Prices

January 18, 2016

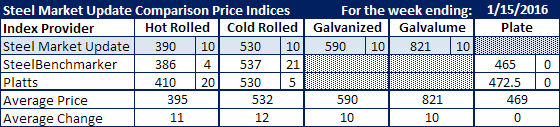

Comparison Price Indices: Wind Behind Mill's Backs

Written by John Packard

Flat rolled steel prices are beginning to catch some wind behind their backs this past week according to the various steel indices followed by Steel Market Update. Benchmark hot rolled prices moved from a low of $4 per ton (SteelBenchmarker at $386) to as much as $20 per ton (Platts at $410). What is undeniable at this point is momentum is on the side of the domestic mills and they pushed the envelope with their second price increase announcement in slightly over a month.

Cold rolled prices ranged from $530 per ton (SMU & Platts) to a high of $537 per ton (SteelBenchmarker) while galvanized and Galvalume both rose $10 per ton. A note about galvanized and Galvalume indexed pricing. SMU produces base price ranges and averages for both products. Those are the numbers you should watch the closest as extras are negotiable. The prices below defer to the full extras for .060” G90 on Galvanized and .0142” AZ50, Grade 80 on Galvalume.

Plate prices did not move even though the mills announced a $30 per ton increase just prior to the flat rolled $20-$30 increase announced last week.

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.