Prices

October 8, 2015

Removal of Supply Should Tighten Market - The Question is When?

Written by John Packard

A debate has begun as to when flat rolled steel prices will bottom and begin to reverse course. Part of that dialogue is what will supply look like should US Steel go through with balancing their production by temporarily taking down their Granite City Works. This would be on top of the trade suits which are expected to affect future imports of hot rolled, cold rolled and coated steels.

US Steel Could Remove 7.6 Million Tons of Supply

US Steel has warned that it is considering idling their Granite City Works and its 2.8 million tons of steel making capacity and most of its downstream rolling operations (the key word here is “considering”–they put out WARN notices earlier this year and then did not follow through on taking down production at Granite City). This new announcement comes after already announcing the closure of the hot end and most of the rolling operations at the company’s Fairfield Works steel mill just outside of Birmingham, Alabama. The Fairfield mill is capable of producing 2.4 million tons of steel.

The company also is backing away from reacquiring their Canadian operations: Hamilton Works and Lake Erie Works. The Hamilton operation shuttered their steel making operations well over a year ago. The second USS Canada operation, Lake Erie Works, is capable of producing approximately 2.4 million tons of steel. Both plants which make up the Canadian operations are in bankruptcy and it is looking doubtful that they will be a player in the 2016 market unless they get a new owner (and that is not expected to happen at any point soon).

Looking at what happened with Sparrows Point, Wheeling and Warren steel plants after being acquired by RG Steel, SMU is concerned that the Canadian operations of US Steel may be following the same flight path….

The combination of all of the US Steel operations discussed above are capable of producing approximately 7.6 million tons of flat rolled sheet products. A portion of, if not all of these tons are looking like they will be taken off the market as we move into First Quarter 2016.

At the same time, 15,000 tons per month of automotive sheet products could be moving to US Steel mills located in the United States which will help tighten their automotive lines here in the States (this is in litigation in the Canadian courts right now).

There have been rumors of ArcelorMittal also doing some production justification moves but SMU has not yet seen anything from the company confirming such a move. The company still has their blog posting dated July 14, 2015 stating they have “no intention of reducing our blast furnace capacity in the United States.” The company will be announcing their 3rd Quarter 2015 earnings later this month or by early November and we should get a sense of what they are going to do by then (if not before).

We are not aware of AK Steel or any of the EAF producers making any capacity adjustments above and beyond their current ability to adjust their production capabilities.

Even so, with the US Steel production adjustments combined with an anticipated reduction in flat rolled steel imports there should be some consolidation/reduction of inventories between now and the end of the year.

How quickly those inventory adjustments are made will have a major impact on where steel prices will be by the first week of January 2016.

The combination of the trade suits beginning to come into focus (CORE – or corrosion resistant steels – Preliminary Determination is due to be announced on November 2nd) and some idling of US Steel operations should help lead to a more balanced supply/demand scenario.

One of the conversion mills told us this afternoon, “The year end special has come early. I think that it would behoove customers to make their buys fairly soon and start committing Q1 tons because once the mills shut down they won’t come back anytime soon and production will match demand quite quickly. I do not believe the market will be over-inventoried much past 12/31.”

We reported on Tuesday of this week that total imports have been dropping by approximately 200,000 tons per month over the past couple of months. The license data for September suggests the month will come in around 2.8 million net tons, down from the 3.0 in August which was down from the 3.2 million tons received in July.

In SMU’s opinion, the combination of lower domestic flat rolled prices and the trade suits against coated products, cold rolled and hot rolled steels will push total imports down to more reasonable import levels of approximately 2.2-2.4 million tons.

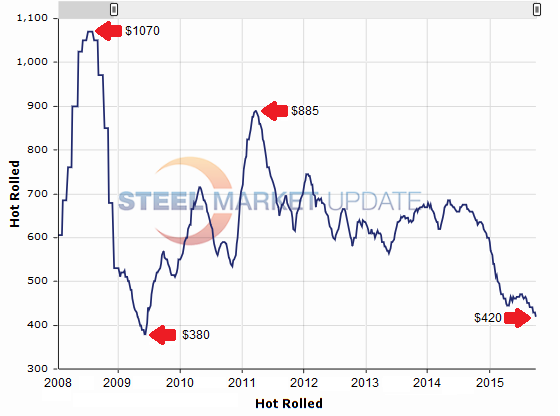

Buyers aren’t (yet) buying into the theory that the end of year specials are here at this point in time or that we may well have more pricing pain to go through in the coming weeks. A number of buyers with whom we communicate on a regular basis are forecasting prices to break through the $400 level (and in some cases already have) on benchmark hot rolled steel coil.

Where will prices go from there? One of the larger national service center chains told us, “…I don’t know if I’d buy into a V shape bounce which everyone seems to jump to always. We sure didn’t see any of the predictions come through during the last 4 months did we?” This executive went on to say, “My thoughts: we will get a big bounce if the price goes to $380 or lower, but where does that get us to – $430? How long can the US keep premium before imports return? There may certainly be some periods where we see premiums but I don’t believe they’ll be sustainable. Last forecast I read for Iron Ore for next year is the mid $30’s. If that turns out to be the case, hard to see how prices move up globally, let alone in the US, for sustained periods.”

A large manufacturing company provided their opinion on the subject of supply rationalization and its impact on pricing in the coming months, “I think there will be capacity taken off line but I don’t see a huge impact to the market. I don’t know anyone that is interested in any tons at the end of the year because I believe that people are more afraid of having orders and trying to fill them versus having inventory and trying to sell it! People are only buying what they know they have sold in my opinion.”

While a medium sized Midwest based service center executive told us that he believed, “The downside risk is really limited. We are entering a period where historically things start to firm up as people make decisions on 2016.” He went on, “I think two to three weeks and then people will make decisions to buy.”

The lowest price recorded for hot rolled coil by the Steel Market Update index was $380 per ton (average) back in June 2009. Prices remained at that level for two weeks before bouncing back from there.

Shredded scrap prices bottomed in March 2009 at $167.50 per gross ton and actually began to rise before hot rolled prices did. We are hearing of scrap buys between $175 and $185 per gross ton for October.

First Quarter 2016 HRC futures traded today at $423 per ton, according to Andre Marshall of Crunchrisk, LLC. SMU believes we could see HRC index averages dropping below $400 per ton in the coming weeks. Will this drop be seen as a buying opportunity or another reason to shrink inventory levels?