Prices

April 5, 2016

SMU Price Ranges & Indices: Still Moving Higher

Written by John Packard

Flat rolled prices continue to tighten and lead times continue to be extended, based on our analysis of the flat rolled steel markets and pricing this week.

Buyers are reporting a shrinking of the range of offers available out there. So, even though we have a range of $440-$460 per ton on hot rolled, we are being told that most of the offers are at the upper end and the number of offers at, or below, $440 are limited. The same goes for other products as well. We are not seeing a large number of offers on coated steels below $31.50/cwt.

We had two mills tell us this afternoon that they had stopped taking orders for a few days (prior to NLMK announcement) as they waited to see where market prices shake out going forward. One galvanized mill told me they were at $32.50/cwt base when they quit while a Galvalume supplier told me they were at $33.50/cwt and carefully controlling their order book.

At this moment here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

Hot Rolled Coil: SMU Range is $440-$460 per ton ($22.00/cwt- $23.00/cwt) with an average of $450 per ton ($22.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago while the upper end remained the same. Our overall average is up $10 per ton over last week. SMU price momentum for hot rolled steel has prices rising over the next 30 days.

Hot Rolled Lead Times: 4-7 weeks.

Cold Rolled Coil: SMU Range is $610-$640 per ton ($30.50/cwt- $32.00/cwt) with an average of $625 per ton ($31.25/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range rose $10 per ton compared to last week. Our overall average is up $10 over one week ago. SMU price momentum for cold rolled steel is for prices to increase over the next 30 days.

Cold Rolled Lead Times: 5-8 weeks.

Galvanized Coil: SMU Base Price Range is $31.00/cwt-$32.50/cwt ($620-$650 per ton) with an average of $31.75/cwt ($635 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago while the upper end increased $10 per ton. Our overall average is up $15 per ton over last week. Our price momentum on galvanized steel is for prices to move higher over the next 30 days.

Galvanized .060” G90 Benchmark: SMU Range is $680-$710 per net ton with an average of $695 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 6-10 weeks.

Galvalume Coil: SMU Base Price Range is $31.50/cwt-$33.50/cwt ($630-$670 per ton) with an average base of $32.50/cwt ($650 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to last week while the upper end increased $30 per ton. Our overall average increased $25 per ton over one week ago. Our price momentum for Galvalume steel is currently pointing towards an increase in prices over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $921-$961 per net ton with an average of $941 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-9 weeks.

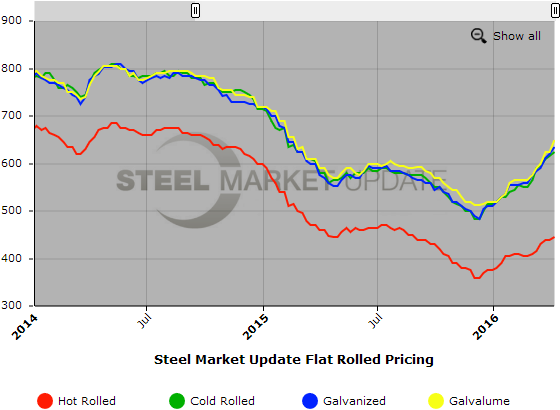

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.