Prices

February 21, 2016

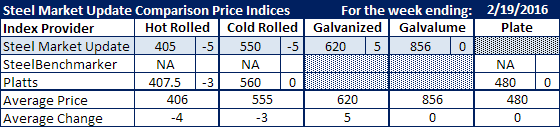

Comparison Price Indices: Some Weakening in Hot Rolled

Written by John Packard

We actually saw some pull back in hot rolled and cold rolled pricing. The amounts were minimal and, in our opinion, do not represent a deteriorating or change in market direction. The hot rolled market is not as strong as that of cold rolled which is not as strong as that of coated steels. Some of this is due to the weakness in the energy, mining and agricultural equipment markets (affecting hot rolled) while seasonal factors are starting to come into play on coated steels.

Last week both Steel Market Update and Platts saw hot rolled prices as down slightly. Our average (without Steel Benchmarker who did not report new prices this past week) was down $4 per ton to $406 per ton.

Cold rolled prices were down $5 at SMU and unchanged at Platts. Our average is now $555 per ton.

Galvanized prices were up $5 per ton and Galvalume pricing remained the same as the prior week.

Plate prices also remained stable at $480 per ton according to Platts.

FOB Points for each index:

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.