own steelmaking facilities. Interestingly, it is this same Chinese billet that Turkish mills hope will put them on a more level playing field to compete with finished steel exports from China itself that have encroached on Turkey’s traditional finished steel export markets. In the short term at least, unless scrap prices fall to a level acceptable to Turkish steel mills, Chinese billet will remain an increasingly favored means of supplying semi-finished steel to their rolling mills. This will mean that downward pressure on scrap prices will remain.

If key supplying countries cannot adapt and lower their cost structures to supply competitively priced scrap, Turkey could well be on the road to becoming a re-roller of Chinese material. We do not believe this will be the case in the medium term, though there are structural reasons for why scrap prices remain stubbornly high relative to iron ore and coking coal, meaning that billet continues to be an attractive option for Turkish producers in the near term. While this is good for Turkish steel mills, in some ways at least, for scrap exporters on the US East Coast and in Europe where margins are already very thin, things may yet get more difficult.”

Shipments to the Far East through the first six months were up by 19.3 percent from last year. YTD through June exports to Canada were down by 22.7 percent and to Mexico were up by 21.6 percent. Exports to India were up by 84.7 percent and to South Korea have been almost cut in half. China has received almost the same volume year over year.

Scrap export prices are reported by the AMM every Tuesday for an 80:20 mix of #1 and #2 heavy melt in US $ per tonne FOB New York and Los Angeles for bulk tonnage sales. The price on the East coast collapsed by $36 / gross ton on July 1st to $235 and has since declined to $212. The West coast price declined from $243 on July 1st to $228 on July 8th and has since declined to $198.50 on August 5th. The price of Chicago shredded was down by $35 on August 6th to $230.